- Trump throws some cool water on hopes for his weekend meeting with Xi

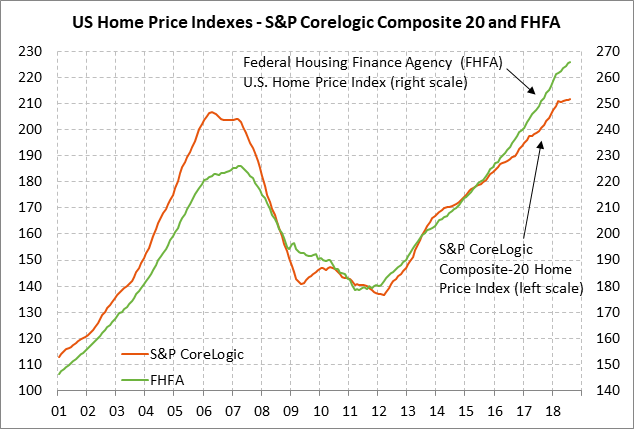

- U.S. home prices expected to continue higher

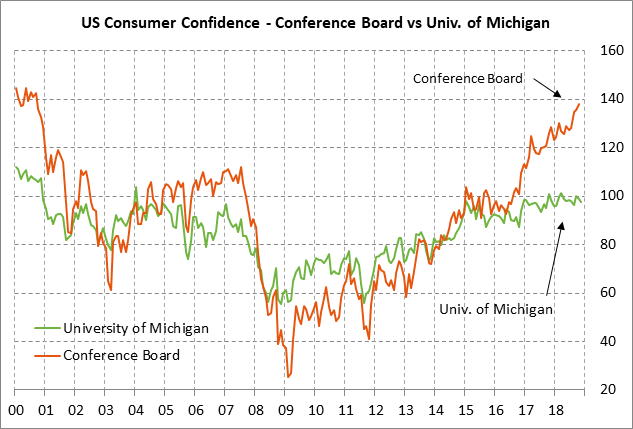

- U.S. consumer confidence expected to fall back from 18-year high

- 5-year T-note auction yield near 2-1/2 month low

Trump throws some cool water on hopes for his weekend meeting with Xi — President Trump in a WSJ interview released Monday afternoon said that it is “highly unlikely” that he would agree to China’s request that he hold off on raising the tariff to 25% from 10% on $200 billion of Chinese goods. He added, “If we don’t make a deal, then I’m going to put the $267 billion additional on” at a tariff rate of either 10% or 25%.

Mr. Trump’s comments may have simply been a negotiating tactic ahead of Saturday’s meeting to encourage China to come to the meeting with the maximum amount of concessions. However, Mr. Trump’s comments also made clear that the U.S. plans to pay hardball and that the market may be overestimating the potential for a breakthrough.

While a climb-down from the trade war would benefit both the U.S. and China, there is still a gulf between the two sides and a temporary truce is probably the best that can be hoped for at this point. Ideally, a truce would mean no more tariffs and that Mr. Trump would hold off on his Jan 1 plan to raise the tariff to 25% from 10% on $200 billion of Chinese goods.

By contrast, it would be disappointing for the markets if a “truce” were to involve only the U.S. holding off on tariffs on another $267 billion of Chinese goods and the U.S. still went ahead with raising the tariff to 25% from 10% on Jan 1 on $200 billion of Chinese goods. At that point, China would be obligated to retaliate with another round of higher tariffs or restrictions on U.S. exports to China. The only real truce would be if the U.S. and China stick with tariffs they have now and agree to formal trade negotiations over the next few months with an agreement not to impose any more tariffs. By contrast, the markets would be very pleased if the weekend agreement were to involve a truce plus a roll-back of some existing tariffs.

U.S. home prices expected to continue higher — The consensus is for today’s home price reports to show continued increases despite the current headwinds for the housing industry. The consensus is for today’s Sep FHFA index to show a solid gain of +0.4% m/m (after Aug’ s +0.3%) and for today’s Sep S&P CoreLogic composite-20 home price index to show a smaller gain of +0.2% m/m (after Aug’s +0.1%).

The FHFA index has remained strong in recent months and showed a +6.1% y/y increase in August. The Composite-20 index, by contrast, has shown only a small gain of +0.1% in each of the last three reporting months (June-Aug) and was up by a smaller +5.5% y/y in August.

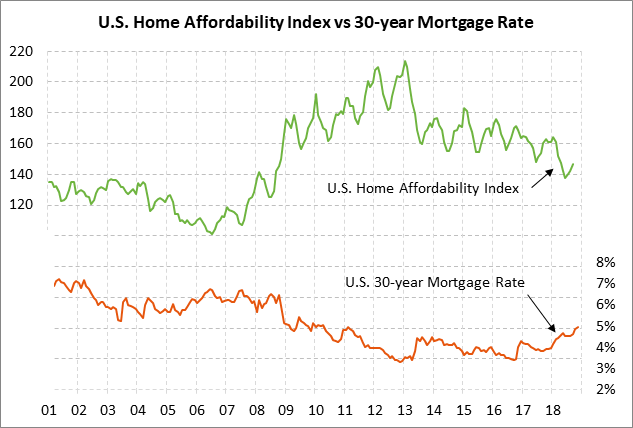

Housing prices should moderate in coming months due to the poor level of home sales and sharp drop in affordability. Existing home sales fell for six straight months (April-Sep) by a total of -8% and then finally showed at least a modest recovery by +1.4% in October. Meanwhile, the National Association of Realtors’ U.S. housing affordability index fell to a 10-year low of 137.7 in June and then recovered only modestly to 146.7 in September. Home affordability has dropped sharply this year due to rising mortgage rates and high home prices. The FHFA U.S. home price index has soared by +49% from the housing bust low posted in 2011.

U.S. consumer confidence expected to fall back from 18-year high — The market consensus is for today’s Nov Conference Board U.S. consumer confidence index to show a -2.1 point decline to 135.8, reversing most of October’s +2.6 point increase to an 18-year high of 137.9. Expectations for a decline in today’s report stem in part from last week’s news that the University of Michigan’s U.S. consumer sentiment index in November fell by -1.1 points to 97.5.

U.S. consumer sentiment in November was undercut by (1) political uncertainty with the Nov 6 mid-term elections, (2) the stock market correction, and (3) ongoing concern about tariffs and rising mortgage rates. However, consumer sentiment remains generally strong due to (1) the strong U.S. economy and labor market, (2) rising wages with Oct average hourly earnings rising to a 9-year high of +3.1% y/y and Sep personal income rising +4.4% y/y, (3) solid household balance sheets with the generally strong stock market and the continued rise in home prices, and (4) the sharp drop in gasoline prices.

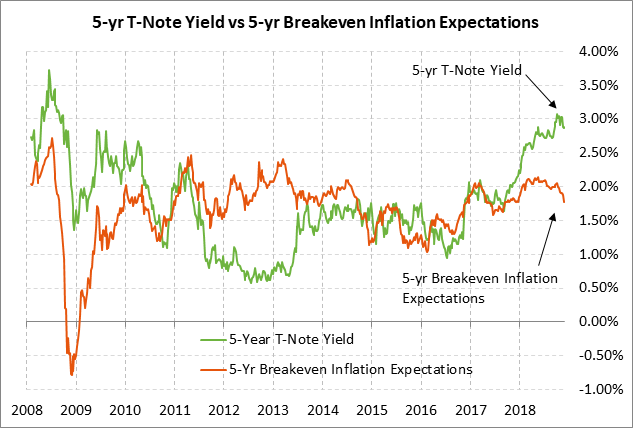

5-year T-note auction yield near 2-1/2 month low — The Treasury today will sell $40 bln of 5-year T-notes. The Treasury will then conclude this week’s $129 bln T-note package on Wednesday by selling $18 bln of 2-year floating-rate notes and $32 bln of 7-year T-notes. The $40 bln size of today’s 5-year T-note is up by $1 bln from October and by $5 bln from the $34 bln size seen during 2016/17.

The 5-year T-note yield late yesterday afternoon was trading at 2.89%, which is near last week’s 2-1/2 month low of 2.85% and well below the early-Nov 10-year high of 3.10%. The 5-year T-note yield has fallen sharply by -21 bp in the past 2 weeks mainly because of the market’s more dovish view of Fed policy and the drop in inflation expectations caused by the meltdown in crude oil prices. The market is now expecting 61.5 bp of rate hikes through the end of 2019 (including December’s expected rate hike), down by -19 bp from the early-Nov peak of 80.5 bp.

The 12-auction averages for the 5-year are as follows: 2.47 bid cover ratio, $48 million in non-competitive bids, 4.1 bp tail to the median yield, 20.0 bp tail to the low yield, and 48% taken at the high yield. The 5-year is the third least popular security among foreign investors and central banks behind the 2-year and 3-year notes. Indirect bidders, a proxy for foreign buyers, have taken an average of 61.6% of the last twelve 5-year T-note auctions, which is mildly below the median of 63.2% for all recent Treasury coupon auctions.