- U.S. existing home sales expected to stabilize after 6-month slide

- U.S. final-Nov consumer sentiment expected unchanged

- U.S. LEI expected to eke out a small gain

- U.S. durable goods orders expected to be tepid

- U.S. unemployment claims expected to remain favorable

- 10-year TIPS auction to yield near 1.09%

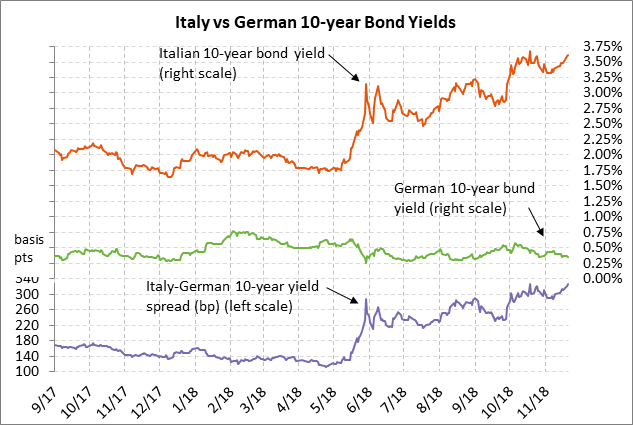

- Italian bond spread nearly matches October’s 5-3/4 year high

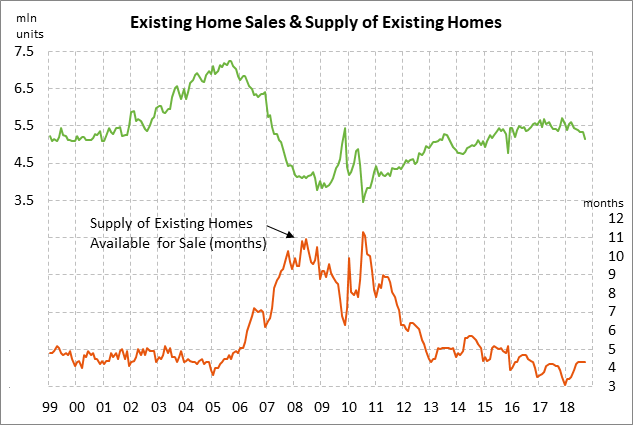

U.S. existing home sales expected to stabilize after 6-month slide — The market consensus is for today’s Oct existing home sales report to show a +1.0% increase to 5.20 million, halting the -8.0% slide seen over the past six months. U.S. home sales have fallen fairly sharply in recent months mainly because of worsening affordability, which has been caused by sharply higher home prices and rising mortgage rates. The National Association of Realtors’ U.S. Housing Affordability index fell to a 10-year low of 137.7 in June and was only modestly above that level in September at 146.7. The FHFA home price index has risen sharply by +49% from the housing bust low and the current 30-year mortgage rate of 4.94% is at an 8-year high.

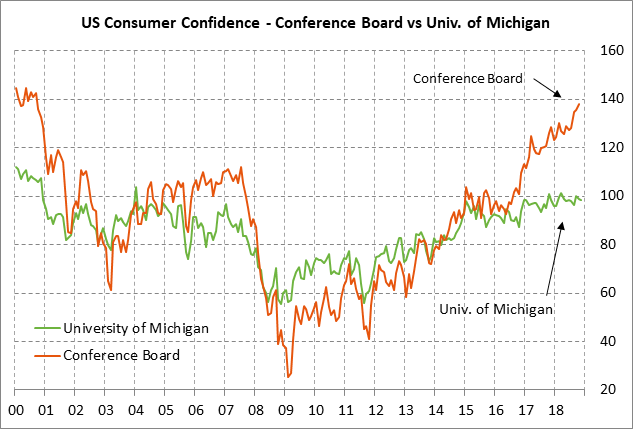

U.S. final-Nov consumer sentiment expected unchanged — The market consensus is for today’s final-Nov University of Michigan U.S. consumer sentiment index to be unchanged from the preliminary report of 98.3, which would leave the index down by -0.3 points from October.

U.S. consumer sentiment fell mildly by a total of -1.8 points in Sep/Oct to a 3-month low but is still in strong shape at only 3.1 points below February’s 15-year high of 101.4. U.S. consumer sentiment in November has been dampened by (1) political uncertainty with the Nov 6 mid-term elections, (2) the shaky stock market, and (3) ongoing concern about tariffs and rising mortgage rates.

However, consumer sentiment remains generally strong due to (1) the strong U.S. economy and labor market, (2) rising wages with Oct average hourly earnings rising to a 9-year high of +3.1% y/y and Sep personal income rising +4.4% y/y, (3) solid household balance sheets with the generally strong stock market and the continued rise in home prices, and (4) the sharp drop in gasoline prices.

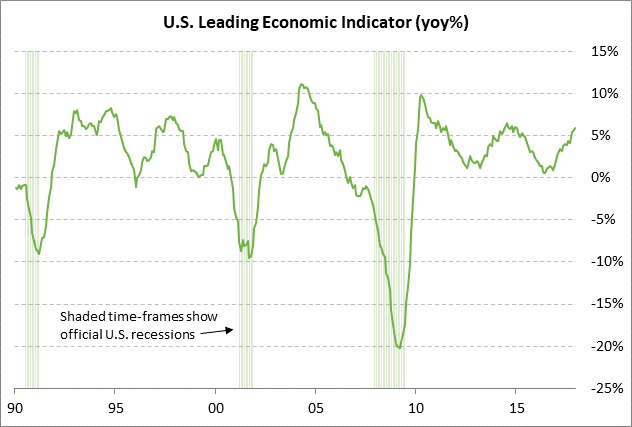

U.S. LEI expected to eke out a small gain — The consensus is for today’s Oct leading indicators index to show a small +0.1% increase, fading after Sep’s strong report of +0.5%. On a year-on-year basis, the LEI was very strong in September with a +7.0% y/y increase, the largest increase in more than eight years. The strong LEI is a positive indicator for the U.S. economy going into Q4. The consensus is for Q4 GDP to show a respectable increase of +2.6%, which would be down from the stellar growth rates of +4.2% in Q2 and +3.5% in Q3, but still above the Fed’s estimate of potential U.S. GDP of +1.8%. On a calendar year basis, the consensus is for strong +2.9% growth this year, followed by a slide to +2.6% in 2019 and +1.9% in 2020.

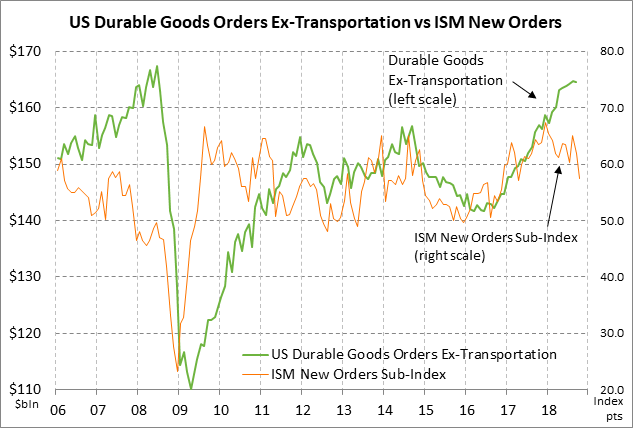

U.S. durable goods orders expected to be tepid — The consensus is for today’s Oct durable goods orders report to show a decline of -2.5% m/m after Sep’s report of +0.7%. Excluding an expected drop in aircraft orders, however, today’s durable goods orders report ex-transportation is expected to show a small increase of +0.4% ex-transportation after Sep’s report of unchanged. Capital spending is expected to be little changed with a small +0.2% increase in Oct core capital goods orders (ex defense and aircraft) after Sep’s report of -0.1%.

The markets will watch today’s report carefully since optimism has been fading about manufacturing orders and shipments. The ISM new orders manufacturing sub-index has fallen by a total of -7.7 points in the last two months (Sep-Oct) to post a new 1-1/2 year low of 57.4. Meanwhile, the headline ISM manufacturing index has fallen by -3.6 points in the last two months to post a new 6-month low of 57.7. Both those levels (ISM 57.7, new orders 57.4) are still relatively strong figures, but they nevertheless represent a distinct slowdown from the euphoria seen earlier this year.

U.S. unemployment claims expected to remain favorable — The consensus is for today’s weekly initial unemployment claims report to show a slight decline of -1,000 to 215,000 after last week’s +2,000 to 216,000. Meanwhile, continuing claims are expected to fall by -26,000 to 1.650 million after last week’s +46,000 to 1.676 million. The claims data remains in very favorable shape with initial claims only 14,000 above Sep’s 49-year low of 202,000 and continuing claims only 46,000 above the late-Oct 45-year low of 1.630 million.

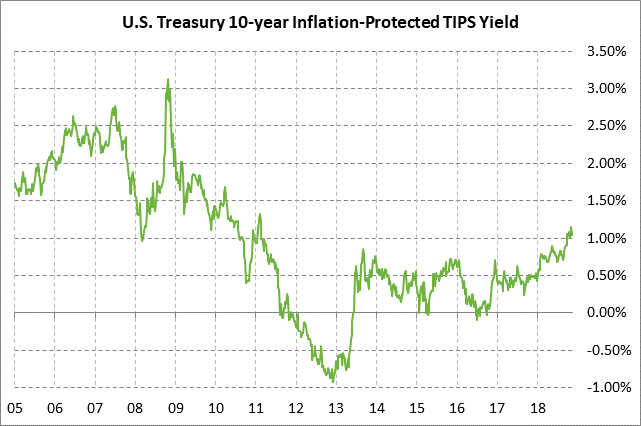

10-year TIPS auction to yield near 1.09% — The Treasury today will sell $11 billion of 10-year TIPS. The 10-year TIPS yield moved sharply higher by about 30 bp in Sep-Oct to post a 7-3/4 year high of 1.17% in early November. However, the yield in the past two weeks has slipped a bit to 1.09%. The 12-auction averages for the 10-year TIPS are as follows: 2.40 bid cover ratio, $22 million in non-competitive bids to mostly retail investors, 5.8 bp tail to the median yield, 12.0 bp tail to the low yield, and 52% taken at the high yield. The 10-year TIPS is the second most popular security among foreign investors and central banks behind the 30-year TIPS. Indirect bidders, a proxy for foreign buyers, have taken an average of 68.5% of the last twelve 10-year TIPS auctions, well above the median of 63.2% for all recent Treasury coupon auctions.

Italian bond spread nearly matches October’s 5-3/4 year high — The Italian 10-year government bond yield on Tuesday rose by +12 bp to a new 3-week high of 3.61%, which was only 7 bp below Oct’s 4-3/4 year high of 3.68%. The Italian-German 10-year yield spread on Monday rose by +4.2 bp to 326.6 bp, which was just 0.3 bp below Oct’s 5-3/4 year high of 326.9 bp.

The markets are worried about how hard the European Commission may come down on Italy today when it releases its budget assessments of the EU countries. The Commission could bring forward an assessment of Italy’s budget from next spring that would highlight Italy’s violation of EU budget rules and kick off the “excessive deficit” procedure that could eventually result in a fine on Italy of at least 0.2% of GDP.