- U.S. payroll growth expected to recover to +180,000 after Nov’s weak report

- White House meeting today could be make-or-break for the shutdown

- Eurozone core CPI expected stable

- Chinese bond yield falls to 2-year low as Chinese outlook darkens

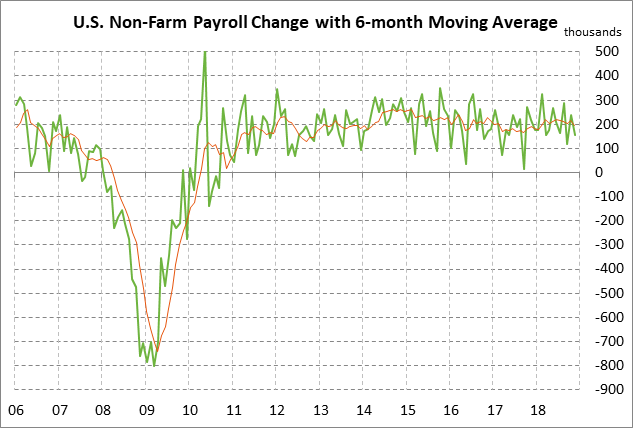

U.S. payroll growth expected to recover to +180,000 after Nov’s weak report — The market consensus is for today’s Dec payroll report to recover to +180,000 from Nov’s weak report of +155,000 but remain below the 12-month trend of +204,000. Expectations for today’s payroll report were bolstered by yesterday’s Dec ADP report of +271,000, which was well above market expectations of +180,000 and was the strongest report in nearly two years.

The market will be sensitive to any weakness in today’s payroll report given the recent concern about weaker economic growth. The recent global business confidence surveys have been weak, raising the possibility that businesses might turn cautious and start trimming their hiring plans. Indeed, Thursday’s Dec U.S. ISM manufacturing index fell by an alarming -5.2 points to 54.1, illustrating a sharp drop in manufacturing confidence. The new orders index plunged by -11.0 points to 51.1, indicating that U.S. manufacturers are seeing a sharp drop in orders as businesses turn more cautious about the economic outlook.

Hiring in any case is likely to downshift in 2019 due to slower U.S. GDP growth and already-high staffing levels. Since the Great Recession, U.S. businesses have hired a net 20.2 million new employees. A recent survey by Bloomberg found a consensus that payroll growth will downshift to an average monthly gain of +156,000 in 2019 from the 2018 level of +206,000. The markets will not be overly impressed with new payroll reports in the area of +156,000.

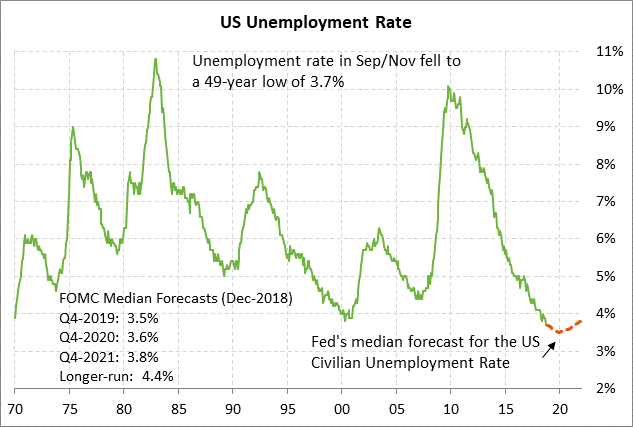

The consensus is for today’s Dec unemployment rate to be unchanged from the 49-year low of 3.7% seen over the past three months. The Fed is forecasting a further -0.2 point drop in the unemployment rate to 3.5% by late this year and then a small rise to +3.6% by late-2020 and 3.8% by late-2020. However, the unemployment rate over the next several years is expected to remain well below the Fed’s estimate of a long-term natural unemployment rate of 4.4%, indicating a tight labor market.

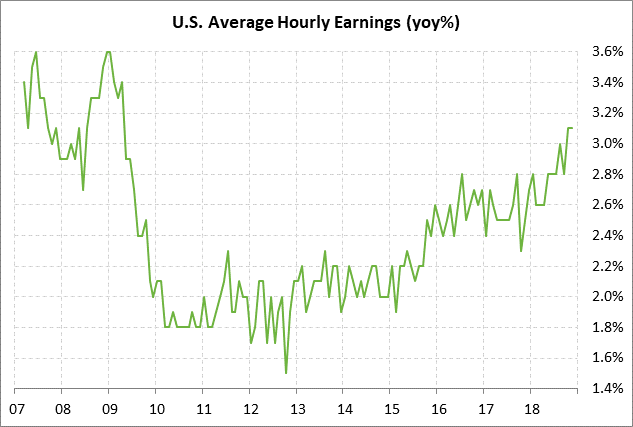

The tight labor market is expected to keep upward pressure on employee wages and salaries even as U.S. economic growth slows this year due to fading tax-stimulus. The consensus is for today’s Dec average hourly earnings report to ease slightly to +3.0% y/y from the 9-1/2 year high of +3.1% posted in October and November. The +3.1% increase in average hourly earnings in November, and the more general +4.2% y/y rise in November personal income, illustrates that the strong labor market is delivering cash and spending power to consumers.

White House meeting today could be make-or-break for the shutdown — Now that the new Congress has been sworn in and Nancy Pelosi has become the new House Speaker, the time has come to see whether there is any escape route from the partial government shutdown. President Trump will meet with Congressional leaders at the White House today for a negotiating session beginning at 11:30 AM ET.

If there is no progress at today’s meeting, then the markets could be in for a long shutdown since the political situation will not change much in coming days. President Trump and Congressional Democrats have backed themselves into opposing corners and any compromise would draw backlash from their respective bases. In the meantime, White House Chair of the White House Council of Economic Advisors Kevin Hassett on Thursday said that the partial government shutdown is trimming U.S. GDP growth by about 0.1 point every two weeks. The shutdown is already at the 2-week mark.

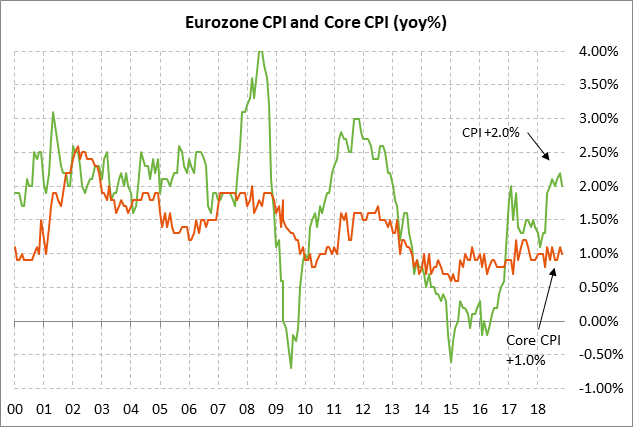

Eurozone core CPI expected stable — The market consensus is for today’s Eurozone Dec CPI report to ease to +1.8% y/y from November’s +2.0% mainly because of the recent plunge in crude oil and fuel prices. However, the Dec core CPI is expected to be unchanged at +1.0% y/y.

The Eurozone core CPI has been locked in the narrow range of 0.7%-1.2% for the past several years despite the ECB’s QE program and zero interest rates. By ending its QE program on Dec 31, the ECB gave up on using bond-buying to boost inflation to its inflation target of just below 2%. The ECB is now hoping that it can eventually boost inflation by keeping interest rates near zero. The ECB has promised to leave rates at current levels at least through this summer, but the market is not fully expecting a rate hike until next year.

Chinese bond yield falls to 2-year low as Chinese outlook darkens — The Chinese 10-year government bond yield on Thursday fell to a new 2-year low of 3.17%. The Chinese 10-year bond yield has plunged by -17 bp just in the past week on the spate of weak global economic data. The Chinese bond yield on Thursday fell after Apple late Wednesday warned of a sharp downward revision in iPhone sales tied to unexpected weakness in spending in China. The markets were already in a sour mood about Chinese economic growth after the weak Chinese manufacturing PMI figures released earlier in the week.

The Chinese 10-year bond yield also fell after China’s central bank announced that a lower Required Reserve Ratio will be applied to more banks, thus freeing up more reserves for banks to boost lending to businesses and consumers. The markets are expecting two or three RRR cuts this year from the People’s Bank of China as a means to ease monetary policy without directly cutting short-term interest rates, which would risk hurting the yuan and causing capital flight.

The Chinese bond yield also fell in sympathy with this week’s sharp drop in U.S. and German bond yields. The 10-year German bund yield on Thursday fell by -1 bp to a 2-year low of 0.15% and the 10-year T-note yield fell by -7 bp to a 1-year low of 2.55%.