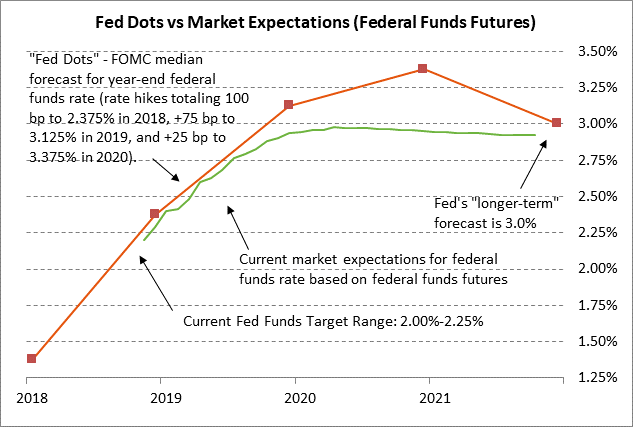

- FOMC meeting was a non-event and market still expects December rate hike

- U.S. consumer sentiment expected to dip but remain strong

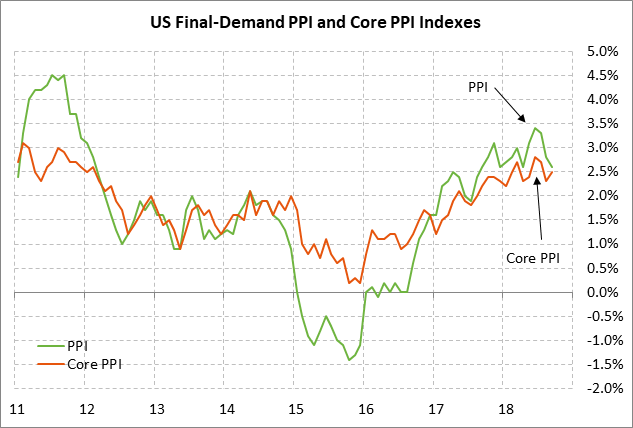

- U.S. Oct PPI expected to ease slightly

- Italian bond yield moves mildly higher as EU forecasts bigger Italian budget deficit

FOMC meeting was a non-event and market still expects December rate hike — The FOMC at its 2-day meeting that ended yesterday left its funds rate target unchanged at 2.00%/2.25%, which was in line with unanimous market expectations. The federal funds futures curve on Thursday turned slightly more hawkish by 1-2 bp for the 2019/20 contracts. There was no change in expectations for the FOMC at its next meeting on Dec 18-19 to raise its funds rate target by +25 bp to 2.25%/2.50%.

The FOMC made only minor changes in the language of its post-meeting statement, sticking with its view of a strong economy and the outlook for “further gradual” rate increases. The FOMC said that the risks to the outlook remain “roughly balanced.” The decision was unanimous at 9-0.

We expect the FOMC to raise its funds rate at the next meeting in December, and then to raise rates again at its second and fourth meetings in 2019 (March and June), thereby pushing the funds rate up to 2.75%/3.00% by mid-2019. That is a more hawkish view than the market, which is expecting the Fed to stretch those two rate hikes out over 2019, delaying that 2.75%/3.00% funds rate until closer to the end of 2019.

We suspect that the Fed will maintain its pattern of raising rates at every other meeting, at least until the funds rate is close to the neutral rate of 3.00%. The FOMC in mid-2019 with the funds rate at 2.75%/3.00% can then assess whether it should keep going with its rate hikes above 3.00% or pause to see how the economy reacts to 200 bp of rate hikes over three years.

By mid-2019, the U.S. economy is likely to have slowed from its current strong pace of +3.5% due to (1) the dissipation of tax-cut stimulus, (2) the cumulative effects of the Fed’s rate hikes, and (3) potentially negative effects from China if US/Chinese trade tensions continue into 2019.

The FOMC at present expects U.S. economic conditions to remain strong enough over the next two years to push the funds rate up to 3.25%/3.50% by late 2020, which would be above the Fed’s estimate neutral rate of 3.00%. However, it is far too early to tell whether the U.S. economy by late 2019 and 2020 will need a restrictive Fed policy to dampen economic growth and inflation.

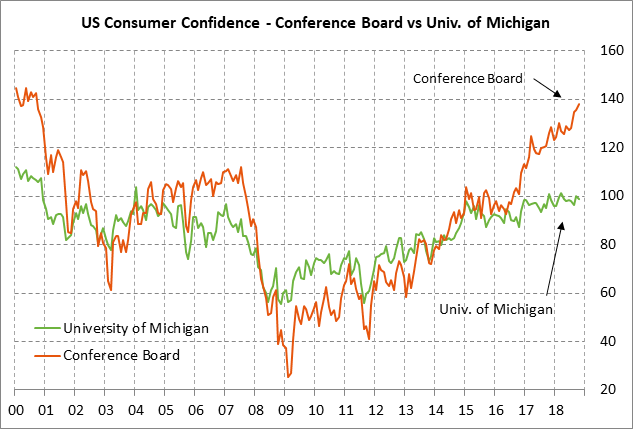

U.S. consumer sentiment expected to dip but remain strong — The market consensus is for today’s preliminary-Nov University of Michigan U.S. consumer sentiment index to show a -0.6 point decline to 98.0, adding to October’s -1.5 point decline to 98.6. Despite the expected back-to-back monthly decline, U.S. consumer sentiment remains in very good shape at only 2.8 points below March’s 15-year high of 101.4.

U.S. consumer sentiment was likely dampened in early November by political uncertainty ahead of the Nov 6 mid-term elections. Consumer sentiment is also seeing challenges from (1) rising interest rates, (2) the shaky stock market, and (3) concern about tariffs.

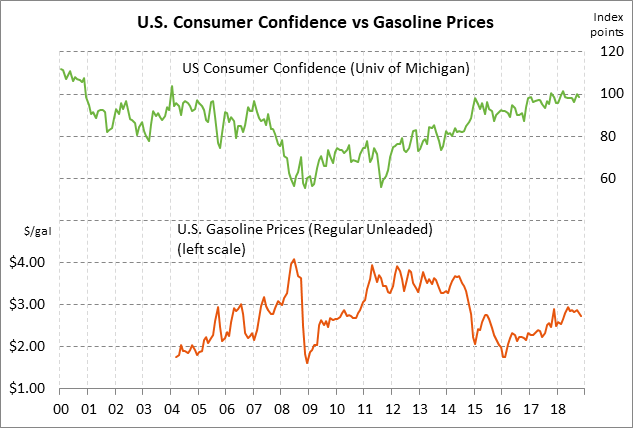

However, consumer sentiment in general remains very strong due to (1) the strong U.S. economy and labor market, (2) rising wages with Nov average hourly earnings rising to a 9-year high of +3.1% y/y and Oct personal income rising +4.7% y/y, (3) solid household balance sheets with the generally strong stock market and the continued rise in home prices, and (4) the -6% drop (-18 cents) in regular gasoline prices seen over the past month to the current 7-month low of $2.74 per gallon.

U.S. Oct PPI expected to ease slightly — The consensus is for today’s Oct final-demand PPI to ease to +2.5% y/y from Sep’s +2.6% and for the core PPI to ease to +2.3% from Sep’s +2.5%. The cooler PPI means that the Fed will not be under any pressure to speed up its rate-hike regimes in response to inflation.

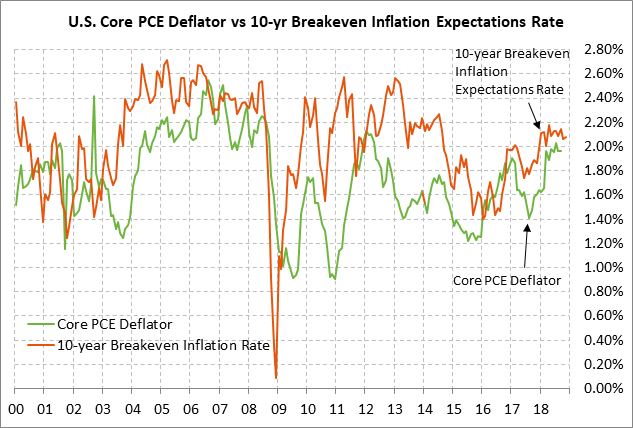

The core PCE deflator has been stable right at the Fed’s inflation target of +2.0% for the past five months. The current 10-year breakeven inflation expectations rate of 2.08% is just slightly above the Fed’s 2.0% inflation target but is well below May’s 3-3/4 year high of 2.21%.

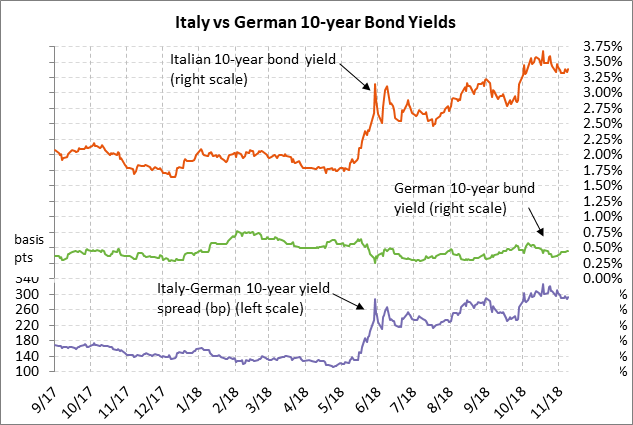

Italian bond yield moves mildly higher as EU forecasts bigger Italian budget deficit — The Italian 10-year bond yield on Thursday rose by +6 bp but remained relatively relaxed compared with recent highs. Specifically, the Italian 10-year government bond yield on Thursday rose by +6 bp to 3.39%, which was only 7 bp above last Friday’s 5-week low of 3.32% and well below the mid-Oct 4-3/4 year high of 3.69% by 30 bp. The Italian-German 10-year bond yield spread on Thursday rose by 5 bp to 294 bp, which was just mildly above Wednesday’s 1-month low of 289 and well below the mid-Oct 5-1/2 year high of 327 bp by 33 bp.

The European Commission on Thursday released its forecast that the Italian budget deficit in 2019 will actually be 2.9% of GDP, well above Italy’s estimate of 2.4%. The Commission also forecasted the 2020 budget deficit at 3.1% of GDP and said that Italy’s total government debt will not fall over the next two years. The European Commission’s higher deficit estimate stemmed in part from a lower Italian GDP estimate than the one used by the Italian government. Both, however, may be too optimistic.

Despite the higher deficit forecast by the European Commission, the Italian government continues to refuse to adopt a smaller deficit to meet EU rules, setting up an EU-Italy showdown with a possible fine for Italy down the road.