- FOMC will continue discussions on how far to raise the funds rate

- Unemployment claims expected to remain favorable

- OPEC+ plans to discuss 2019 production cut at weekend meeting due to recent oil price plunge

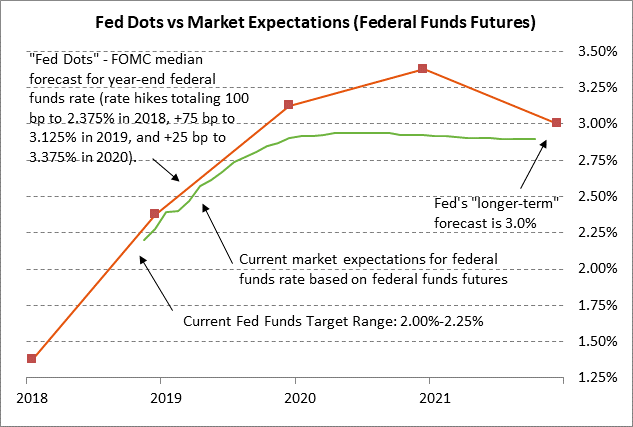

FOMC will continue discussions on how far to raise the funds rate — The unanimous consensus is that the FOMC at its 2-day meeting that concludes today will leave its monetary policy unchanged since the Fed just raised its funds rate target by +25 bp to 2.00%/2.25% at its last meeting in September. The Fed today will not release updated forecasts and Fed Chair Powell will not hold a press conference.

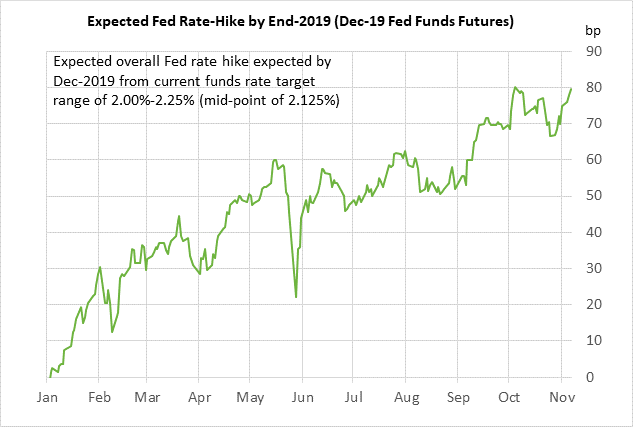

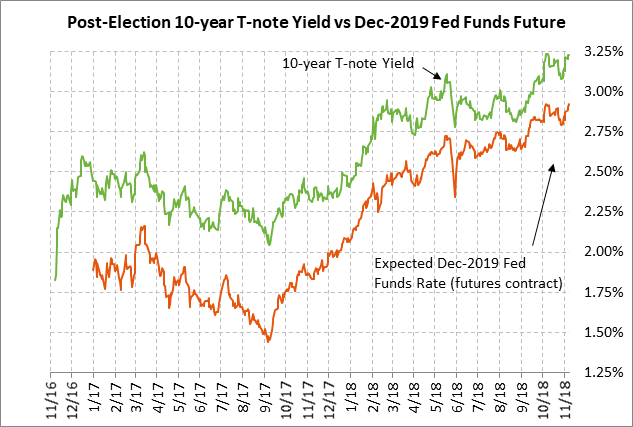

While the Fed this week is expected to leave its policy unchanged, the market is discounting a 100% chance of a 25 bp rate hike to 2.25%/2.50% at the next FOMC meeting on Dec 18-19, according to the federal funds futures market. That would be the fourth and final rate hike of 2018 and would make good on the Fed-dot median forecast for four rate hikes in 2018.

The FOMC at today’s meeting is likely to continue its discussion about how far above the neutral rate the Fed may have to raise the funds rate. The minutes from the FOMC’s last meeting on Sep 25-26 said that, “A few participants expected that policy would need to become modestly restrictive for a time and a number judged that it would be necessary to temporarily raise the federal funds rate above their assessments of its longer-run level.” The minutes were not surprising since the majority of the individual Fed-dot forecasts are above the 3.00% neutral rate from the end of 2019 through 2021. Indeed, nearly half of FOMC members (7 of 16) are predicting a funds rate above 3.50% by the end of 2020.

The hawkish tone to the September FOMC minutes supports our view that the FOMC will continue its pattern over at least the next three quarters of raising interest rates at every other FOMC meeting, which would mean rate hikes at the meetings in December, March and June, leaving the funds rate target at 2.75%/3.00% by mid-2019. That is a more hawkish view than the market, which is expecting the Fed to stretch two rate hikes out over 2019, delaying that 2.75%/3.00% funds rate until late 2019. We think the Fed will move more quickly than the market expects since the Fed expects to lift the funds rate above 3.00% and will not want to delay that move.

Of course, the Fed and the markets are only speculating about how the macroeconomic and geopolitical situation will look in 1-2 years, making predictions for the funds rate highly uncertain. The U.S. economy is strong now, but could easily lose momentum as the tax-cut stimulus fades and if trade tensions worsen. In addition, China is getting a serious stress test from U.S. pressure and any collapse in China would have very negative global consequences that would certainly force the Fed to pause its rate hikes.

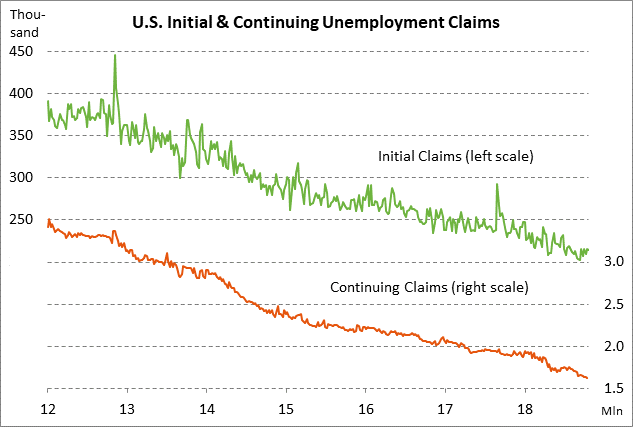

Unemployment claims expected to remain favorable — The consensus is for today’s weekly initial unemployment claims report to show a small -1,000 decline to 213,000 (after last week’s -2,000 to 214,000) and continuing claims to show a small +3,000 increase to 1.634 million (after last week’s -7,000 to 1.631 million). The unemployment claims data remains in very favorable shape with layoffs near the lowest levels in four decades. Initial claims are currently only +10,000 above September’s 49-year low and continuing claims in last week’s report fell to a new 45-year low.

U.S. businesses are not only holding on tightly to their current employees but they also continue to hire new employees at an active pace. Last Friday’s Oct payroll report showed a strong gain of +250,000. Payrolls in the past six months have shown a strong average monthly gain of +216,000. The unemployment rate in October remained unchanged from September’s 49-year low of 3.7%, which is well below the Fed’s estimate of the long-run natural unemployment rate of 4.5%.

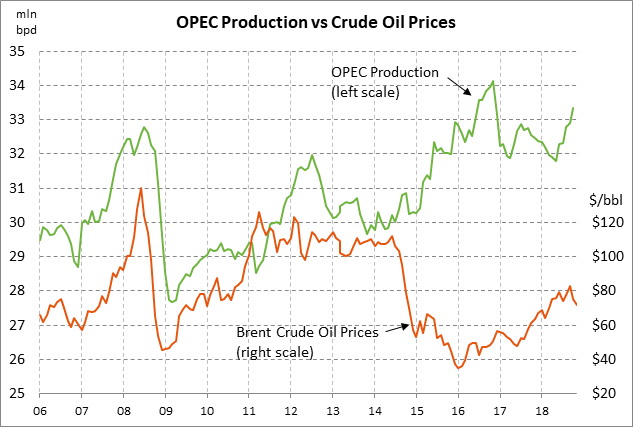

OPEC+ plans to discuss 2019 production cut at weekend meeting due to recent oil price plunge — The OPEC+ Joint Ministerial Monitoring Committee will meet this weekend and reports indicate that the group will discuss possible production cuts for 2019. The talks this weekend will be in preparation for December’s full OPEC+ meeting, where ministers will have to decide how to handle production quotas starting in 2019 after their 2017/2018 production cut agreement expires.

OPEC+ ministers are undoubtedly alarmed by the fact that Dec WTI crude oil prices have plunged over the past month by a total of -20.2%% from the early-Oct 4-year high of $76.72 to yesterday’s 7-month low of $61.20. Jan Brent crude has showed a similar overall sell-off of -17.5% from the early-Oct 4-year high of $83.56 to Tuesday’s 2-3/4 month low of $71.18.

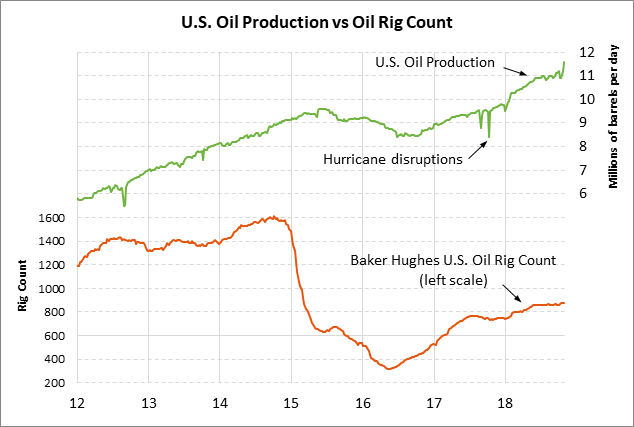

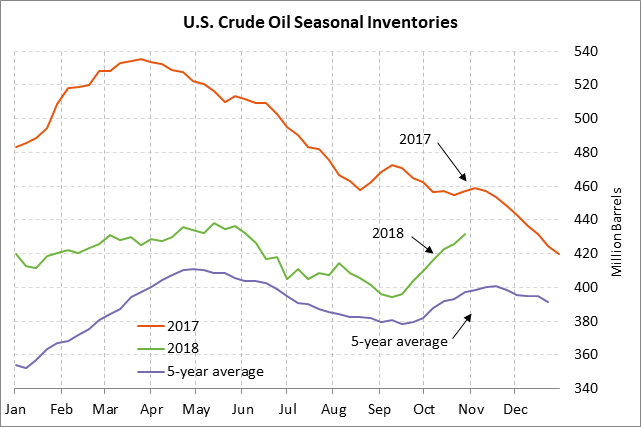

Dec WTI crude oil prices yesterday fell by -0.87% due to the very bearish weekly EIA report, which showed a +5.78 million bbl surge in U.S. crude inventories to a 5-month high, much more than expectations of +2.0 million bbl. U.S. crude oil inventories are now +3.1% above the 5-year seasonal average, the highest oil inventory position in nine months. In addition, Wednesday’s EIA report showed that U.S. crude production rose sharply by +3.6% w/w to a record high of 11.6 mln bpd. The EIA recently boosted its forecast for 2019 U.S. production to 12.06 mln bpd, which would represent a further 4% rise from the current level.

OPEC+ is now talking about the possible need for production cuts in 2019 due to strong U.S. production, a recovery in Libyan production to a 5-year high, and news of U.S. 6-month sanction waivers that suggest Iranian oil exports may not fall much farther from current levels through mid-2019. Just a month ago, Saudi Arabia was in the mode of “produce as much as you can” to offset supply worries. However, the improved supply situation now means that OPEC+ is facing the need to trim production in 2019.