- US/China ceasefire is marred by differing interpretations

- 2-week CR extension could reduce the odds for a U.S. government shut-down

- Wednesday becomes a partial holiday

US/China ceasefire is marred by differing interpretations — The markets on Monday reacted favorably to Saturday’s US/Chinese 3-month trade ceasefire. The S&P 500 index closed the day up +1.09%, although below its new 3-week high where it was up by +1.45%. The Nasdaq 100 index closed up +1.63%.

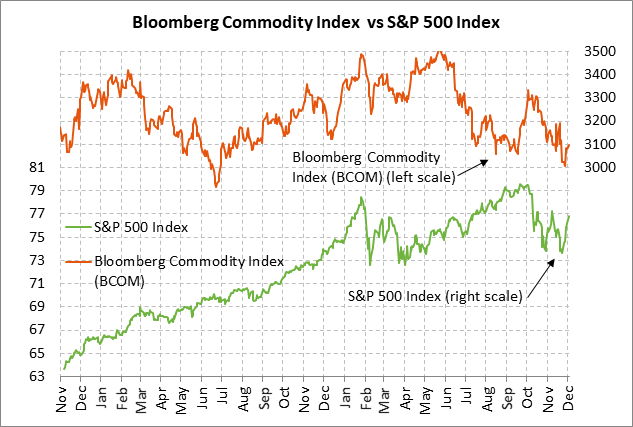

Commodity prices on Monday rallied on reduced trade tensions and China’s apparent agreement to buy a “substantial” amount of U.S. farm and industrial products. The Bloomberg Commodity index on Monday rallied by +0.48% and posted a new 1-1/2 week high. Jan soybeans gapped to a new 3-3/4 month high and closed the day up +1.23%. However, Feb lean hogs closed the day down -0.96%.

U.S. agriculture markets took the news of the cease-fire agreement with some caution since the size and timing of any Chinese commodity purchases was not detailed. In addition, China made no mention of any near-term move to cut its retaliatory tariffs on U.S. ag products, which would suggest there will be few purchases until a comprehensive deal is reached and penalty tariffs are dropped.

The Chinese government apparently intends to encourage purchases of U.S. soybeans for state-managed stockpiles by reimbursing the cost of the tariff, which would result in at least some purchases of U.S. soybeans. However, Chinese soybean crushers are not likely to buy expensive U.S. soybeans as long as the penalty tariff of 25% applies.

Some of the initial shine also came off the US/Chines ceasefire deal when the markets saw the wide variation in how the U.S. and China described the deal and when questions arose on Chinese auto tariffs. Mr. Trump late Sunday night tweeted that China agreed to drop all tariffs on U.S. autos to zero. China responded to Mr. Trump’s claim with a stony silence. Mr. Kudlow later Monday walked back Mr. Trump’s claim to say that China agreed with the general idea of reducing auto tariffs but there was no “specific agreement” on reducing auto tariffs.

Still, there was good news on Monday when White House economic advisor Kudlow clarified that the 90-day tariff ceasefire will actually start on Jan 1, which was better than the market’s initial assumption that the 90-day ceasefire would begin immediately on Dec 1. The deadline means if the negotiations are not successful, the Trump administration on April 1 will raise its penalty tariff to 25% from 10% on $200 billion of Chinese goods. Mr. Trump on April 1 might also slap tariffs on the remaining $267 billion of Chinese goods. China did not refer to the 90-day deadline in its summary of the agreement, which raised some questions about whether China agrees that there is a 90-day deadline.

There was also some good news on Monday with the announcement that U.S. Trade Representative Lighthizer will lead the negotiations for the American side. While it might seem more favorable for the markets to have trade-moderate Treasury Secretary Mnuchin leading the negotiations, Mr. Lighthizer is more likely to be able to lead negotiations towards a comprehensive deal that will stick and that will be accepted by President Trump. Back in July, Mr. Mnuchin’s trade deal with China quickly fell apart with President Trump because the deal was viewed as too soft on China. Mr. Lighthizer is a trade hawk but the fact remains that he is getting deals done since he landed NATFA 2.0 and helped reached a revised free trade deal with South Korea.

White House trade advisor Navarro and Treasury Secretary Mnuchin seemed to troll each other on Monday about who would lead the negotiations. Mr. Navarro told NPR that Mr. Lighthizer would be leading the negotiations. Mr. Mnuchin apparently took that as a slight since he then tweeted that President Trump was actually the one that would be leading the negotiations.

While Mr. Trump obviously has control over the broad contours of a deal, the fact remains that only Mr. Lighthizer has the detailed trade knowledge to be able to negotiate a comprehensive trade deal on a day-to-day basis with China. China might actually be a little relieved that Mr. Lighthizer has been placed in charge of negotiations, even though he is a China hawk, since there will at least be clear lines of authority and Chinese officials will not have to wonder if the moderate wing of the White House has the power to push through any final trade deal.

2-week CR extension could reduce the odds for a U.S. government shut-down — The markets during this busy week of news will at least not have to worry about a partial government shutdown on Friday night. Congress is moving towards passing a 2-week continuing resolution until Dec 21 to keep the government operating, thus avoiding conflicts with week’s events in Washington DC honoring former President George H.W. Bush.

The delay until Dec 21 might actually reduce the odds for a partial U.S. government shutdown since presumably no one in Washington wants to be blamed if Congress leaves Washington for the Christmas holiday with the U.S. government on partial shutdown. The biggest budget beef is over the amount of funding for President Trump’s wall with Senate Democrats at $1.6 billion and House Republicans and President Trump at $5 billion.

Wednesday becomes a partial holiday — The U.S. stock and cash fixed income markets will be closed on Wednesday, along with CME equity and interest rate futures markets, to honor former President Bush. Federal offices will also be closed except the Fed’s bank payments system will be operational since banks will remain open. Fed Chair Powell’s testimony to the Joint Economic Committee of Congress has been postponed with a new date to be announced later. CME and ICE commodity futures markets will be open during regular hours on Wednesday.