- Trump administration holds off on auto tariffs due to lack of ripe targets

- May gets important Brexit victory with cabinet approval but approval by Parliament will be more difficult

- U.S. retail sales expected to improve after hurricane disruptions

- U.S. unemployment claims expected to show small changes and remain favorable

- EIA weekly Petroleum Report

Trump administration holds off on auto tariffs due to lack of ripe targets — President Trump at his meeting with advisors on Tuesday decided to hold off on tariffs and make some changes to the draft report that the Commerce Department is working on to justify auto tariffs based on national security concerns. That was good news because the global stock markets would undoubtedly take a significant hit on auto tariffs since that would severely disrupt global auto supply chains and hurt macroeconomic growth in the countries targeted by the tariffs, not to mention increase the price of autos for U.S. consumers.

The decision to hold off on auto tariffs was not surprising since the main targets would be Europe and Japan. Europe and Japan currently have some degree of immunity since President Trump has promised not to slap auto tariffs on Japan and Europe during formal trade negotiations, which are expected to kick into gear in early 2019. In addition, Canada and Mexico are already exempted from any new auto tariffs since the NAFTA 2.0 agreement includes protection from new tariffs in exchange for quota limits. The Trump administration might slap auto tariffs on South Korea, but that would violate the spirit, if the not the letter, of the US/South Korean free trade agreement.

The bottom line is that there are no major targets for auto tariffs at present. Just to be safe, however, European Commissioner for Trade Cecilia Malmstrom, meeting in Washington on Wednesday with USTR Lighthizer, said that if President Trump should suddenly announce tariffs on European autos, the EU will be ready with retaliatory tariffs on U.S. products. Ms. Malmstrom was in Washington to try to make sure that the US/EU trade talk process stays on track.

May gets important Brexit victory with cabinet approval but approval by Parliament will be more difficult — After a 5-hour meeting on Wednesday, Prime Minister May emerged with cabinet approval of her separation agreement with the EU. However, the approval was not unanimous and the markets are waiting to see if any of Ms. May’s cabinet members announce their resignations in protest or if a leadership challenge emerges from Brexit hardliners. The cabinet approval means that there can now be a special EU summit to approve the deal, perhaps on Nov 25.

However, the hard part now comes when Prime Minister May must get the majority approval of Parliament. If Parliament rejects the deal, then the risks will rise substantially that the UK crashes out of the EU in March 2019 without a transition period. A hard customs border would then suddenly pop up in March 2019, leading to massive shipping delays and product shortages. If Parliament rejects the agreement, there is the assurance of political chaos and perhaps a second referendum.

Sterling closed only +0.12% higher on Wednesday since the markets know the hard part of getting the Brexit deal through Parliament is just beginning. The FTSE-100 index on Wednesday closed mildly lower by -0.28%.

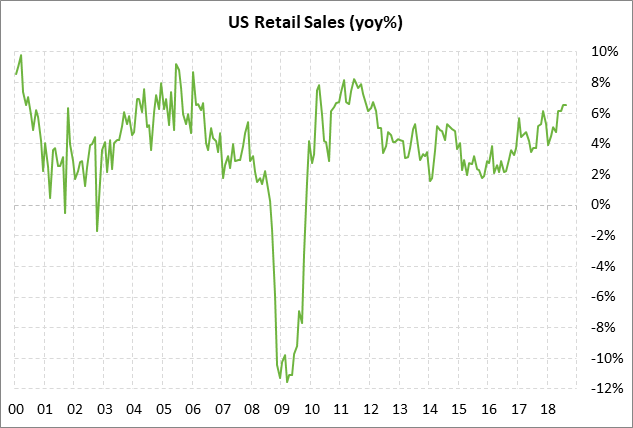

U.S. retail sales expected to improve after hurricane disruptions — The market consensus is for a strong Oct retail sales report of +0.5% and +0.5% ex autos, recovering from Sep’s weak report of +0.1% and -0.1% ex autos. Hurricane Florence in September caused some significant disruptions and Hurricane Michael caused some disruptions in October. Excluding hurricane disruptions, U.S. confidence and spending remains strong. Personal consumption contributed a hefty 2.57 percentage points of the Q2 GDP report of +4.2% and 2.69 points of the Q3 GDP report of +3.5%.

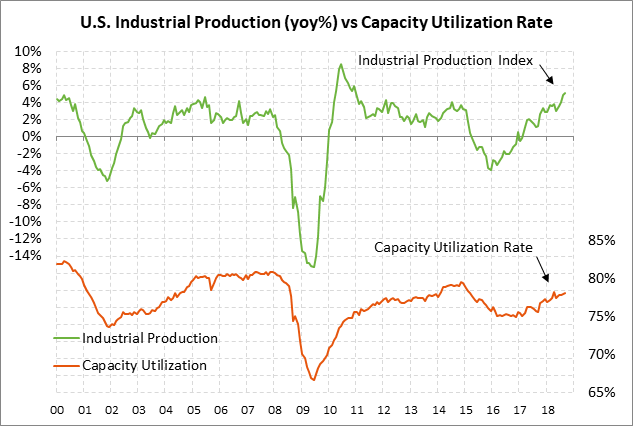

U.S. industrial production expected tepid — The market consensus is for a tepid Oct industrial production report of +0.2% m/m, down from Sep’s report of +0.3%. Excluding mining and utilities, Oct manufacturing production is expected to show an increase of +0.2% m/m, matching Sep’s increase.

On a year-on-year basis, industrial production is still showing a strong increase of +5.1% y/y and manufacturing production is at a 6-year high of +3.5% y/y. However, the manufacturing sector is cooling off somewhat as the stimulus from the Jan 1 tax cuts dissipates and as economic growth cools overseas. The ISM manufacturing index has fallen for the last two months by a total of -3.6 points to post a new 15-month low of 57.7 in October.

U.S. unemployment claims expected to show small changes and remain favorable — The unemployment claims data remains in very favorable shape with layoffs remaining near the lowest level in four decades. Initial claims are only +12,000 above Sep’s 49-year low of 202,000 and continuing claims in last week’s report fell to a new 45-year low of 1.623 million.

The consensus is for today’s initial unemployment claims report to show a small -1,000 decline to 213,000 (after last week’s -1,000 to 213,000) and for continuing claims to show a +2,000 increase to 1.625 million (after last week’s -8,000 to 1.623 million).

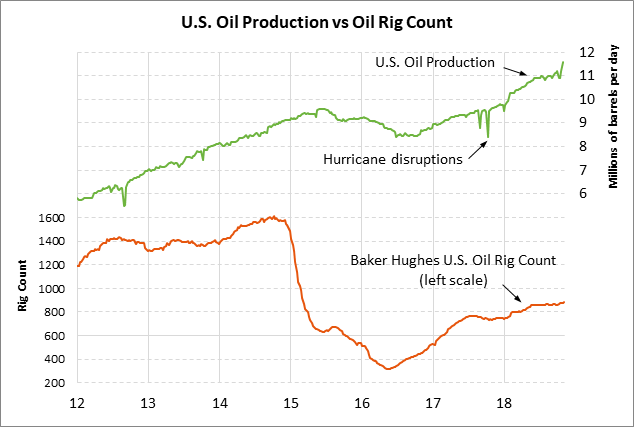

EIA weekly Petroleum Report — The consensus is for today’s weekly EIA report to show a +3.0 mln bbl rise in U.S. crude oil inventories, a +500,000 bbl rise in gasoline inventories, and a -2.2 mln bbl decline in distillate inventories. The API on Wed reported that U.S. crude oil inventories surged by +8.78 million bbls. U.S. crude oil inventories are currently 3.1% above the 5-year seasonal average, the highest such level since February. U.S. oil production in last week’s report showed a +3.6% w/w surge to a record high of 11.6 mln bpd.