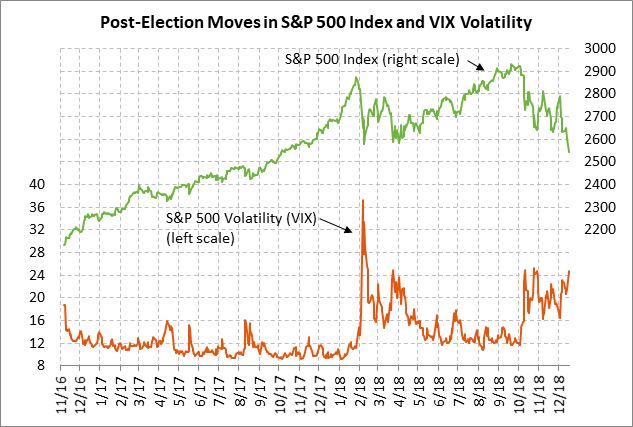

- S&P 500 falls to new 1-1/4 year low as bearish factors pile up

- Markets wait to see if FOMC will pause

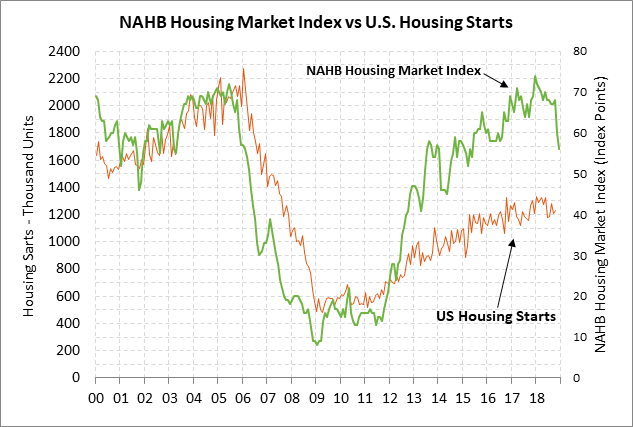

- U.S. housing starts outlook is undercut by a sharp drop in home builder confidence

S&P 500 falls to new 1-1/4 year low as bearish factors pile up — The S&P 500 index on Monday fell sharply to take out February’s low and post a new 1-1/4 year low. The index has now corrected lower by a total -13.95% from September’s record high, which is still within a correction range since it is less than a 20% bear market. The VIX on Monday closed at 24.52%, the highest close in 7 weeks and just 0.7 points below October’s 10-month highest close of 25.23%.

U.S. stocks on Monday were hammered mainly on fears of a “hawkish rate hike” by the FOMC on Wednesday, meaning a rate hike plus indications that more rate hikes are coming soon. However, some investors are holding out hope for a “dovish rate hike” whereby the FOMC raises the funds rate on Wednesday but gives some guidance that it might pause its rate hikes through perhaps mid-2019.

Other than a hawkish Fed, bearish factors for the U.S. stock market include (1) the possibility of a partial U.S. government shutdown on Friday night when the continuing resolution expires, (2) worries about the global economy after last week’s weak Chinese and European economic data, (3) a sharp drop in U.S. health care stocks on Monday after a Texas-based federal district court late last Friday ruled that key elements of Obamacare are unconstitutional, (4) strength in the dollar as the dollar index last Friday rallied to a new 1-1/2 year high, (5) fading support from the Jan 1 tax cuts, (6) peak earnings with the consensus for SPX earnings growth to decline to +8% in 2019 from 2018’s stellar pace of +24%, (7) continued US/Chinese trade and tech tensions, and (8) Washington political uncertainty as Democrats take control of the House in January and as the Mueller investigation seems to be getting closer to the White House.

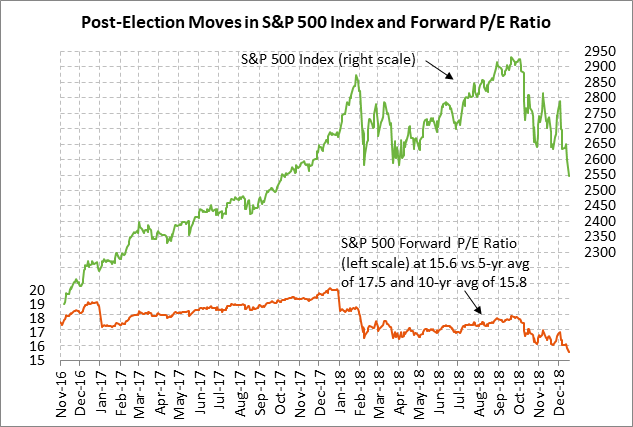

There are nevertheless some supportive factors for U.S. stocks that could yet bring the correction to a halt, which include (1) hopes that the Fed is nearly at the end of its rate-hike regime after this week’s hike, (2) much more reasonable valuation levels with the forward SPX P/E at 15.6 (below the 5-year and 10-year averages of 17.5 and 15.8, respectively, (3) indications that U.S. economic growth remains solid so far, (4) falling inflation expectations and a lack of pressure on the Fed for rate hikes based on inflation, (5) the sharp decline in oil prices, which frees up cash for consumers and businesses, and (6) somewhat reduced trade tensions from the NAFTA 2.0 agreement and the temporary U.S. tariff ceasefire agreements with China, EU, and Japan.

Markets wait to see if FOMC will pause — The market is currently discounting the odds at about 80% for a rate hike at the 2-day FOMC meeting that begins today. Since a rate hike today is mostly a foregone conclusion, the biggest question this week will be whether the FOMC softens its language by enough to indicate that the FOMC will pause its rate-hike regime in early 2018. The Fed seems ready to soften its current guidance for “further gradual increases” in rates, which would suggest that the Fed has taken itself off its 2-year track of raising rates every other meeting, and that decisions going forward will be fully data-dependent.

Market expectations for Fed rate hikes have fallen sharply in just the past two weeks. This month’s plunge in the U.S. stock market has convinced many investors that the outlook is not particularly bright and that the Fed should heed the stock market warning by backing off on its rate-hike regime. The key is whether the FOMC will heed the warnings of the stock market or whether it will plow ahead with its rate-hike regime based on the current strength in the economy, the tightness of the labor market, and the on-target inflation statistics.

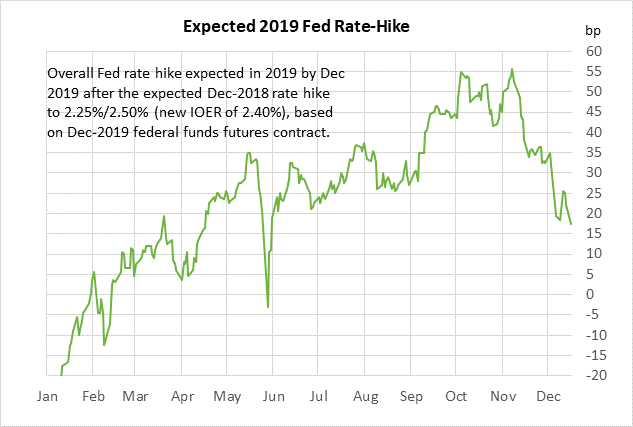

The market this month has sharply curbed its expectations for 2019 rate hikes. Assuming that the FOMC this week implements a +25 bp rate hike, the federal funds futures market is then discounting only a 70% chance of one +25 bp rate hike in 2019, which is much more dovish than expectations in November for two rate hikes in 2019.

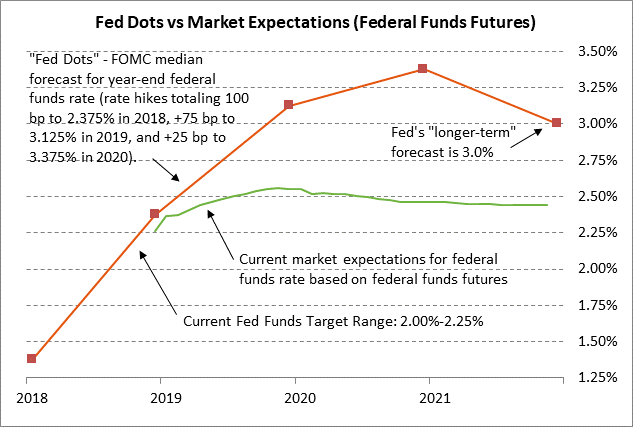

Aside from language adjustments, the markets will also key heavily on whether FOMC members revise their Fed-dot forecasts for the funds rate considerably lower. Right now, the FOMC is far more hawkish than the market is. The FOMC’s median forecast is for a rate hike this week, three rate hikes in 2019, and one rate hike in 2020, bringing the funds target range to 3.25%/3.50% by late 2020. The market, by contrast, is expecting the funds rate to be at only 2.50% through 2019/20, which is almost 100 bp lower than the FOMC’s median forecast.

U.S. housing starts outlook is undercut by a sharp drop in home builder confidence — The market consensus is for today’s Nov housing starts report to show a small -0.2% point decline to 1.226 million, giving back part of October’s +1.5% increase to 1.228 million. Housing starts in October were 7.9% below January’s 11-1/4 year high of 1.334 million units. Housing starts in recent months have been hurt mainly by lower sales caused by a sharp decline in home affordability, which in turn has been caused by rising home prices and higher mortgage rates.

Home builders in the past two months have become decidedly more pessimistic about the outlook for the home building market. The National Association of Home Builders’ housing index plunged by a combined -12 points in Nov-Dec to a 3-1/2 year low of 56 (18 points below last December’s 19-year high of 74).

Investors are also bearish on the outlook for the home building industry. The SPDR S&P Homebuilders ETF is down by -26.1% on a year-to-date basis, which is much worse than the -4.8% year-to-date decline in the S&P 500 index.