- Weekly global market focus

- President Trump delays March 1 tariff deadline

- Prime Minister May postpones this week’s Brexit vote until March 12

- Heavy T-note supply on Monday-Tuesday

- Q4 earnings season winds down

Weekly global market focus — The U.S. markets this week will focus on (1) reaction to the Sunday news from President Trump of progress in the US/Chinese trade talks and the delay of Friday’s tariff deadline, which prompted a +0.3% rally in stock index futures on Sunday night, (2) Fed policy with Fed Chair Powell testifying before Congress on Tuesday and Wednesday in the semi-annual monetary policy hearings, (3) testimony by U.S. Trade Representative Lighthizer on Wednesday before Congress on topics such as US/Chinese trade talks, whether President Trump will impose duties on U.S. auto imports, and NAFTA 2.0, (4) possible political turmoil as former Trump lawyer Michael Cohen testifies publicly on Wednesday before the House Oversight Committee, (5) the Treasury’s sale of $113 billion of T-notes on Monday and Tuesday, (6) the tail end of Q4 earnings season with 37 of the S&P 500 companies scheduled to report, and (7) a busy U.S. economic schedule that includes Thursday’s U.S. Q4 GDP report (expected +2.5% after Q3’s +3.4%). The Justice Department said last Friday that the Mueller report will not be released this week.

In Europe, the focus remains on Brexit as UK/EU negotiations over the Irish backstop will continue this week as PM May delayed Wednesday’s Brexit vote until March 12. The European markets are also looking ahead to next Thursday’s (March 7) ECB meeting and whether the ECB will announce a big round of new TLTRO loans to replace expiring loans, thus keeping the banking system fully liquefied.

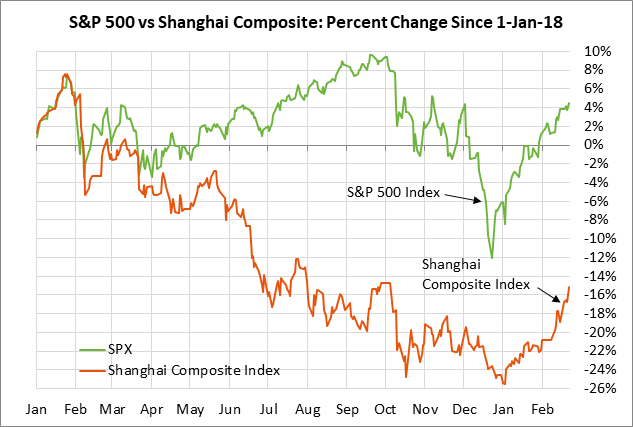

In Asia, the focus will be on the US/Chinese trade talks and whether Chinese stocks can continue the Jan/Feb recovery. The Shanghai index last Friday posted a 4-3/4 month high and recovered by a total of +14.9% from the early-January 4-1/4 year low. China’s manufacturing PMI reports on Wednesday and Thursday nights (ET time) are expected to stabilize after the recent weakness.

President Trump delays March 1 tariff deadline — In a relief for the markets, President Trump late Sunday afternoon announced a delay of this Friday’s tariff deadline. Mr. Trump said that if there is continued progress in negotiations, then he and President Xi will meet at Mar-a-Lago to conclude the deal, although he did not give any timing on that anticipated meeting. Treasury Secretary Mnuchin last Friday that plans are being made for Presidents Trump and Xi to meet later in March at Mar-a-Lago.

Specifically, President Trump on Sunday tweeted, “The U.S. has made substantial progress in our talk talks with China on important structural issues including intellectual property protection, technology transfer, agriculture, services, currency, and many other issues. As a result of these productive talks, I will be delaying the U.S. increase in tariffs now scheduled for March 1.

The markets are relieved that Mr. Trump delayed the March 1 deadline, which raises expectations for the successful conclusion of the talks. However, the bad news is that the markets are now operating on a day-to-day basis since Mr. Trump did not say how long the tariff deadline would be extended or when he and President Xi will be holding a meeting to presumably announce a final agreement. That raises the possibility that the tariffs could be raised at any time if the talks should suddenly fall apart. The U.S. Trade Representative’s office this week will formally announce the extension of the tariff deadline and a new deadline date could be given then.

Prime Minister May postpones this week’s Brexit vote until March 12 — Prime Minister May postponed this Wednesday’s Brexit vote until March 12, which will be only 17 days before the March 29 Brexit deadline. Ms. May delayed the vote as her negotiators are scheduled to return to Brussels on Tuesday to resume negotiations on the Irish backstop. Ms. May is still hoping to get enough concessions from the EU on the Irish backstop that she can present a final Brexit separation agreement to Parliament that will be accepted, thus ushering in a smooth transition period until Dec 2020.

However, the EU is still flatly rejecting a reopening of the Brexit separation or any significant concessions on the Irish backstop. A vote by Parliament in favor of a Brexit separation agreement before the March 29 deadline seems increasingly hopeless, leading to expectations that Ms. May in March will be forced to request a delay of the March 29 Brexit deadline. If Ms. May doesn’t request the delay herself, then Parliament at their March 12 vote seems likely to vote on the Cooper amendment that would require a deadline delay.

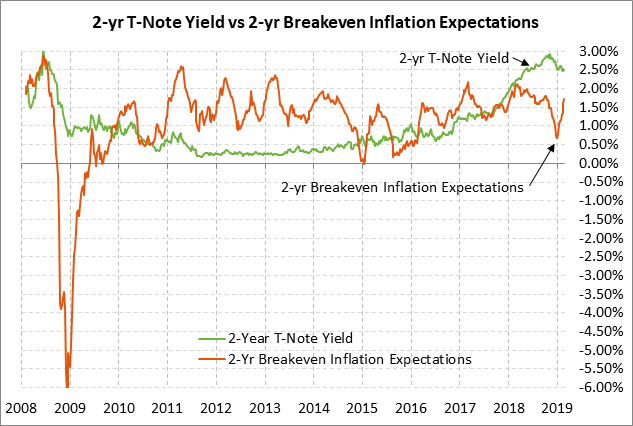

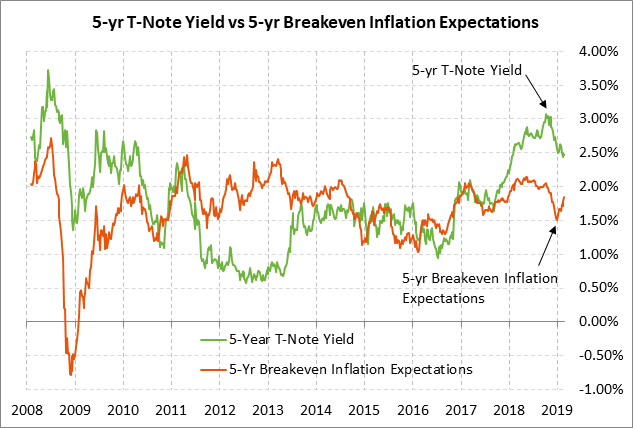

Heavy T-note supply on Monday-Tuesday — The Treasury today will sell $40 billion of 2-year T-notes and $41 billion of 5-year T-notes. The Treasury will then conclude this week’s $113 billion T-note package by selling $32 billion of 7-year T-notes on Tuesday. The Treasury is holding its T-note auctions earlier in the week than usual due to Fed Chair Powell’s testimony on Tuesday and Wednesday. The 2-year and 5-year T-note yields have traded sideways in the past three weeks and the 2-year yield last Friday closed at 2.49% while the 5-year closed at 2.47%.

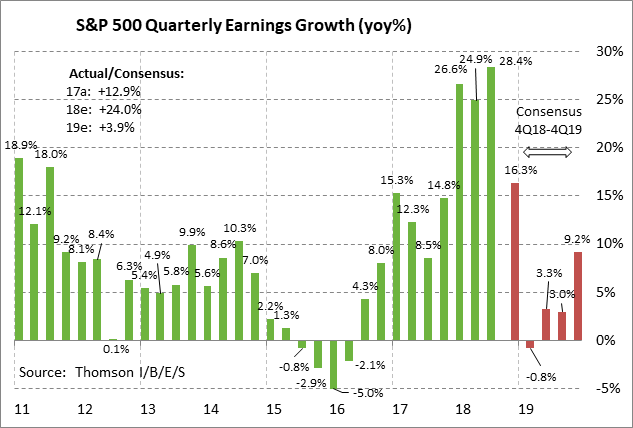

Q4 earnings season winds down — Q4 earnings season is winding down with 37 of the S&P 500 companies reporting this week. Of the 444 SPX companies that have so far reported, 69.1% have beaten earnings according to Thomson Reuters Refinitiv, above the long-term average of 64% but below the 4-quarter average of 78%.

After strong Q4 earnings growth near +16.3% y/y, the consensus is for SPX earnings growth in Q1 to fall to -0.8% y/y as the tax-cut effects fade and then remain weak at +3.3% in Q2 and +3.0% in Q3. The consensus is for SPX earnings in 2019 to ease to +3.9% from +24.0% in 2018.