- ECB’s QE program is ending but a rate hike may be more than a year away

- Prime Minister May survives leadership challenge but now somehow needs to deliver a better Brexit deal

- 30-year T-bond auction to yield near 3.15%

- Italian bond yield falls to 2-1/2 month low on budget compromise offer

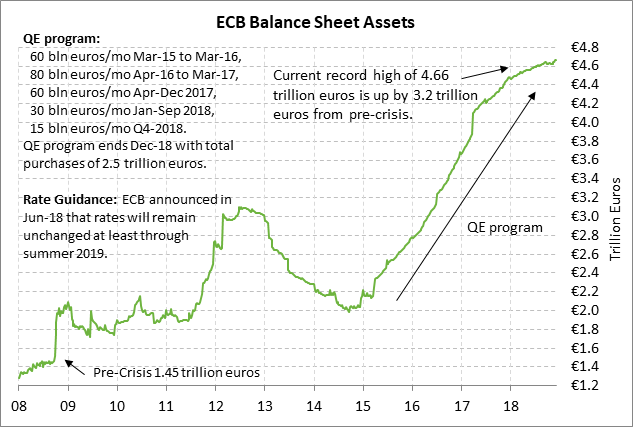

ECB’s QE program is ending but a rate hike may be more than a year away — The ECB at its meeting today is expected to confirm the end of its QE program in about two weeks on Dec 31. However, the ECB has already said that it will reinvest the proceeds from maturing securities, meaning that the balance sheet level will remain constant and will not decline in a backdoor type of tightening move. The ECB has already said that it will reinvest maturing debt “for an extended period of time,” which probably means at least 2-3 years. The Fed left its balance sheet unchanged for about three years (Nov 2014 to Oct 2017) before starting its balance sheet drawdown program in Oct 2017.

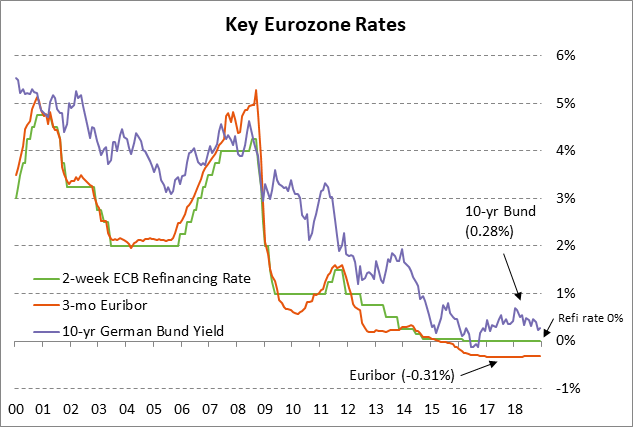

The ECB currently has a pledge in place to leave rates unchanged at least until summer 2019. However, the market now believes that the ECB will not be able to implement its first rate hike until early 2020, later than previous ideas of fall 2019.

ECB President Draghi today will be walking a fine line on admitting that the Eurozone economy has slowed while expressed confidence that the economy is strong enough for the ECB to end its QE program. In Q3, German GDP fell by -0.2% q/q due to a temporary dip in the auto sector caused by auto emissions issues, while the Italian economy in Q3 showed zero growth. The Eurozone as a whole in Q3 showed weak growth of only +0.2% q/q (+0.8% annualized).

The Eurozone is still facing significant obstacles including Brexit, the EU/Italy showdown, and big protests in France that have shaken the Macron government. The consensus is for Eurozone GDP to ease to +1.6% in 2019 and +1.5% in 2020 after this year’s growth of about +1.9%.

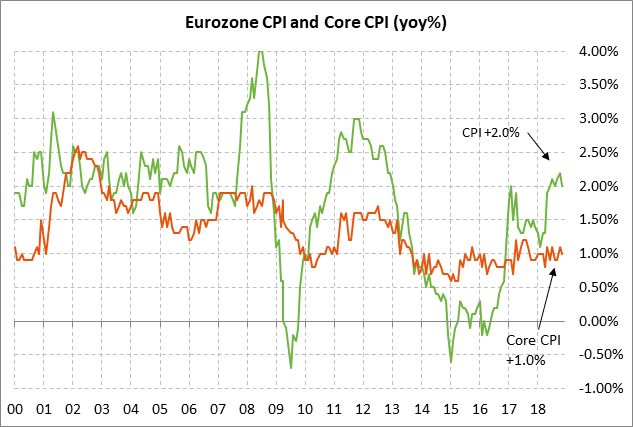

The ECB today will confirm the end of its QE program even though there is no sign of upward movement in inflation towards the ECB’s target of just under 2.0%. The headline Eurozone CPI was at +2.0% y/y in November. However, the more important Eurozone core CPI was at only +1.0% y/y in November, locked in the middle of its narrow 3-year range of 0.7%/1.2%.

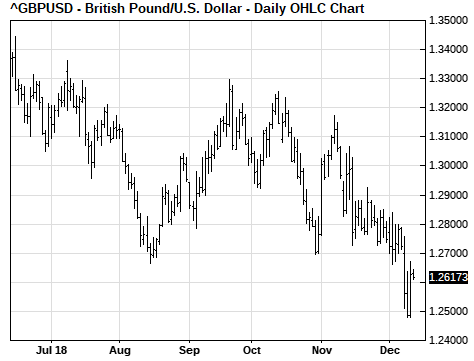

Prime Minister May survives leadership challenge but now somehow needs to deliver a better Brexit deal — Prime Minister May yesterday survived a Conservative Party leadership challenge and stayed in office to fight another day. Ms. May won the vote 200-117 but the fact that there were 117 members of her own party who opposed her made it even more obvious that it will be nearly impossible for her to get enough support in Parliament for her Brexit separation plan when she brings it to a vote by January 21.

The only good news about Wednesday’s leadership challenge was that another challenge vote cannot be held for a year. Conservative hard-line Brexiters shot their only bullet yesterday and it went for naught. The only thing that could bring down Ms. May now (other than a self-imposed resignation) is a no-confidence motion in Parliament that brings down her entire government and that would result in new elections.

Ms. May will meet with EU leaders at their summit today in an attempt to extract some concessions to sweeten her Brexit deal. However, the EU continues to insist that there will no relief from the current Irish backstop except for non-binding assurances that the EU does not want the UK to end up in the backstop forever.

Sterling on Wednesday slipped to a new 1-3/4 year low on news of the Conservative Party leadership vote but then recovered after Ms. May won the vote and closed the day up 1.12%. The FTSE 100 index on Wednesday rallied on Ms. May’s win and closed the day +1.08% higher, adding to Tuesday’s +1.27% rally.

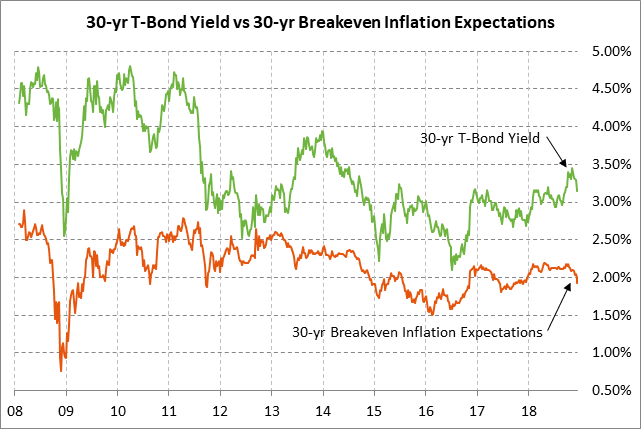

30-year T-bond auction to yield near 3.15% — The Treasury today will sell $16 billion of 30-year T-bonds, concluding this week’s coupon package. The size of today’s auction is up by $1 billion from the last reopening in Sep-Oct and is up by a hefty $4 billion from the $12 billion size that prevailed during 2016-2017.

The 30-year T-bond yield in the past 5 weeks plunged by an overall -36 bp to Monday’s 3-1/2 month low of 3.10% but then rebounded higher to 3.15% by Wednesday. The plunge in the 30-year T-bond yield has been due to (1) the drop in market expectations to only one Fed rate hike in 2019 from two rate hikes, (2) the sharp drop in inflation expectations due largely to the plunge in oil prices, (3) softer global economic growth, and (4) safe-haven demand.

The 12-auction averages for the 30-year are as follows: 2.37 bid cover ratio, $6 million in non-competitive bids, 4.2 bp tail to the median yield, 34.3 bp tail to the low yield, and 40% taken at the high yield. The 30-year is slightly above average in popularity among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 63.3% of the last twelve 30-year T-bond auctions, which is slightly above the median of 63.2% for all recent coupon auctions.

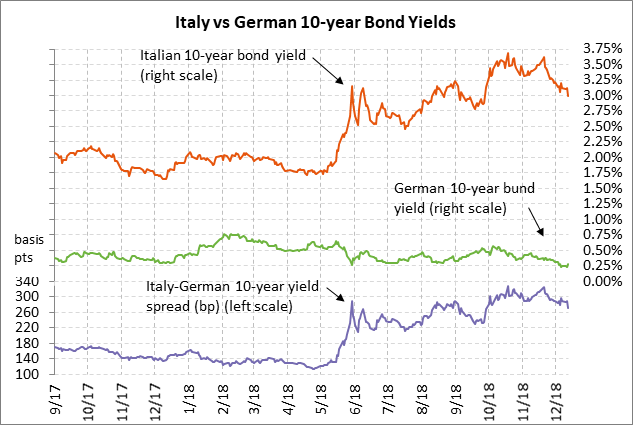

Italian bond yield falls to 2-1/2 month low — The 10-year Italian bond yield on Wednesday fell sharply by -12 bp to a 2-1/2 month low of 3.00% on reports of an Italian budget compromise. The Italy-German 10-year bond yield spread on Wednesday fell to a 2-1/2 month low of 272 bp, down sharply by a total of -55 bp from this autumn’s 5-3/4 year high of 327 bp. Italian Prime Minister Conte on Wednesday delivered an offer to European Commission President Juncker of a 2019 Italian budget deficit of 2.04% of GDP, down from the previous figure of 2.4%. However, Europe has been calling for an even lower figure, so the standoff so far continues.