- Powell reiterates recent themes on first day of his Congressional testimony

- USTR Lighthizer testifies today on key trade topicsPM May will allow Parliament to vote against “no deal” with vote-a-rama March 12-14

- U.S. economic reports expected mildly positive

- China’s mfg PMI expected to match 3-year low

Powell reiterates recent themes on first day of his Congressional testimony — Fed Chair Powell in his first day of testimony to Congress on Tuesday in the semi-annual monetary policy hearings had little to say that the markets have not already heard. The dollar temporarily strengthened when Mr. Powell expressed confidence about the U.S. economy. However, the stock market showed little net reaction to the testimony. Mr. Powell will appear today before the House Financial Services Committee, delivering the same prepared remarks but answering different questions.

Mr. Powell stressed the Fed’s policy of “patience” and said, “We’re in no rush to make a judgment about changes in policy.” He referred to “crosscurrents and conflicting signals,” “muted” inflation pressures, policy uncertainties involving Brexit and trade tensions, and concern about overseas growth. Mr. Powell offered no fresh news on the Fed’s approach to its balance sheet.

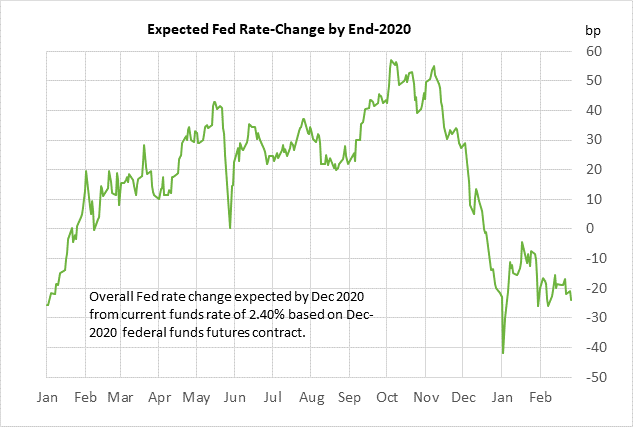

The federal funds futures curve on Tuesday turned slightly more dovish by 2-3 bp for the 2019-2020 contracts in response to Mr. Powell’s testimony. The federal funds futures market is currently discounting no change in the funds rate this year but a 96% chance of a -25 bp rate cut in 2020 with the Dec 2020 contract trading at 2.16% (i.e., 24 bp below the current funds rate of 2.40%).

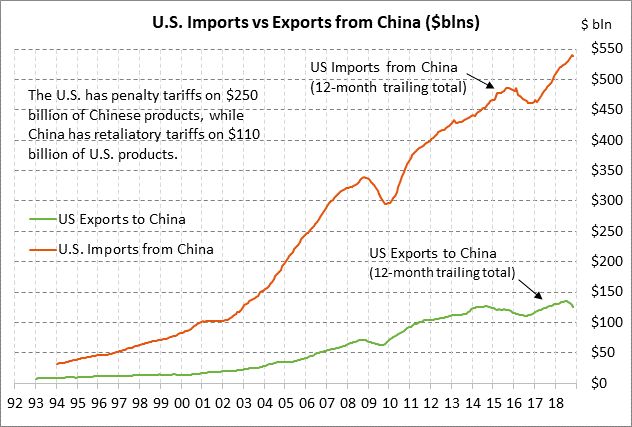

USTR Lighthizer testifies today on key trade topics — U.S. Trade Representative Lighthizer testifies today before the House Ways and Means Committee. The markets are mainly interesting in hearing from Mr. Lighthizer about how close the U.S. and China actually are to a final trade agreement. President Trump has been very optimistic about an agreement but Mr. Lighthizer is a long-standing China-trade hawk who seems to want to drive a hard bargain with China regardless of how the markets react.

The markets are also very interested in hearing whether President Trump plans to slap tariffs on imported autos. The Commerce Department has already delivered its recommendation to President Trump about whether tariffs on imported autos can be justified on national security grounds but those conclusions have yet to be made public. Yet there is little doubt that the Commerce Department complied with Mr. Trump’s plan to threaten the EU and Japan with tariffs on imported autos. Mr. Trump last year promised to hold off on any new tariffs on Europe and Japan while trade talks are progressing. However, Europe in particular is nervous that Mr. Trump may go ahead with tariffs on European autos anyway because the US/EU trade talks are moving slowly and because the EU wants to stick to the industrial sector and avoid discussions about the agriculture sector.

The other key topic of trade interest is the NAFTA 2.0 agreement that the Trump administration negotiated with Mexico. Congress needs to approve the new US/Mexico trade treaty and there is plenty of opposition to the treaty from different factions in Congress. Mr. Trump has threatened to announce a U.S. withdrawal from the current NAFTA agreement in order to start the clock running on the 6-month notice period, thus stepping up the pressure on Congress to accept his NAFTA 2.0 deal without changes.

PM May will allow Parliament to vote against “no deal” with vote-a-rama March 12-14 — Prime Minister May on Tuesday outlined her plan to have Parliament vote on her Brexit separation agreement on March 12. If that plan is voted down, then she will allow a vote on March 13 on whether to prevent a “no deal” Brexit on March 29. Assuming that Parliament votes to prevent a “no deal,” then she will allow a vote on March 14 about whether to delay the March 29 Brexit deadline. Ms. May said she would only offer a short deadline extension until perhaps June.

By allowing a vote to prevent a no-deal Brexit, Ms. May at least temporarily put down a rebellion by members of Parliament and indeed members of her cabinet who refuse to allow the disaster of a no-deal Brexit. Parliament will hold Brexit votes today, but it remains to be seen whether there will be any votes on amendments of consequence. The big votes will come on March 12-14.

Ms. May is still hoping to pull a rabbit out of the hat by getting Parliament to approve her Brexit separation agreement, which would usher in a smooth transition period through December 2020 during which time the UK would remain in the EU single market and have time to negotiate a final trade deal with the EU. There is still a small chance for success on that plan if Attorney General Cox can get enough assurances from the EU to soften his previous legal conclusion that the Brexit separation plan with its Irish backstop could trap the UK in the EU forever.

Hard-line Brexit Conservatives now have an increased incentive to vote in favor of Ms. May’s plan because a delay in the March 29 Brexit deadline could mean that Brexit might never happen at all if calls grow for a second public referendum. Indeed, Labour leader Corbyn this week adopted a Labour policy of calling for a second public vote.

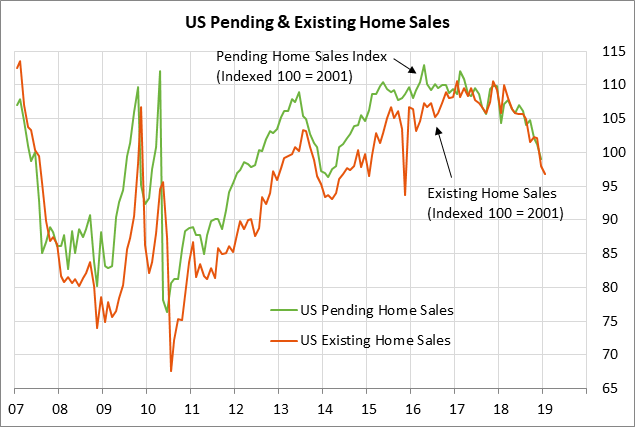

U.S. economic reports expected mildly positive — Today’s U.S. economic reports are expected to be mildly positive. The consensus is for today’s Jan pending home sales report to show an improvement of +1.0% m/m and -4.6% y/y from the weak Dec report of -2.2% m/m and -9.5% y/y. Today’s Dec factory orders report is expected to show an increase of +0.6% following Nov’s report of -0.6% and -1.3% ex-transportation.

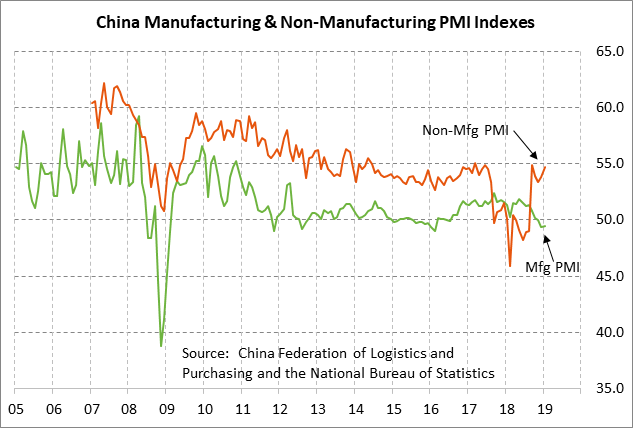

China’s mfg PMI expected to match 3-year low — The consensus is for today’s China Feb manufacturing PMI to fall -0.1 to match December’s 3-year low of 49.4 (after Jan +0.1 to 49.5). The Feb non-manufacturing PMI is expected to fall -0.2 to 54.5, giving back part of Jan’s +0.9 increase to 54.7.