- Dovish minutes show FOMC members on board with pause and that balance sheet runoff could end this year

- US/Chinese high-level trade talks resume today

- EU-UK are reportedly working on compromise backstop language

- 30-year TIPS auction

- U.S. economic report deluge today

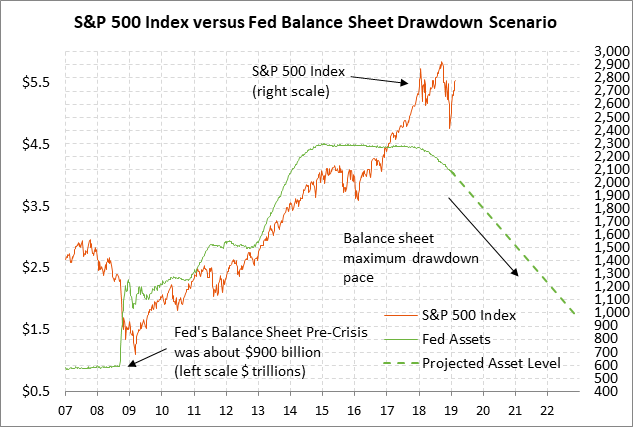

Dovish minutes show FOMC members on board with pause and that balance sheet runoff could end this year — Wednesday’s minutes from the Jan 29-30 FOMC meeting were dovish although the federal funds futures curve closed the day little changed. The minutes showed that most of the FOMC members were on board with the Fed’s dovish shift to a fully-neutral policy from the previous guidance toward higher rates. However, the minutes also implied that there could be a shift back to a hawkish tilt by saying, “Many participants observed that if uncertainty abated, the Committee would need to reassess the characterization of monetary policy as ‘patient’ and might then use different statement language.”

The big news from the minutes was that the FOMC anticipates ending its balance sheet reduction plan by later this year, which is sooner than the recent consensus of 2020. The minutes said, “Almost all participants thought that it would be desirable to announce before too long a plan to stop reducing the Federal Reserve’s asset holdings later this year.”

The Fed’s willingness to end its balance sheet reduction program later this year is a remarkable turnaround from Fed Chair Powell’s comment after the December FOMC meeting that the balance sheet program was on autopilot with essentially no end in sight. The Fed seemed to shift its position on its balance sheet after the sharp drop in stock prices in Q4-2018 was partially blamed on the Fed’s balance sheet reduction program.

The link between the Fed’s balance sheet and the stock market is highly tenuous. Nevertheless, during the days of QE, the markets were convinced that the increase in permanent liquidity was supportive for the stock market and asset prices in general, which in turn supported household wealth and consumer-business confidence. If true, then the corollary must be true as well, i.e., that the current decline in liquidity is bearish for the stock market and asset prices.

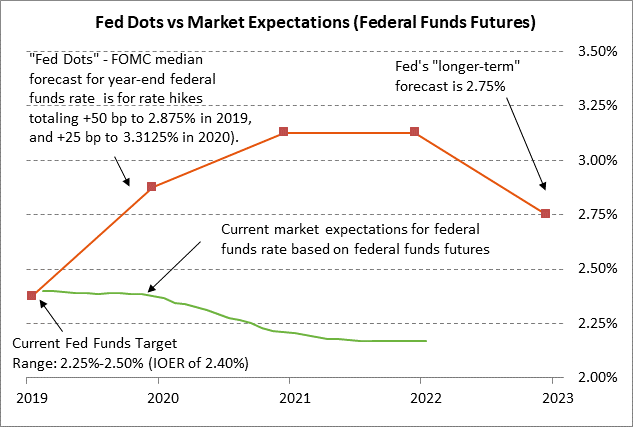

Market participants will now turn their attention to the next FOMC meeting March 19-20. The FOMC at that meeting will release an updated set of Fed-dot forecasts, which will show whether FOMC members believe that the Fed’s rate-hike cycle is finished or whether they expect to resume raising interest rates once the current global uncertainty abates. The last set of Fed dots showed a median expectation of two more rate hikes in 2019 and a third rate hike in 2020, which would push the funds rate target range up to 3.00%/3.25% by late 2020.

US/Chinese high-level trade talks resume today — The Thursday/Friday trade talks among top U.S. and Chinese officials begin today in Washington. The talks will be led by USTR Lighthizer and Chinese Vice Premier Liu. The market consensus seems to be that the two sides are still too far apart for a final agreement, but that there has been enough progress for President Trump to extend next Friday’s March 1 tariff deadline.

Bloomberg reported last week that President Trump is considering a 60-day extension of the March 1 deadline. Mr. Trump on Tuesday fueled further speculation that he is willing to extend the deadline when he said that there is nothing “magical” about the March 1 deadline. However, there is also the chance that Mr. Trump may go ahead with a tariff hike after March 1 if he thinks it is necessary to shake loose more concessions from China on the tough structural issues.

EU-UK are reportedly working on compromise backstop language — The EU and UK are already working on compromise language on the Irish backstop, according to comments that Spain’s foreign minister made to Bloomberg on Wednesday. Brexit Secretary Barclay and Attorney General Cox will be in Brussels today to discuss compromise language. It remains to be seen whether the EU is willing to go far enough on a backstop compromise to satisfy the UK Parliament. Ms. May’s government is racing to get some kind of compromise that it can present to Parliament before next Wednesday’s Brexit vote, in which Parliament might adopt the Cooper-Boles amendment that would extend the March 29 Brexit deadline if there is no Brexit agreement by March 13.

30-year TIPS auction — The Treasury today will auction $8 billion of newly-issued 30-year TIPS. The 30-year TIPS yield on Wednesday edged to a 5-month low and closed the day at 1.06%. The 12-auction averages are: 2.46 bid cover ratio, $13 million in non-competitive bids, 6.8 bp tail to the median yield, 18.3 bp tail to the low yield, and 62% taken at the high yield. The 30-year TIPS security is the most popular security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 73.2% of the last twelve 30-year TIPS auctions, which is well above the median of 61.9% for all recent Treasury coupon auctions.

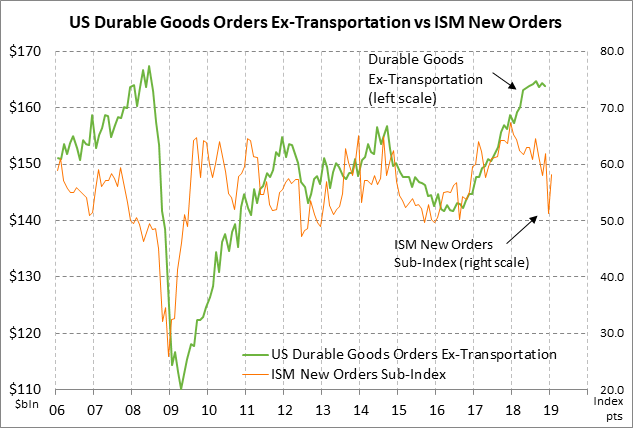

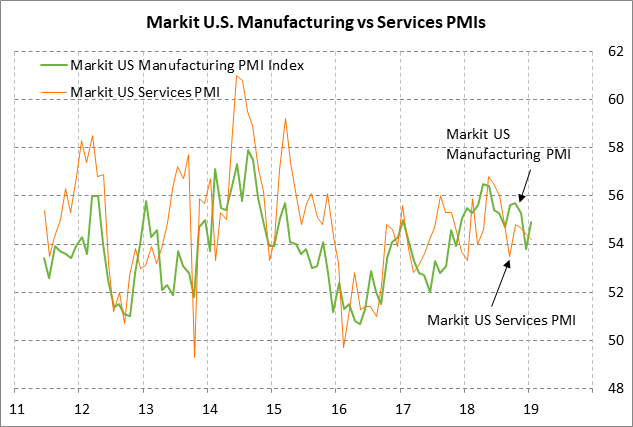

U.S. economic report deluge today — There is a deluge of U.S. economic data today, some on which was delayed by the Dec/Jan U.S. government shutdown. Dec durable goods orders are expected to improve to +1.7% and +0.3% ex-transportation from Nov’s report of +0.4% and -0.4% ex-transportation. Today’s Jan leading indicators report is expected to show a small +0.1% m/m rise, reversing Dec’s -0.1% decline. Today’s Jan existing home sales report is expected to show a small +0.2% increase to 5.00 million units, stabilizing after December’s -6.4% decline to 4.99 million. The prelim-Feb Markit manufacturing PMI is expected to show a -0.1 point decline to 54.8 (after Jan’s +1.1 to 54.9) and the services PMI is expected to show a +0.1 point increase to 54.3 (after Jan’s -0.2 to 54.2). Initial claims are expected to fall -11,000 to 228,000 while continuing claims are expected to fall -30,000 to 1.743 million.