PM

- FOMC discusses above-neutral funds rate

- LEI report expected to bode well for the U.S. economy through year-end

- U.S. claims data remains favorable despite hurricane distortions

- 30-year TIPS auction to yield near 1.21%

- China GDP expected to ease to new 9-year low

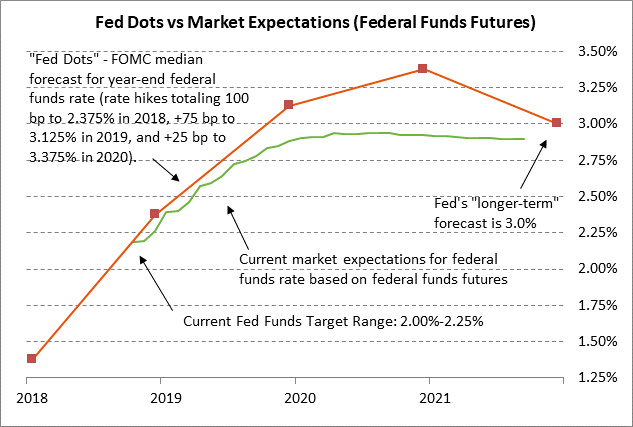

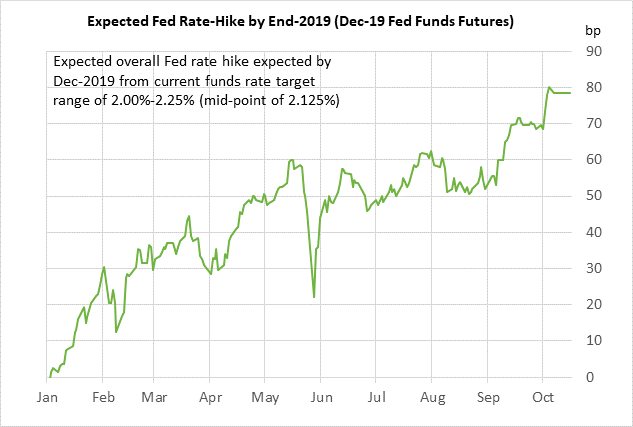

FOMC discusses above-neutral funds rate — The federal funds futures curve yesterday showed a slight 1-2 bp tightening in response to the Sep 25-26 FOMC minutes which noted the discussion among FOMC members of an above-neutral funds rate. The minutes said, “A few participants expected that policy would need to become modestly restrictive for a time and a number judged that it would be necessary to temporarily raise the federal funds rate above their assessments of its longer-run level.”

The minutes were not surprising since the majority of the individual Fed-dot forecasts are above the 3.00% neutral rate from the end of 2019 through 2021. Indeed, a near majority of FOMC members (7 of 16) are predicting a funds rate above 3.50% by the end of 2020.

The hawkish tone to the FOMC minutes supports our view that the FOMC will continue its pattern over at least the next three quarters of raising interest rates at every other FOMC meeting, which would mean rate hikes at the meetings in December, March and June, leaving the funds rate target at 2.75%/3.00% by mid-2019. That is a more hawkish view than the market, which is expecting the Fed to stretch two rate hikes out over 2019, delaying that 2.75%/3.00% funds rate until late 2019. We think the Fed will move more quickly than the market expects since the Fed expects to lift the funds rate above 3.00% and will not want to delay that move.

Of course, the Fed and the markets are only speculating about how the macroeconomic and geopolitical situation will look in 1-2 years, making predictions for the funds rate in 1-2 years highly uncertain. The U.S. economy is strong now, but could easily lose momentum as the tax-cut stimulus fades and if trade tensions worsen. In addition, China is getting a serious stress test from U.S. pressure and any collapse in China would have very negative global consequences that would certainly force the Fed to pause its rate hikes.

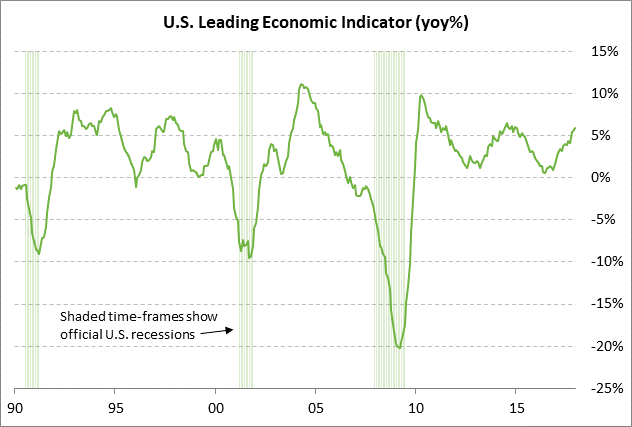

LEI report expected to bode well for the U.S. economy through year-end — The market consensus is for today’s Sep leading indicators report to show another solid increase of +0.5%, adding to Aug’s increase of +0.4%. The LEI is in very strong shape at a 4-year high of +6.4% on a year-on-year basis.

The LEI bodes well for U.S. economic growth through year-end, although the market is expecting a mild cooling from Q2’s torrid pace of +4.2%. The consensus is for U.S. GDP growth to ease to +3.2% in Q3 and +2.8% in Q4, leading to annual GDP growth in 2018 of about +3.1%. The market is then expecting the U.S. economy to slow to +2.5% in 2019 and to its long-term potential of +1.9% in 2020 as the Fed’s rate-hikes bite and as the tax-cut stimulus fades.

U.S. claims data remains favorable despite hurricane distortions — The unemployment claims data remains in favorable shape despite the disruptions from Hurricane Florence (which made landfall in North Carolina on Sep 14) and Hurricane Michael (which made landfall in Florida’s panhandle on Oct 10).

Initial claims are only +12,000 above mid-September’s 49-year low of 202,000 and continuing claims are only +15,000 above early-September’s 45-year low of 1.645 million. The consensus is for today’s initial unemployment claims report to show a small decline of -3,000 to 211,000 following last week’s +7,000 increase to 214,000. The consensus is for today’s continuing claims report to show a +5,000 increase to 1.665 million, adding to last week’s +4,000 gain to 1.660 million.

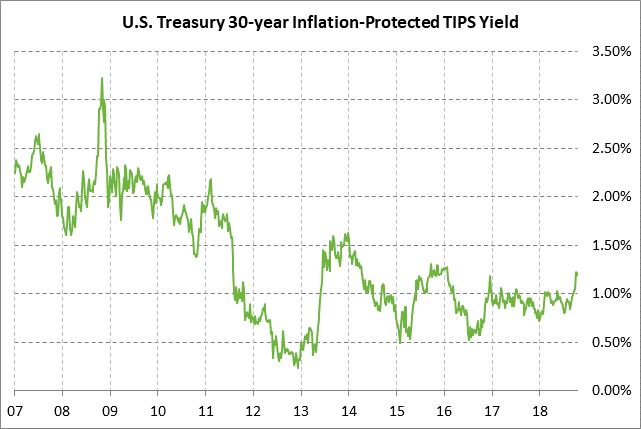

30-year TIPS auction to yield near 1.21% — The Treasury today will sell $5 billion of 30-year TIPS in the second and final reopening of the 1% 30-year TIPS of Feb 2048 that the Treasury first sold earlier this year in February. The Treasury in recent years has followed a pattern of a selling a new 30-year TIPS in February and then reopening it in June and October.

The 30-year TIPS yield moved sharply higher in early October to post a new 3-3/4 year high of 1.26% but has since eased a bit to 1.21%. The 30-year TIPS yield has been pushed higher by increased expectations for Fed rate hikes, the strong U.S. economy, and increased fears of inflation.

The 12-auction averages for the 30-year TIPS are as follows: 2.46 bid cover ratio, $14 million in non-competitive bids, 6.7 bp tail to the median yield, 16.6 bp tail to the low yield, and 65% taken at the high yield. The 30-year TIPS is the most popular coupon security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 72.3% of the last twelve 30-year TIPS auctions, well above the median of 63.1% for all recent Treasury coupon auctions.

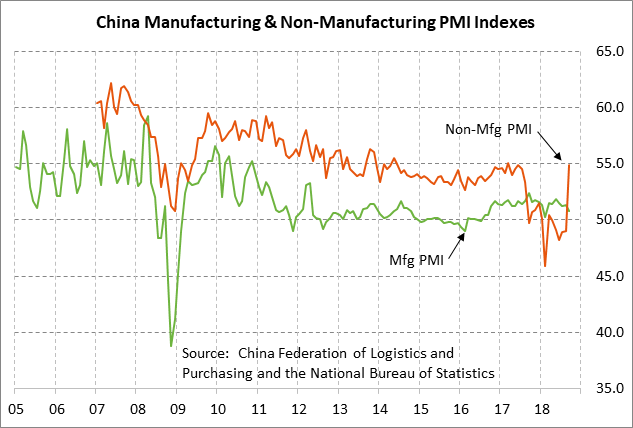

China GDP expected to ease to new 9-year low — The market consensus is for tonight’s China Q3 GDP report to ease slightly to +6.6% y/y from +6.7% in Q2. China’s GDP in Q2 already fell to match a 9-year low of +6.7% and is certainly headed lower in coming quarters. Indeed, with the soft Chinese economic data seen recently, a decline in Q3 GDP to only +6.6% seems less than believable. China’s national Sep manufacturing PMI fell by -0.5 points to a 7-month low and the Sep Caixin PMI fell by -0.6 points to a 16-month low of 50.0. On a more positive note, the Sep Caixin services PMI rose by +1.6 points to a 3-month high of 53.1. The consensus is for China’s annual GDP to fall from +6.6% in 2018 to +6.3% in 2019 and +6.1% in 2020 due to trade tensions, the government’s need to eventually relaunch its deleveraging campaign, and a softening to more normal growth levels for a large economy.