- Fed rate-hike expectations slide on market turmoil and slower global economy

- Ross says Trump-Xi will at most agree on a framework for talks

- Sterling plunges as PM May holds on for dear life

- U.S. industrial production

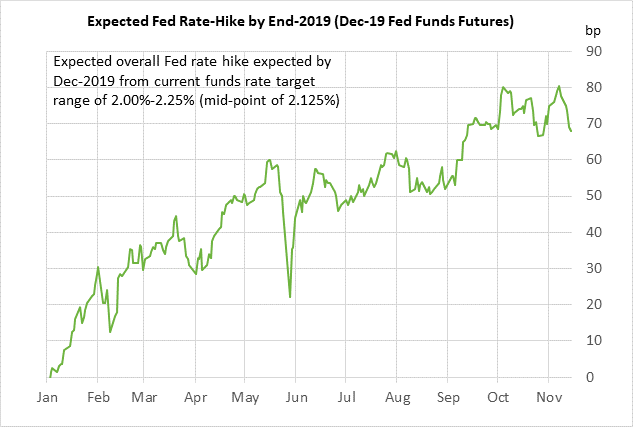

Fed rate-hike expectations slide on market turmoil and slower global economy — Market expectations for Fed rate hikes through the end of 2019 have fallen sharply by -12.5 bp in the past week, which is equivalent to half of a rate hike. Specifically, the Dec 2019 federal funds contract (on a yield basis) has fallen by -12.5 bp to 2.805% from last week’s record high of 2.93%.

The market is now discounting a total of 67 bp of rate hikes through the end of 2019 (i.e., 2.7 rate hikes), down from last week’s peak of 80.5 bp (i.e., 3.2 rate hikes). The current expectation for 2.7 rate hikes through the end of 2019 includes the expected rate hike at the next meeting on Dec 18-19, meaning the market is now discounting only 1.7 rate hikes during 2019 versus last week’s peak of 2.2 rate hikes.

The market in the past week has cut rate-hike expectations due to (1) weak global economic data with both Germany (-0.8% q/q annualized) and Japan (-1.2%) showing negative GDP growth in Q3, (2) a more tepid inflation outlook with last Friday’s core CPI showing an increase of only +1.6% (3-month annualized) and with the 10-year breakeven rate falling by -7 bp to a 10-month low of 2.01% due in part to the plunge in oil prices, (3) increased worries about the U.S. corporate bond market, which is seeing credit stress due to higher interest rates and the melt-down of former blue-chip stars like GE, (4) the increased chance that the UK will crash out of the EU in March 2019 after the opposition seen to PM May’s Brexit withdrawal agreement, (5) Italy’s obstinacy on its 2019 budget deficit, which keeps EU tensions high, and (6) worries about the slowing Chinese economy, particularly if Presidents Trump and Xi do not reach a truce at their G-20 meeting in Argentina in 2 weeks.

Meanwhile, Fed Chair Powell in comments over the past two days said that the U.S. economy is currently strong but he acknowledged that the U.S. economy faces headwinds from slower growth overseas, fading fiscal stimulus, and the lagged effects of the Fed’s rate hikes to-date.

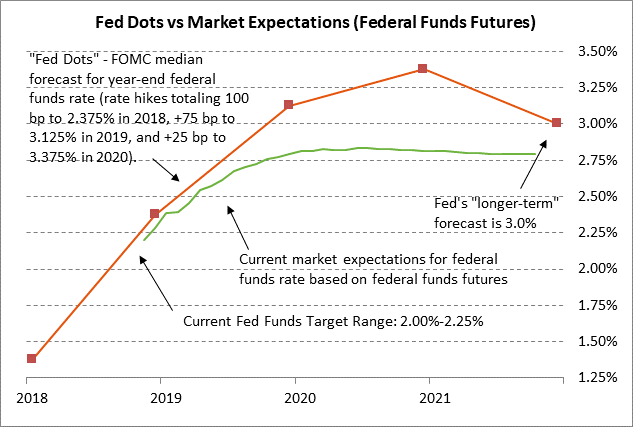

Mr. Powell also made the interesting comment that, “We have to be thinking about how much further to raise rates, and the pace at which we will raise rates.” In one sense, that statement is a non-event since the Fed always has to think about how it will change rates. However, the statement could also be read in a more dovish way that the Fed might already be thinking about toning down its hawkish Fed-dot forecast for a further +125 bp rate hike to 3.25-3.50% by the end of 2020.

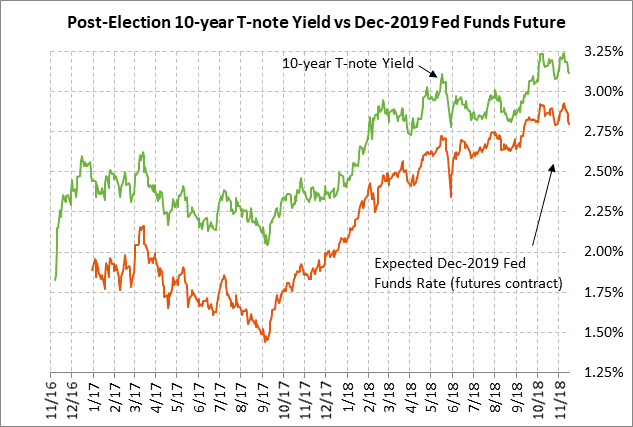

Since last Wednesday’s 1-month high of 3.25%, the 10-year T-note yield has fallen by -14 bp to Thursday’s close of 3.11%, which nearly matches the -12.5 bp drop in the Dec 2019 federal funds futures contract.

Ross says Trump-Xi will at most agree on a framework for talks — Commerce Secretary Wilbur Ross on Thursday said that the U.S. still plans to raise the tariff to 25% from 10% on $200 billion worth of Chinese products on Jan 1 and that the upcoming Trump-Xi meeting at the G-20 meeting will at best result in a “framework” for further talks. Meanwhile, the Financial Times on Thursday reported that USTR Lighthizer recently told some business executives that the next round of China tariffs is on hold, but Mr. Lighthizer’s office late Thursday denied that report.

The planning is continuing for the Trump-Xi meeting in two weeks at the G-20 meeting. Bloomberg on Thursday reported that China has outlined a series of concessions to bring to the meeting, but that the concessions are mostly a rehash of old measures and do not involve, for example, the U.S. demand for an end to the “Made in China 2025” initiative. In any case, the markets continue to hope that President Trump at his G-20 meeting with President Xi might at least agree to the same type of cease-fire deal that he currently has with Europe and Japan, i.e., an agreement not to implement new tariffs and to begin formal trade negotiations.

Sterling plunges as PM May holds on for dear life — Sterling on Thursday plunged by -1.7% but the FTSE-100 was able to close slightly higher by +0.06%. Prime Minister May’s Brexit withdrawal agreement met with disdain from nearly all quarters and the odds seem very slim that the plan will be approved by Parliament. If Ms. May’s government survives long enough, Parliament is expected to vote on the Brexit plan in early or mid December before leaving on Dec 20 for its holiday recess.

Prime Minister May on Thursday delivered a defiant speech in which she said that her plan was the only viable Brexit option and that the only alternative is to simply crash out of the EU in March 2019. Ms. May tried to project confidence even after two cabinet ministers resigned, the most notable being her Brexit minister Dominic Raab.

Meanwhile, Tory member Jacob Rees-Mogg is spearheading an attempt to bring a no-confidence vote against Ms. May and install a Brexit hardliner as the new PM. That effort may get the 48 parliament members necessary to begin the no confidence process, but there does not appear to be enough votes at this point to bring down Ms. May with a majority vote in Parliament. The EU is planning to hold a special summit on Nov 25 to ratify the Brexit deal unless “something extraordinary happens,” e.g., the fall of Ms. May’s government or the withdrawal of the plan by Ms. May.

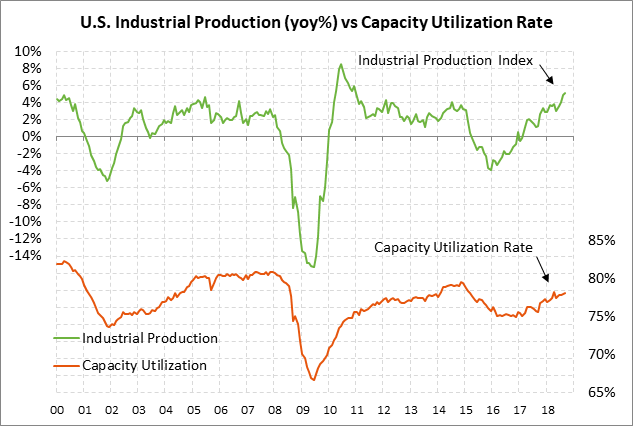

U.S. industrial production — Today’s Oct U.S. industrial production report is expected to show a tepid increase of only +0.2% after Sep’s +0.3%. U.S. Oct manufacturing production is expected at +0.2%, matching Sep’s +0.2%. On a year-on-year basis, industrial production is still showing a strong increase of +5.1% y/y and manufacturing production is at a 6-year high of +3.5% y/y.