- Markets are undercut as Powell says balance sheet will become “substantially smaller”

- Odds improve for an end to the shutdown as Trump moves toward emergency declaration

- CPI report will hint at how much room Fed has to pause

Markets are undercut as Powell says balance sheet will become “substantially smaller” — The stock market on Thursday turned lower after Fed Chair Powell in a question-and-answer period at the Washington Economic Club said that the Fed’s balance sheet “will be substantially smaller than it is now,” though bigger than it was before the crisis.

The markets after the Dec 18-19 FOMC meeting reacted negatively when Mr. Powell said that the Fed’s balance sheet reduction program is on auto-pilot and that the Fed does not plan to use it to adjust monetary policy, leaving that role to the federal funds rate. Mr. Powell last Friday then eased up a bit on that statement by saying that the balance sheet program could always be adjusted depending on circumstances. However, Mr. Powell on Thursday returned to his hawkish auto-pilot view when he said that the Fed will continue driving the balance sheet lower to a “substantially smaller” level.

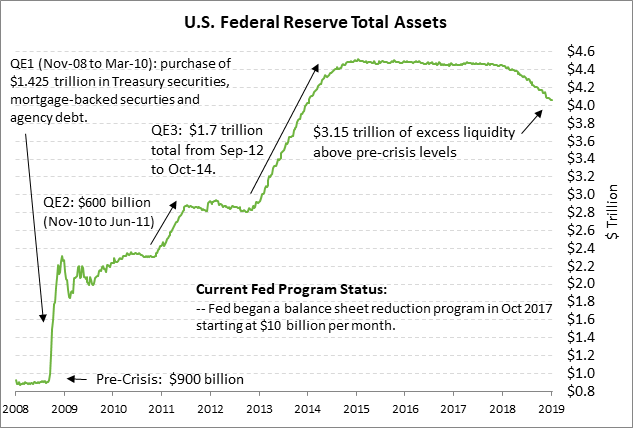

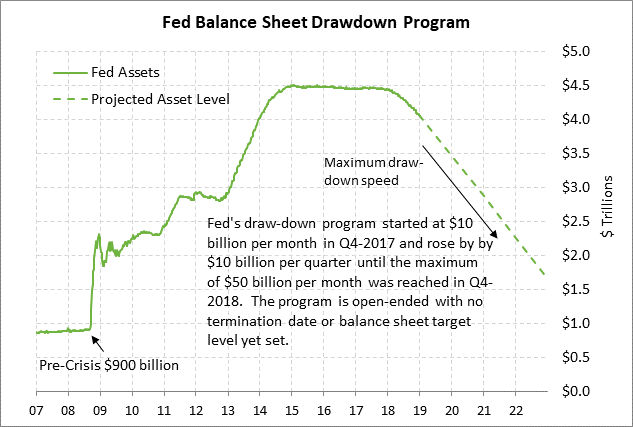

The Fed is currently allowing its balance sheet to decline at a maximum rate of $50 billion per month as securities mature in its portfolio without replacement. The Fed’s balance sheet has so far fallen by $460 billion (-10.2%) to $4.057 trillion from its maximum level of $4.5l6 trillion posted in Jan 2015 and by $399 billion (-9.0%) from October 2017 when the Fed’s balance sheet drawdown program began.

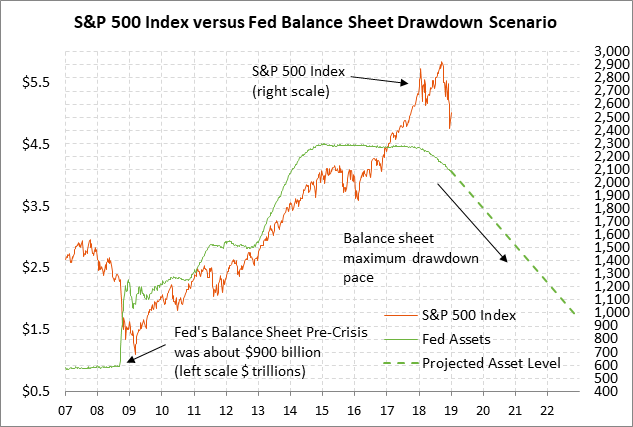

The Fed has not yet identified its eventual target for the balance sheet since that depends in part on whether the Fed decides it wants to use a floor or a corridor policy for running monetary policy. However, there is speculation that the Fed’s eventual balance sheet level will be on the order of $2.5-3.0 trillion. If true, that would mean that the Fed still has at least another 2-3 years of drawdown left at the current drawdown rate. The markets are therefore far too premature if they are hoping that the Fed is going to dial back its drawdown program anytime soon.

On the more dovish side, Mr. Powell on Thursday clearly reiterated that the Fed is on hold and that future actions are fully data-dependent. Mr. Powell said, “We’re in a place where we can be patient and flexible and wait and see what does evolve, and I think for the meantime we’re waiting and watching.” For good measure he added, “You should anticipate that we’re going to be patient and watching and waiting and seeing.” The market is currently discounting essentially no funds rate change in 2019 and a 50% chance of a rate cut in 2020.

Odds improve for an end to the shutdown as Trump moves toward emergency declaration — President Trump on Thursday said that it would be “surprising to me” if he doesn’t make an emergency declaration on the border if talks with the Democrats fail. The emergency option now seems to be the only solution for reopening the government. The White House and Democrats show no signs of moving an inch off their positions and talks among Senators about a larger immigration deal are falling flat.

Mr. Trump could make the emergency declaration as soon as today or this weekend in order to get the shutdown over with by early next week so he doesn’t have to incur another week of negative shutdown news. Many federal workers will miss their first paycheck today and the shutdown by tomorrow will become the longest in U.S. history. If agreed, the shutdown could end quickly since the Senate just needs to sign off on the spending bills already passed by the House and the President then just needs to sign those bills.

We continue to suspect that the markets would be pleased if Mr. Trump agrees to reopen the government after declaring an emergency on the border. The markets would be much happier about the government reopening than they would be worried about whatever the political uncertainty emerges from the declaration of a national emergency. The emergency declaration and wall funding would simply end up as a pinball in the courts with little implication for the markets.

White House economist Hassett has said that the shutdown is trimming U.S. GDP by 0.1 point every two weeks while other economists believe the impact is twice that much, plus the additional negative impact from reduced consumer, business, and investor confidence. Fed Chair Powell yesterday warned that a prolonged shutdown would hurt the U.S. economy. He also warned that the Fed is now flying partially blind because the Commerce Department cannot calculate and disseminate the retail sales and GDP reports.

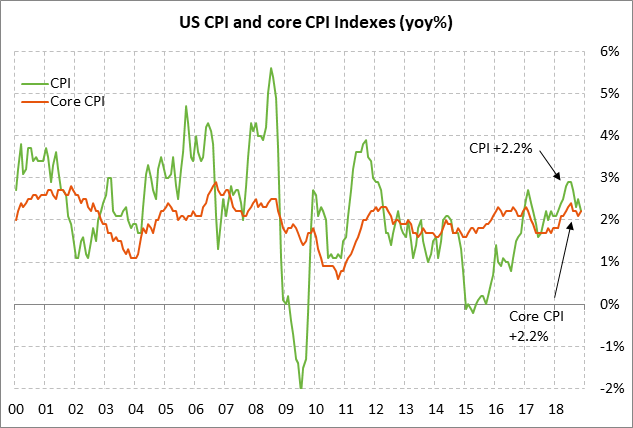

CPI report will hint at how much room Fed has to pause — Today’s CPI report will provide some incremental information on how much room the Fed has to pause its rate-hike regime. A recent theme from the Fed has been that the Fed has room to put its monetary policy on pause because of the tepid inflation situation.

However, the tepid view of the inflation comes mainly from the falling breakeven rate, not from the actual inflation statistics. Today’s Dec CPI is expected to edge lower to +1.9% y/y from Nov’s +2.2% due to lower oil prices, but the core CPI is expected to be unchanged from Nov’s +2.2% y/y, which is slightly above the Fed’s +2.0% inflation target. The Nov core PCE deflator is only in slightly better shape at +1.9%, or 0.1 point below the Fed’s inflation target.

By contrast, the 10-year breakeven inflation expectations rate has fallen sharply in recent weeks due to the plunge in oil prices and the talk about weaker global economic growth. The 10-year breakeven inflation expectations rate in early January hit a 1-1/2 year low of 1.67%, which was down by about 48 bp from late-September. The 10-year breakeven rate has since rebounded higher by +15 bp to 1.82% due to the upward rebound in both crude oil prices and U.S. stocks, but that is still well below the Fed’s inflation target.