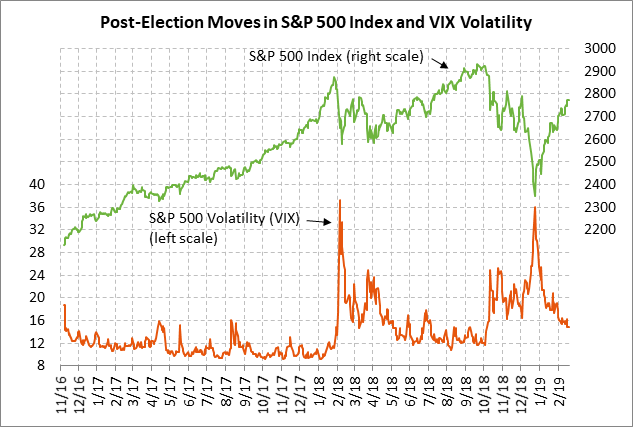

- Weekly global market focus

- President Trump receives auto import tariff recommendation from Commerce Dept

- US/Chinese trade talks continue this week in Washington ahead of next Friday’s deadline

- PM May faces deadline of next Wednesday for Brexit deal progress

- Q4 earnings season winds down

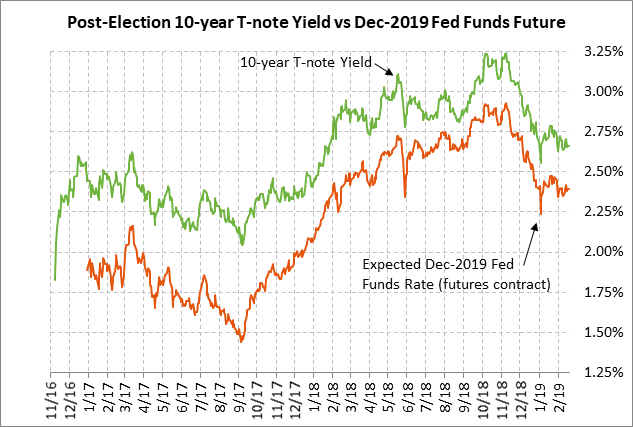

Weekly global market focus — The U.S. markets this week will focus on (1) trade tensions as the US/Chinese talks resume this week and as the markets await news as to whether the Commerce Department in Sunday’s report recommended tariffs on U.S. auto imports, (2) continued analysis of the Fed’s rate-hike pause with five speaking engagements this week by Fed officials and with Wednesday’s release of the minutes from the Jan 29-30 FOMC meeting, (3) the tail end of Q4 earnings season as 51 of the S&P 500 companies report this week, and (4) the Treasury’s sale of 2-year floating-rate notes on Wednesday and 30-year TIPS on Thursday.

In Europe, the focus is on (1) whether President Trump will impose tariffs on European autos, and (2) Brexit developments ahead of next week’s key vote in Parliament. The Euro Stoxx 50 index on Monday edged to a new 3-1/4 month high and closed mildly higher by +0.11%, building on last Friday’s +1.84% rally. European stocks on Monday were supported by Monday’s rally in Asian stocks, but were held back by weakness in European auto stocks on concern that the U.S. might impose tariffs on European autos.

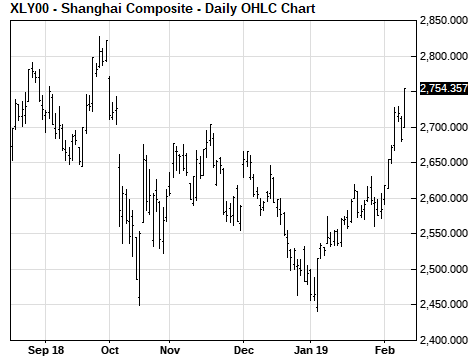

In Asia, the Shanghai Composite index on Monday rallied sharply by +2.68% and posted a new 4-1/2 month high. Chinese stocks were boosted by (1) claims by Presidents Trump and Xi that US/Chinese trade talks are progressing well, (2) last Friday’s news that Chinese new yuan loans rose by a record +3.230 trillion yuan (vs expectations of +3.0 trillion), which indicated that the PBOC’s monetary stimulus is bearing fruit with higher bank lending, and (3) short-covering and new technical buying with the breakout to a new 4-1/2 month high in the Shanghai Composite index.

President Trump receives auto import tariff recommendation from Commerce Dept — President Trump on Sunday received the Commerce Department’s recommendation on whether he should impose tariffs or quotas on U.S. auto imports on national security grounds. The recommendations have yet to be made public but will likely leak soon. The President has 90 days to act on the recommendations.

Europe seems to be assuming that the Commerce Department indeed recommended tariffs on U.S. auto imports since the EU has stepped up its threats of retaliation. An EU spokesman on Monday said that if the U.S. hits European autos with an import tariff, the EU will “react in a swift and adequate manner.” The EU has already prepared a list of $23 billion of U.S. products that will be hit with retaliatory tariffs if the U.S. goes through with tariffs on European autos, which are much higher than the tariffs on 2.8 billion euros of U.S. products that the EU imposed in retaliation for U.S. tariffs on European steel and aluminum.

US/Chinese trade talks continue this week in Washington ahead of next Friday’s deadline — US/Chinese talks will continue this week in Washington. The White House on Monday said that there will be deputy-level talks on Tuesday and Wednesday and then principal-level talks starting on Thursday led by USTR Lighthizer and Chinese Vice Premier Liu. The presence of Lighthizer/Liu is encouraging since they are the top US/Chinese negotiators with the most authority to act beneath Presidents Trump-Xi.

The U.S. and China are still far apart on key issues, according to most accounts, which means the odds appear slim for a final agreement by next Friday’s deadline. Indeed, President Trump has said that a final deal would not happen until he and President Xi meet in person and there is no such meeting scheduled at this point. However, President Trump over the weekend expressed optimism about the trade talks after being briefed by his team on Saturday, saying that last week’s talks were “very productive.” Chinese President Xi was also expressed optimism by saying that last week’s talks “achieved important progress in another step.”

Bloomberg last week reported that President Trump is considering a 60-day extension of the March 1 deadline for raising tariffs to 25% from 10% on $200 billion of Chinese goods. However, there is also the possibility that Mr. Trump might go ahead with the tariff hike next week to try to shake loose more concessions from China on the difficult structural issues.

PM May faces deadline of next Wednesday for Brexit deal progress — Prime Minister May this week will continue pressuring the EU for concessions on the Irish border backstop. However, she has only until next Wednesday (Feb 27) before she faces new Brexit votes in Parliament.

There is the possibility that Ms. May’s entire Brexit strategy could go up in smoke next Wednesday if Parliament were to approve the Cooper-Boles amendment, which provides for an extension of the March 29 Brexit date if Parliament cannot approve a Brexit separation agreement by March 13. If Parliament approves the Cooper-Boles amendment, then the Brexit deadline delay will almost certainly be activated because Parliament will not have the threat of a no-deal Brexit to force agreement to Ms. May’s Brexit plan, which is disliked by nearly everyone. The betting odds for a no-deal Brexit by April 1 remain unchanged at 7/4 (37% probability), according to oddschecker.com.

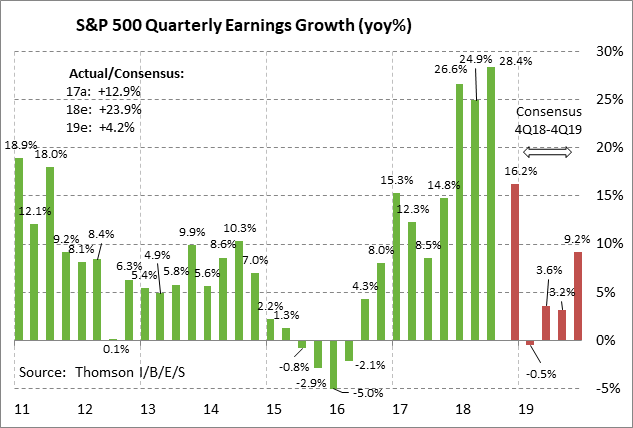

Q4 earnings season winds down — Q4 earnings season is winding down with 51 of the S&P 500 companies reporting this week. Of the 394 SPX companies that have so far reported, 69.5% have beaten earnings according to Thomson Reuters Refinitiv, above the long-term average of 64% but below the 4-quarter average of 78%.

After strong Q4 earnings growth near +16.2% y/y, the consensus is for SPX earnings growth in Q1 to fall to -0.5% y/y as the tax-cut effects fade. The consensus is for SPX earnings in 2019 to ease to +4.2% from +23.9% in 2018.