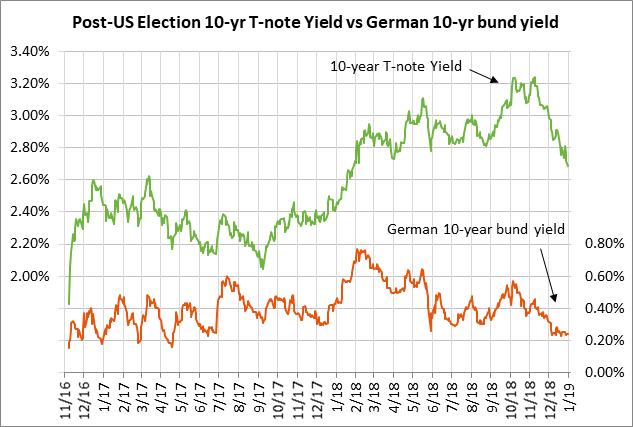

- U.S. and German yields hit new 1-2 year lows on weaker economic outlook and safe-haven

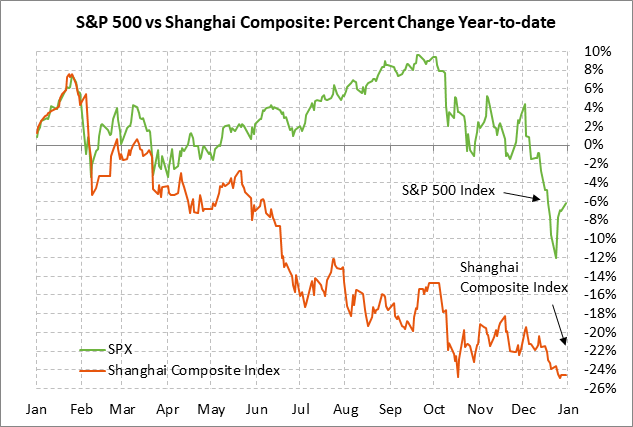

- Chinese and Hong Kong stocks sink on poor Chinese mfg PMIs

- New Congress takes power today with no progress on ending U.S. government shutdown

- U.S. ADP report expected to be stable at +180,000

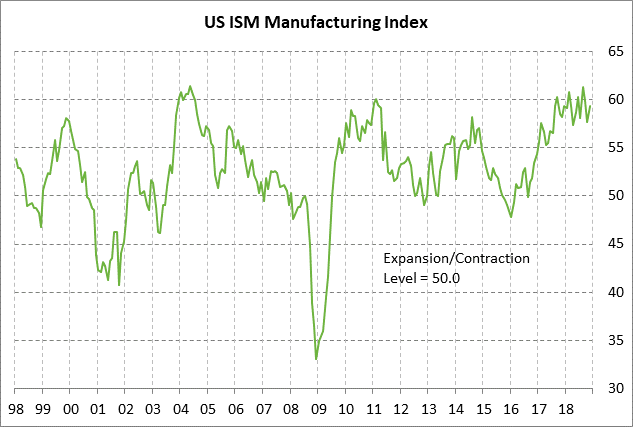

- U.S. ISM manufacturing index expected to weaken

U.S. and German yields hit new 1-2 year lows on weaker economic outlook and safe-haven — The 10-year German bund yield on Wednesday tumbled by -8 bp to a 2-year low of 0.15% and the 10-year T-note yield fell by -6 bp to a 1-year low of 2.62%. The new lows illustrate the market’s deteriorating outlook for the global economy and the more dovish view of central bank policy. The ECB has ended its QE program but will keep its balance sheet constant for at least the next two years and a rate hike isn’t likely until 2020. The federal funds futures market believes that the Fed’s rate-hike regime is already over and is discounting a 90% chance of a Fed rate cut in 2020.

The decline in government bond yields is also being driven by safe-haven demand from (1) global trade tensions as the March 1 deadline approaches for a US/Chinese trade agreement and as the US-Japan and US-EU tariff ceasefires are on shaky ground, (2) the possibility of a meltdown in China as the economy slows with heavy corporate and household debt burdens, (3) the lack of a Brexit solution ahead of the March deadline, and (4) Washington political uncertainty on talk that Special Counsel Mueller could release a report as soon as February and as House committees gear up to investigate President Trump and his administration.

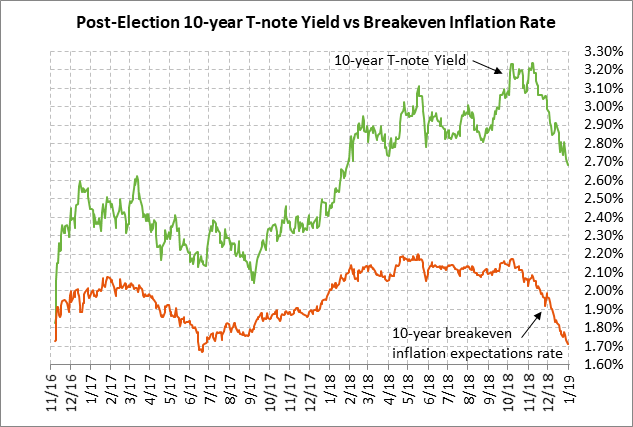

World bond yields are also falling due to sharply lower inflation expectations driven by the plunge in oil prices and expectations for weaker global economic growth. The U.S. 10-year breakeven inflation expectations rate on Wednesday fell to a new 1-1/2 year low of 1.69%. The German 10-year breakeven rate on Wednesday matched the 2-year low of 0.92% posted in June 2017.

Chinese and Hong Kong stocks sink on poor Chinese mfg PMIs — The Shanghai Composite index on Wednesday fell by -1.15% and the Hong Kong Hang Seng fell by -2.77% due to increased concern about slower Chinese economic growth after the weak Dec manufacturing PMI reports. China’s national Dec manufacturing PMI on Sunday night fell by -0.6 points to a 2-3/4 year low of 49.4, which was substantially weaker than expectations of unchanged at 50.0. The Caixin Dec Chinese manufacturing PMI report on Tuesday night then fell by -0.5 points to a 1-1/2 year low of 49.7, weaker than expectations of unchanged at 50.2. Both the national and Caixin manufacturing PMI’s are now below the expansion-contraction level of 50.0, suggesting that China’s manufacturing sector is contracting.

The fact that the US/Chinese trade war is partially behind the slowdown is seen by the fact that the national China manufacturing export orders sub-index fell by -0.4 points to a 3-year low of 46.0, remaining below the expansion-contraction level of 50.0 for the seventh consecutive month.

There was some good news in Sunday night’s national PMI report since the Dec non-manufacturing PMI rose by +0.4 points to 53.8, stronger than expectations of -0.2 to 53.2. However, Thursday night’s Dec Caixin Chinese services PMI is expected to fall -0.8 points to 53.0, painting a weaker picture for China’s service sector.

Concern about slower Chinese and global growth was also fueled on Wednesday by Apple’s warning of slower sales tied in part to lower phone demand in China.

New Congress takes power today with no progress on ending U.S. government shutdown — The new Congress begins today at noon ET. The new Democratically-controlled House on Thursday or Friday is expected to vote on bills seeking to reopen the government. The House is expected to pass continuing resolution until Feb 8 for the Department of Homeland Security and spending bills for the remainder of the fiscal year covering the other agencies that are currently closed. None of those bills will include President Trump’s demand for $5 billion in wall funding.

The House bills are expected to quickly die in the Senate since Senate Majority Leader McConnell has said that the Senate will not vote on a bill until there is a bipartisan agreement between the White House and Democrats that can get 60 votes in the Senate for cloture.

The White House scheduled a second meeting with Congressional leaders on Friday after Wednesday’s border security briefing ended with no apparent progress. After Wednesday’s meeting, Mr. McConnell raised the possibility of the shutdown lasting for weeks, telling reporters, “It was a civil discussion. We’re hopeful that somehow in the coming days and weeks we’ll be able to reach an agreement.”

U.S. ADP report expected to be stable at +180,000 — The market consensus is for today’s Dec ADP employment report to show a solid increase of +180,000, which would be very close to Nov’s report of +179,000 but weaker than the 12-month trend average of +202,000. The market is mainly looking ahead to Friday’s Dec payroll report, which is expected to rebound higher to +180,000 from Nov’s weak +155,000 report but remain below the 12-month trend of +204,000. Job growth is seeing some weakness in interest-rate-sensitive sectors such as housing and autos. The markets will be on guard for a weaker-than-expected payroll report on Friday, which would fuel fears that the stock market correction is causing businesses to lose confidence and trim their hiring plans.

U.S. ISM manufacturing index expected to weaken — The consensus is for today’s Dec ISM manufacturing index to fall by -1.8 points to 57.5, more than reversing Nov’s unexpected +1.6 point increase to 59.3. Today’s expected report of 57.5 would still be a strong level that indicates optimism about the manufacturing sector. However, there is room for a weaker-than-expected ISM report today given the weakness in overseas PMIs and the ongoing U.S. stock market correction that is dampening American business confidence.