- State of the Union address will be watched for any news on government shutdown potential and US/Chinese trade

- ISM non-manufacturing index expected to show another decline but remain in generally strong shape

- 3-year T-note auction to yield near 2.52%

State of the Union address will be watched for any news on government shutdown potential and US/Chinese trade — The markets will be listening to tonight’s State of the Union address by President Trump for several key issues: (1) wall funding and the possibility of another government shutdown next Friday, (2) US/Chinese trade talks, and (3) any revived infrastructure proposal. Mr. Trump could revive his campaign against any new interest rate hikes from the Fed although that seems unlikely in the formal setting of the State of the Union address.

Regarding the US/Chinese trade talks, the markets will watch to see if Mr. Trump has any new announcements, such as a formal announcement of a Trump/Xi summit meeting in late February. The two presidents at that meeting could either announce a completed trade agreement or a kick-start for continued negotiations on the more difficult structural issues. The definitive scheduling of a Trump-Xi meeting would be a favorable sign since neither of the leaders would presumably want to show up for a meeting that ends in failure. The South China Morning Post this past Saturday reported that a Trump-Xi meeting is being considered for February 27-28 in Vietnam.

Regarding border wall funding, the markets will be listening for any hints about whether Mr. Trump will shut down the government again on February 15 when the continuing resolution expires. There is a Congressional panel that is working on a bipartisan compromise on border security, but Mr. Trump has said that they are wasting their time if they don’t produce his wall funding.

If Congress doesn’t agree to provide wall funding, then Mr. Trump has only three basic choices: (1) take whatever Congress will give him on border security and give up on the wall funding for now, (2) shut down the government again on February 15 to see if he can get House Democrats to cave in on wall funding the second time around, or (3) declare a border emergency and try to use military or disaster-relief money to pay for the wall.

Regarding the topic of infrastructure, Mr. Trump will reportedly stress the need for bipartisan cooperation in his speech, which means he may also revive his proposal for a big infrastructure program since that has some bipartisan appeal. The stock market would be pleased by any new fiscal stimulus from infrastructure spending but the Treasury security market will not be happy if the program is paid for by even higher Treasury borrowing.

The odds of an infrastructure program passing Congress are low, however, because there will be opposition to any new spending from Senate Republicans in particular. The CBO is already forecasting a budget deficit in 2019 of about $900 billion, rising to more than $1 trillion per year beginning in 2022.

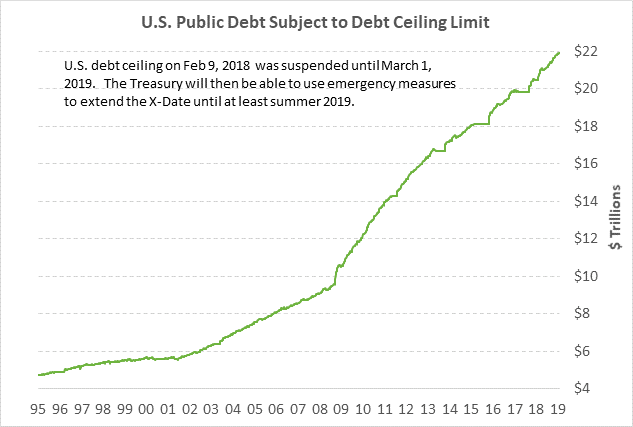

The U.S. public debt has reached a record $22 trillion, which is 2.5 times higher than the $8 trillion level seen before the 2007/09 global financial crisis and Great Recession. The U.S. federal debt held by the public is currently at 79% of U.S. GDP. The CBO is projecting a rise in the public debt to 93% of GDP in 2029 and to an unsustainably high 150% of GDP by 2049, as seen in the nearby chart.

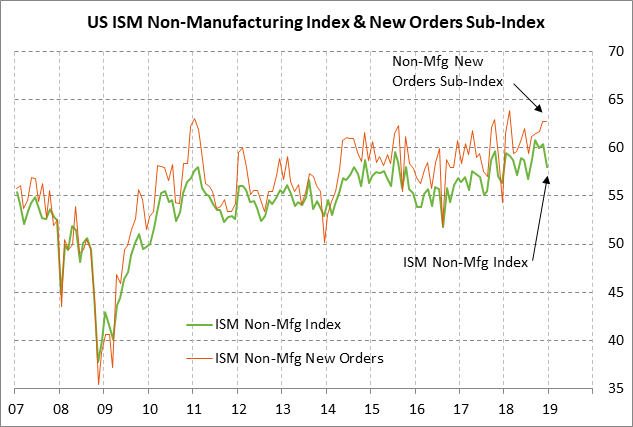

ISM non-manufacturing index expected to show another decline but remain in generally strong shape — The market consensus is for today’s Jan ISM non-manufacturing index to show a -0.9 point decline to 57.1, adding to December’s -2.4 point decline to 58.0. Despite expectations for another decline today, the expected index level of 57.1 would still be relatively strong and would indicate general business optimism in the non-manufacturing sectors of the U.S. economy. December’s index level of 58.0 was only 2.8 points below the 13-year high of 60.8 posted in Sep 2018.

There are reasons for U.S. business to be skeptical about the near-term economic outlook including (1) expectations for slower GDP growth in 2019, (2) trade tensions and the higher business costs from paying U.S. tariffs and the damper on some U.S. exports caused by retaliatory tariffs, (3) stock market volatility and the Q4 stock market correction, and (4) the possibility of another government shutdown on February 15. Despite these negative factors, U.S. business confidence in general remains solid since (1) the U.S. economy continues to grow at a solid pace, (2) the Fed has stopped its interest-rate hike regime, and (3) the stock market recovered nicely in January.

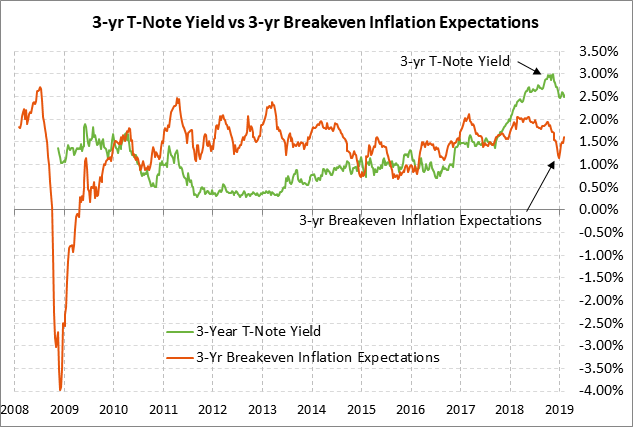

3-year T-note auction to yield near 2.52% — The Treasury today will sell $38 billion of 3-year T-notes. The Treasury will then continue this week’s $84 bln refunding operation by selling $27 bln of new 10-year T-notes on Wed and $19 bln of new 30-year T-bonds on Thursday. The 3-year T-note yield late Monday was trading at 2.52%, up by +18 bp from the early-Jan 10-month low of 2.34%.

The size of this week’s 3, 10 and 30-year auctions are the same as the comparable prior auctions. The Treasury has now raised the sizes of its coupon auctions by enough to cover the higher U.S. budget deficit, which gives the T-note and T-bond market some relief. The Treasury raised the 3-year T-note to the current level of $38 billion from only $24 billion as recently as a year ago.

The 12-auction averages for the 3-year are: 2.70 bid cover ratio, $88 million in non-competitive bids, 3.4 bp tail to the median yield, 18.8 bp tail to the low yield, and 54% taken at the high yield. The 3-year is the second least popular coupon security behind the 2-year among foreign investors and central banks with indirect bidders taking an average of only 46.8% of the last twelve 3-year T-note auctions, well below the average of 61.9% for all recent coupon auctions.