- U.S. stocks appear to set near-term low

- Congress returns to session today but chances appear dim for a breakthrough on the U.S. government shutdown

- U.S. consumer confidence expected to remain strong

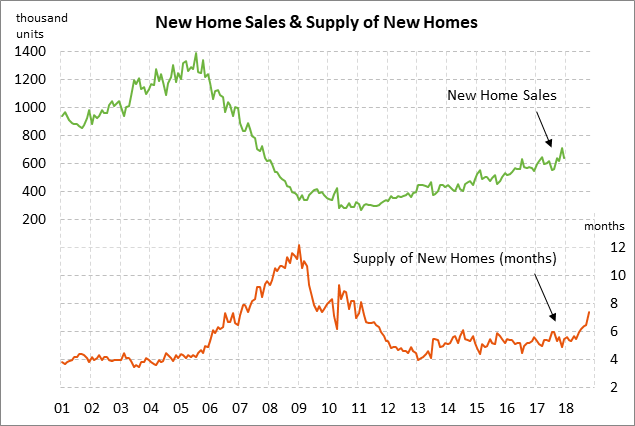

- U.S. new home sales expected to rebound from 2-1/2 year low

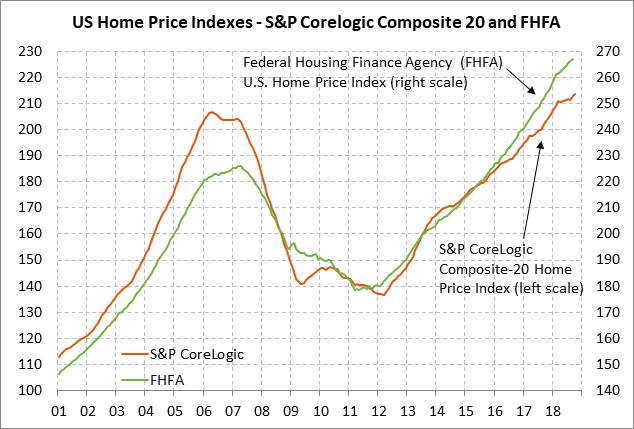

- U.S. home prices expected to moderate

- U.S. unemployment claims expected to remain favorable

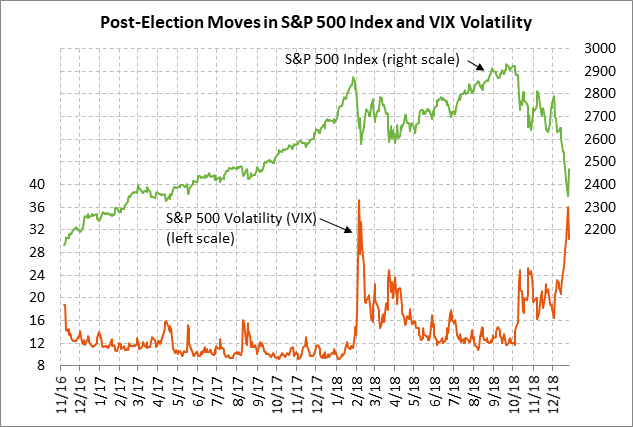

U.S. stocks appear to set near-term low — The S&P 500 index on Wednesday soared by +4.96%, reversing the losses seen in the two previous sessions but still showing a month-to-date loss for December of -10.6%. The Nasdaq 100 index on Wednesday closed +6.16% higher and the Dow Industrials closed up +4.98%. The size of Wednesday’s rally was large enough to suggest that the U.S. stock market has found at least a near-term bottom.

Stocks got off to a good start on Wednesday after Chairman of the White House Council of Economic Advisors Kevin Hassett told reporters that “yes, of course, a hundred percent” that Fed Chair Powell’s job is safe. Mr. Hassett also said that U.S. banks are not facing a liquidity crisis, soothing concerns that arose after Treasury Secretary Mnuchin did a welfare check this past weekend with the CEOs of the six largest U.S. banks.

Other bullish factors on Wednesday included (1) cheap stock valuations after the recent plunge, and (2) afternoon news that mid-level U.S. trade negotiators will travel to China in the week of January 7 for trade talks. Those will be the first face-to-face trade talks since Presidents Trump and Xi agreed on a 3-month ceasefire on December 1 at their meeting in Buenos Aires, although there have been some recent trade discussions by phone. The bad news is that the 3-month ceasefire is already one-third over.

The broad U.S. stock market was also supported by a sharp rally in retail and energy stocks. The S&P 500 Retailing Index rallied by +7.4% on reports of very strong holiday spending. The S&P Energy Index rallied by +6.24% due to the +8.68% rally in Feb WTI oil prices. Oil prices rallied on the surge in the stock market and on short-covering sparked by Russian Oil Minister Novak’s comment that OPEC+ could meet at any time to discuss further production cuts if more cuts are necessary to balance the market.

Congress returns to session today but chances appear dim for a breakthrough on the U.S. government shutdown — About one-quarter of the U.S. government has been shut down since last Friday night when the continuing resolution expired. After the short holiday break, Congressional leaders and the White House today will resume negotiations on a deal to address President Trump’s demand for border wall financing in a new continuing resolution.

The Trump administration is reportedly ready lower its demand to $2.1 billion for a border wall from $5 billion but Democrats are still resisting. The House has already passed a continuing resolution with $5.7 billion in border wall and security funding, but the Senate cannot proceed with that bill since there is opposition from Democrats and there aren’t the 60 votes necessary for cloture as a precursor to an up-or-down vote on the bill.

House Majority Whip Steve Scalise’s office on Wednesday said that no House votes are expected on Thursday and that representatives will be given 24-hour notice when they need to return to Washington for a vote. Meanwhile, Senate Majority leader McConnell has said the Senate will not vote until there is a three-way border security deal among the White House, Republicans, and Democrats.

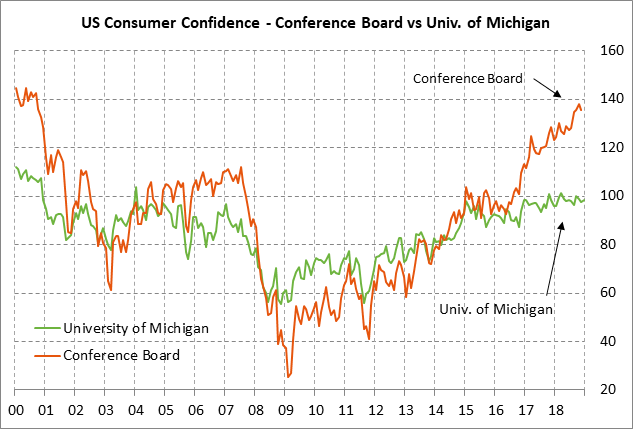

U.S. consumer confidence expected to remain strong — The market consensus is for today’s Dec Conference Board U.S. consumer confidence index to show a -2.2 point decline to 133.5, adding to November’s -2.2 decline to 135.7. A decline today in the Conference Board’s index would be at odds with the University of Michigan’s U.S. consumer sentiment index, which showed an unexpected +0.8 point increase to 98.3 in December. However, the Conference Board’s index has been much stronger than the University of Michigan’s index over the past two years, which means the Conference Board’s index has some room on the downside to deflate.

U.S. consumer confidence in general remains strong due to the (1) strong U.S. economy and labor market, (2) rising income and wages with Oct personal income up +4.3% y/y, (3) strong household wealth with the continued rise in U.S. home prices, and (4) the sharp decline in gasoline prices, which frees up cash for consumers to save, pay down debt, or buy other products. The main threat for consumer confidence is the recent plunge in the stock market, which is a negative sign for the economy and also reduces the value of consumers’ savings and 401k plans.

U.S. new home sales expected to rebound from 2-1/2 year low — The consensus is for today’s Nov new home sales report to show a +4.4% increase to 568,000, recovering about half of Oct’s -8.9% decline to a 2-1/2 year low of 544,000. New home sales were down -12.0% y/y in October mainly because of the poor affordability of new homes, caused by both higher mortgage rates and the sharp +50% rise in home prices seen since the financial crisis.

U.S. home prices expected to moderate — The consensus is for today’s Oct FHFA house price index to show an increase of +0.2% m/m, matching Sep’s report of +0.2% m/m. The FHFA home price index remained strong at +6.0% y/y in September. However, home prices are likely to cool somewhat in coming months due to resistance to high prices and the higher costs of mortgages.

.

.

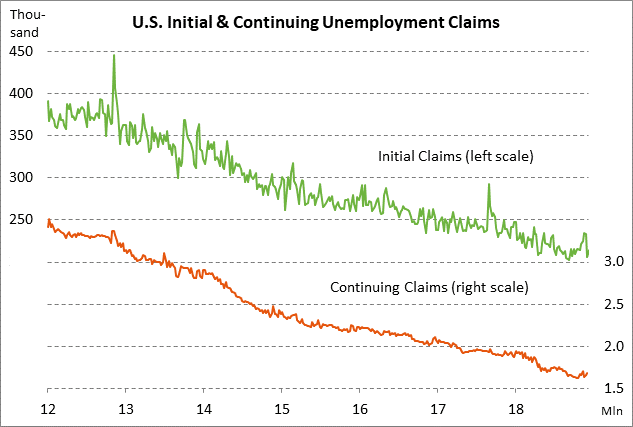

US. unemployment claims expected to remain favorable — The consensus is for today’s weekly initial unemployment claims report to show a small +2,000 increase to 216,000 (vs last week’s +8,000 to 214,000) and for continuing claims to fall -15,000 to 1.673 million (vs last week’s +27,000 to 1.688 million). The claims data remains in very favorable shape with layoffs near the lowest levels in more than four decades. Initial claims are only 12,000 above Sep’s 49-year low of 202,000 and continuing claims are only 58,000 above October’s 45-year low of 1.630 million.