- Shutdown mess is a preview of next year’s politics

- Nov deflator expected little changed but inflation expectations are crashing

- Personal income and spending expected to moderate

- U.S. consumer sentiment expected unchanged

- U.S. GDP headed lower after today’s report

Shutdown mess is a preview of next year’s politics — The stock market on Thursday fell sharply after President Trump said he would not sign a continuing resolution without his $5 billion in border wall funding. Congress had a simple plan to pass a CR until February 8 and then leave Washington for the holidays. However, President Trump knee-capped that plan after he received blow-back from his base about not getting his border wall funding. The House last night was then able to pass a bill with $5.7 billion in border wall funding. However, Senate Democratic leader Schumer then said the House plan was dead-on-arrival and that the Senate on Friday would simply kick back the previous plan to the House. Some Democratic votes are necessary for the CR in the Senate to avoid a filibuster.

If a CR is not passed today, then about 25% of the government will shutdown at midnight tonight, affecting about 100,000 federal employees. Once a shut down begins, it could easily last until the Democrats take over the House on January 3. However, the situation then will be even more intractable since Democrats will have control of the House.

The U.S. financial markets normally would not be too worried about a short shutdown in the federal government. However, the stock market was already in a bearish mood and Thursday’s shutdown threat was enough to spark a new down-leg in the stock market. The market is also worried that this shutdown could easily last until January. Once the shutdown begins, neither President Trump nor the Democrats will want to be seen as conceding.

Thursday’s political mess is a preview of how Washington political strife is about to get much worse in January when Democrats take power in the House. House Democrats will block any legislative agenda put forward by the White House or Senate Republicans and will also launch a multitude of investigations into the White House. The threat of government shutdowns will be one of the few levers available to force through any legislation next year.

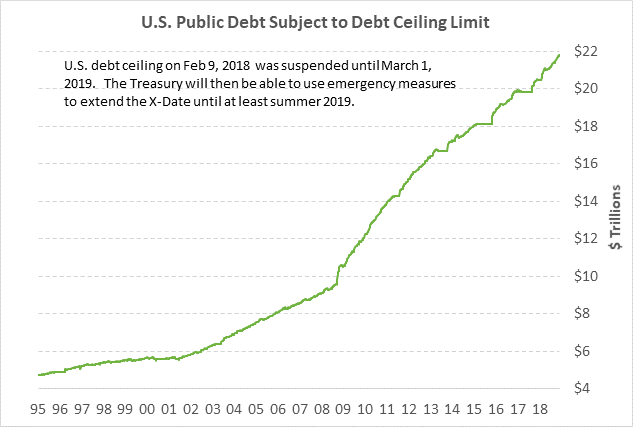

Even worse for the markets, Congress and the White House will need to pass a debt ceiling hike by next autumn. After the debt ceiling suspension expires on March 1, the Treasury is expected to be able to use its usual emergency procedures to last through summer 2019. However, the Treasury by autumn is expected to hit its X-date, which is when the threat will arise of a Treasury default.

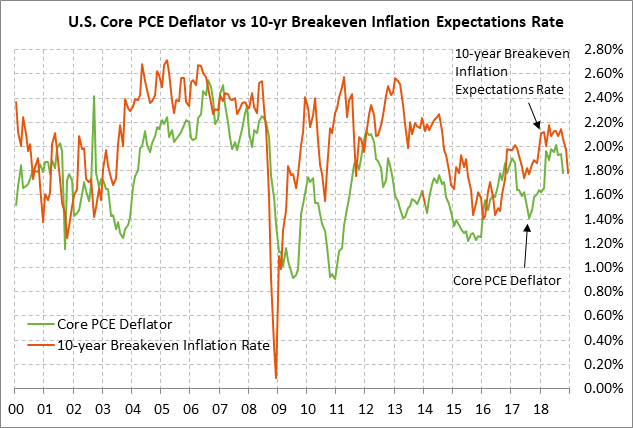

Nov deflator expected little changed but inflation expectations are crashing — The consensus is for today’s Nov PCE deflator to ease to +1.8% y/y from Oct’s +2.0% but for the core deflator to edge higher +1.9% y/y from Oct’s +1.8% y/y. Today’s expected report of +1.8% headline and +1.9% core would be the first time since February that both measures have been below the Fed’s +2.0% inflation target. The fact that the deflator is pointing downward is also seen by the fact that the core PCE deflator in October fell to a 1-1/2 year low of +1.1% on a 3-month annualized basis.

Not only are the deflator figures moving lower, but inflation expectations are crashing. The 10-year breakeven inflation expectations rate on Thursday fell to a new 15-month low of 1.78%, far below the Fed’s +2.0% inflation target. The breakeven rate has been falling mainly because of the plunge in oil prices. The fall in the breakeven rate, however, is also due to expectations for weaker global economic growth, which will put some downward pressure on prices.

The 10-year T-note yield has fallen sharply by -45 bp since early-Nov to the current level of 2.80%. The 10-year note yield has fallen mainly because of reduced expectations for Fed tightening since the market is now discounting only 0.5 rate hikes in 2019 versus expectations as recently as November for two rate hikes. However, the T-note yield has also fallen due to the sharp drop in inflation expectations.

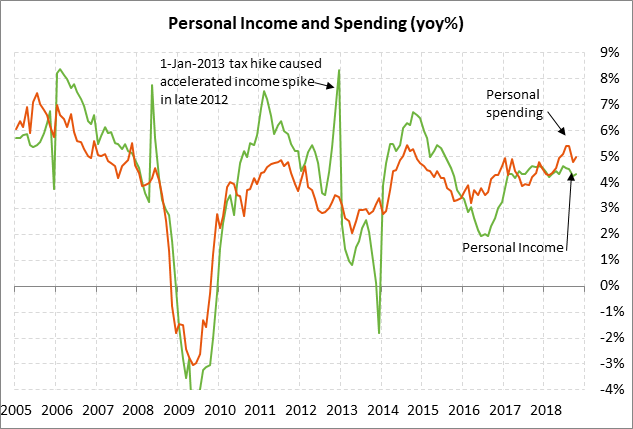

Personal income and spending expected to moderate — Today’s Nov personal income and spending reports are each expected to show increases of +0.3% m/m following Oct’s report of +0.5% and +0.6%, respectively. The expected reports of +0.3% would be respectable reports that indicate that consumers continue to see their income rising and continue to spend money at a decent pace. With an expected U.S. economic slowdown in 2019, the U.S. consumer will be more important than ever in keeping the U.S. economy afloat.

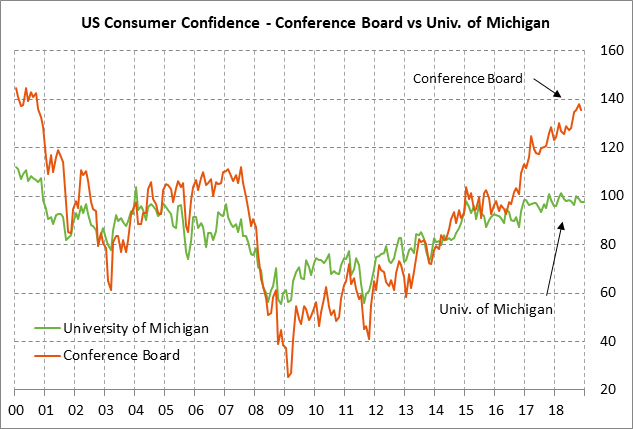

U.S. consumer sentiment expected unchanged — The consensus is for today’s final-Dec University of Michigan U.S. consumer sentiment index to be unrevised from the preliminary-Dec report of 97.5, which would leave the index unchanged from November’s level of 97.5. The index has fallen by a total of -2.6 points since September and fell to a 4-month low in November and early December. The main negative factor for consumer sentiment is the weak stock market, which fell sharply in October and again in December on a plethora of concerns including higher interest rates and trade tensions.

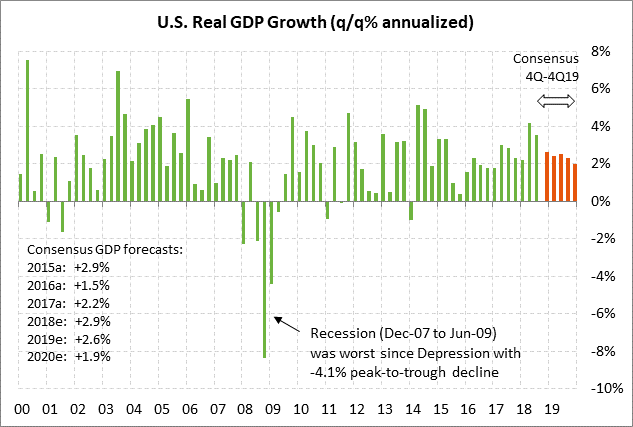

U.S. GDP headed lower after today’s report — The consensus is for today’s Q3 GDP report to be unrevised at +3.5% (q/q annualized) and for Q3 personal consumption to be unrevised at +3.6%. While U.S. GDP was very strong in Q2 (+4.2%) and +Q3 (3.5%), mainly due to the tax-cut stimulus, the days of above-3% GDP reports are over. The next GDP report in January for Q4 is expected at +2.6% and GDP is then expected to ease further to the +2.4% area in the first half of 2019. The stock market is more worried about weaker economic growth in 2019 than forecasters, who are not considering fuzzier factors such as falling investor confidence and the negative implications of a nearly-inverted yield curve.