- Powell may shed more light on Fed balance sheet and rate-pause policies

- Chinese government position seems to be more cautious than Trump on trade deal prospects

- PM May may be close to delaying Brexit

- U.S. economic report deluge today

- 7-year T-note auction

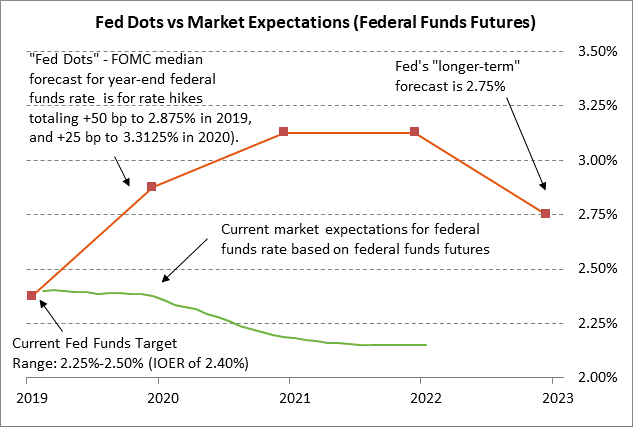

Powell may shed more light on Fed balance sheet and rate-pause policies — Fed Chair Powell will testify today before the Senate Banking Committee in the first day of his 2-day semiannual Congressional hearings on monetary policy. The two main topics of interest are the Fed’s rate-hike pause and its balance sheet policy. The federal funds futures market is currently discounting no change in the funds rate this year but an 84% chance of a -25 bp rate cut in 2020 with the Dec 2020 contract trading at 2.19% (i.e., 21 bp below the current funds rate of 2.40%).

The FOMC at its last meeting on Jan 29-30 shifted to a fully-neutral policy and removed its guidance for a slow rise in interest rates. However, the tightening bias could be reinstated if global risks abate and if U.S. inflation strengthens. Last Wednesday’s FOMC minutes said, “Many participants observed that if uncertainty abated, the Committee would need to reassess the characterization of monetary policy as ‘patient’ and might then use different statement language.”

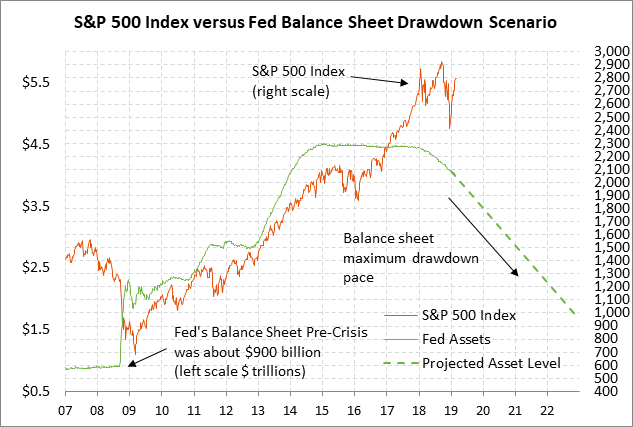

On the balance sheet, the Jan 39-30 FOMC meeting minutes said, “Almost all participants thought that it would be desirable to announce before too long a plan to stop reducing the Federal Reserve’s asset holdings later this year.” The markets had previously thought that the FOMC would continue its balance sheet runoff at least into 2020. However, the FOMC seems to fear that tighter liquidity caused by the balance sheet runoff may indeed have been a factor behind the sharp sell-off in global stocks in Q4-2018.

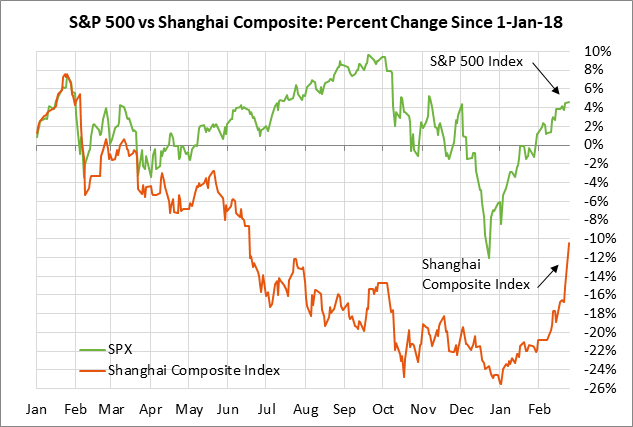

Chinese government position seems to be more cautious than Trump on trade deal prospects — The Shanghai Composite index on Monday soared by 5.6% to a new 8-month high on optimism about a possible U.S. trade deal after President Trump on Sunday delayed the March 1 tariff-hike deadline. The U.S. stock market had a more measured reaction with the S&P 500 index closing the day just slightly higher by +0.1%.

The difference in the reactions can be traced in part to the fact that China has much more to lose than the U.S. if President Trump goes ahead with raising the tariff to 25% from 10% on $200 billion of Chinese goods. China has already slapped retaliatory tariffs on $110 billion of U.S. goods, which covers nearly all of U.S. exports to China. In order to retaliate further, China would have to raise the existing retaliatory tariff levels and perhaps take non-tariff moves such as limiting the ability of U.S. companies to do business in China.

In any case, President Trump’s announcement of a delay in the March 1 tariff deadline has to be taken with a grain of salt because there was no date specified for a new tariff deadline or for a summit between Presidents Trump and Xi. The delay of the March 1 deadline was good news, but the bad news is that President Trump could raise the tariffs at virtually any time if the US/Chinese trade talks should suddenly fall apart.

In addition, Chinese officials seemed to take a more cautious view of the talks when the state-run new agency Xinhua on Monday said, “Trade talks will be harder at the final stage, and new uncertainties can’t be ruled out. There needs to be a sober mind about the fact that the China-U.S. trade frictions are long-term, complicated and arduous.” Most reports suggest that there are still significant issues to be resolved, particularly when it comes to enforcement.

PM May might be close to delaying Brexit — Bloomberg reported late Monday afternoon that Prime Minister May today will discuss the possibility of delaying the Brexit deadline with her cabinet. An announcement of any decision could come after the cabinet meeting. Ms. May seems to have finally realized that she has hit a dead end with Parliament and ministers in her cabinet are ready to take whatever votes are necessary to prevent a no-deal Brexit. Without the threat of a no-deal Brexit and with no EU concession on the Irish backstop, Ms. May has little chance at this stage of producing a Brexit separation agreement that could be approved by Parliament. Her only option now is to accept a Brexit delay rather than have it forced upon her by Parliament, in the process causing what would likely to be a slew of resignations from her cabinet.

A delay of the Brexit deadline would prevent a no-deal Brexit, but would also infuriate the hard-Brexit wing of her party and could even lead to the downfall of the government in a no-confidence motion. A delay would also open the door for a second public referendum on Brexit, which could result in Brexit not happening at all. Labour Leader Corbyn on Monday finally pulled the trigger and said that the Labour Party now favors a second public Brexit vote.

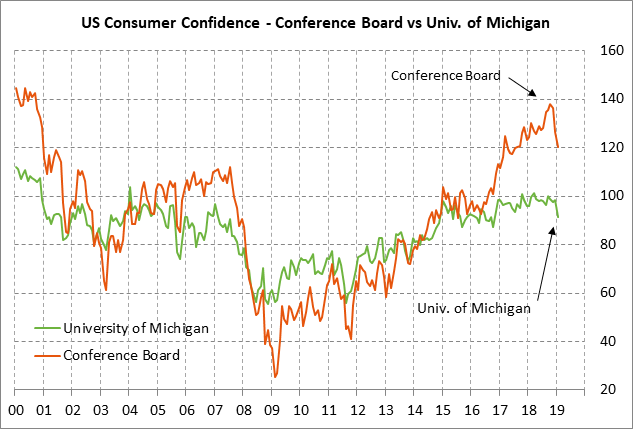

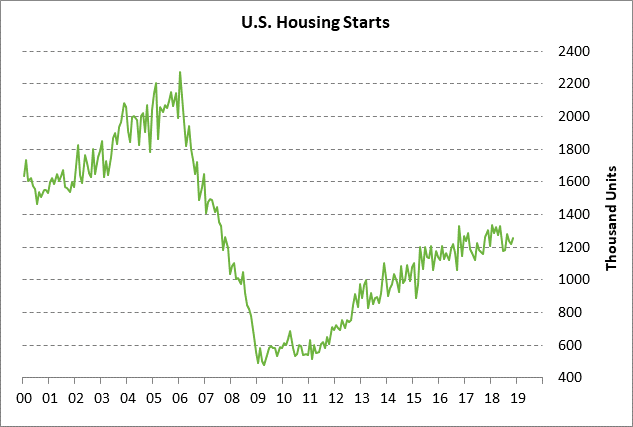

U.S. economic report deluge today — There is expected to be some positive consumer news today since the consensus is for today’s Feb Conference Board U.S. consumer confidence index to show a +4.5 point increase to 124.7, reversing part of January’s -6.4 point decline to 120.2. On the housing front, today’s Dec housing starts report is expected to show a small -0.2% decline to 1.253 million, giving back a little of Nov’s +3.2% increase to 1.256 million. U.S. home prices are expected to move higher with the Dec FHFA house price index up +0.4% m/m (after Nov’s +0.4%) and the Dec S&P CoreLogic composite-20 home price index up +0.3% m/m and +4.5% y/y (after Nov’s +0.3% m/m and +4.7% y/y.).

7-year T-note auction — The Treasury today will conclude this week’s $113 billion T-note package by selling $32 billion of 7-year T-notes. The Treasury sold 2-year and 5-year T-notes on Monday. The Treasury is holding its T-note auctions earlier in the week than usual due to Fed Chair Powell’s testimony on Tuesday and Wednesday. The 7-year T-note yield in February has traded sideways in a narrow range and closed +0.7 bp at 2.558% on Monday.