- Weekly market focus

- Trade tensions remain high as Canada has yet to agree to a revised NAFTA and as U.S. may announce new China tariffs late this week

- ISM manufacturing index expected to show a back-to-back dip but remain strong

Weekly market focus — The U.S. markets this week will focus on (1) trade tensions after the lack of a Canada/NAFTA agreement last Friday and as the Trump administration late this week may announcement the implementation of tariffs on another $200 billion of Chinese goods after the comment period ends on Thursday (Sep 6), (2) Washington political drama as the Russian investigation continues and as the Senate Judiciary Committee on Tuesday begins three days of hearings on the confirmation of Brett Kavanaugh to the Supreme Court, (3) whether Congress can pass spending bills over the next four weeks to avert a government shutdown on Sep 30, (4) oil prices as Tropical Storm Gordon could soon become a hurricane as it moves into the Gulf of Mexico, and (5) this week’s busy U.S. economic schedule that is capped by Friday’s U.S. July unemployment report (July payrolls expected +191,000 and July unemployment rate expected unchanged at 3.9%).

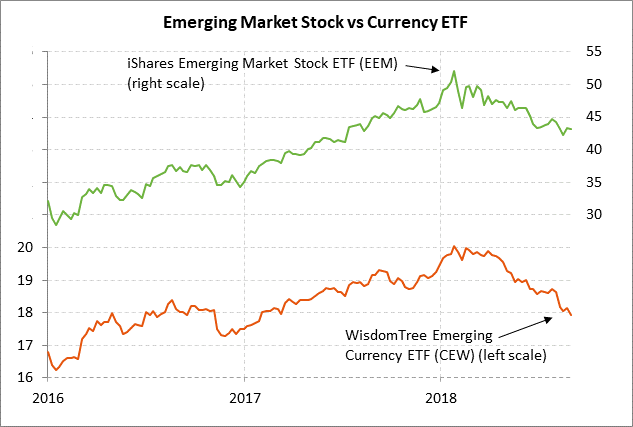

The markets will continue to watch the emerging markets with crises in both Argentina and Turkey. Turkey has yet to release the American pastor, meaning President Trump could launch more sanctions on Turkey at any time. Meanwhile, Turkey has not yet taken any major steps to address its currency crisis or any of its other major problems such as huge foreign debt obligations, a big current account deficit, and insufficient foreign currency reserves. However, the markets were mildly encouraged on Monday when Turkey’s central bank suggested that a rate hike may come at the bank’s policy meeting next Thursday (Sep 13).

The European markets this week will focus on trade tensions, Brexit, and Italy’s budget situation. The spread of Italy’s 10-year bond yield over Germany fell by -8 bp to 283 bp on Monday after (1) Fitch left its Italian credit rating unchanged at BBB, although it downgraded its outlook to negative, and (2) Italian deputy premier and League head Salvini said that Italy’s 2019 budget “will respect all rules.” The EuroStoxx 50 index on Monday extended its week-long decline to post a new 2-week low.

Trade tensions remain high as Canada has yet to agree to a revised NAFTA and as U.S. may announce new China tariffs late this week — Canada did not agree to revised NAFTA terms by last Friday’s U.S.-imposed deadline. However, the two sides said they were making progress and they agreed to resume talks this Wednesday. President Trump last Friday sent notification to Congress of the US/Mexico trade agreement that was reached last Monday and said the agreement would include Canada “if it is willing.” That meant that the U.S. and Canada still have 30 days to reach an agreement since the details of a new NAFTA agreement do not need to be sent to Congress for another 30 days. President Trump in tweets over the weekend again threatened to terminate NAFTA saying, “Congress should not interfere with these negotiations or I will simply terminate NAFTA entirely and we will be far better off.”

Regarding US/Chinese trade tensions, the markets are worried after last week’s reports that the Trump administration late this week plans to announce the implementation of tariffs on another $200 billion of Chinese goods. The Trump administration can implement the tariffs any time after the public comment period ends this Thursday (Sep 6).

The administration could announce the implementation of the tariffs effective immediately or it could announce a delayed implementation. With the first round of tariffs, the administration in June announced a 3-week delay in the implementation of tariffs on the first $34 billion of products and delayed the implementation of the tariffs on the final $16 billion of products until August. A delay would obviously give the U.S. and China some time for talks to potentially avert the implementation of the talks.

If the U.S. proceeds with new tariffs this week, then China has already said that it will slap tariffs on another $60 billion of U.S. goods. That action would mean that China would have tariffs on about 80% of all U.S. exports to Chinese including nearly all U.S. products except for crude oil and large aircraft.

Since the U.S. tariffs on another $200 billion of Chinese products have not yet brought China to the bargaining table with sufficient concessions, President Trump this week may also announce that he will slap tariffs on the remaining $250-275 billion of Chinese products imported by the U.S. The U.S. has imported $525 billion of Chinese goods over the last twelve months.

On the European front, European automaker stocks last Friday fell sharply after President Trump shot down Europe’s offer to cut tariffs to zero on all industrial goods including autos by saying that the offer was not good enough. There are concerns that President Trump may be on the verge of ending his tariff cease-fire with Europe after he said that “Europe is just as bad as China, only smaller.” The USTR is still considering President Trump’s proposal for 25% tariffs on imported autos based on national security grounds.

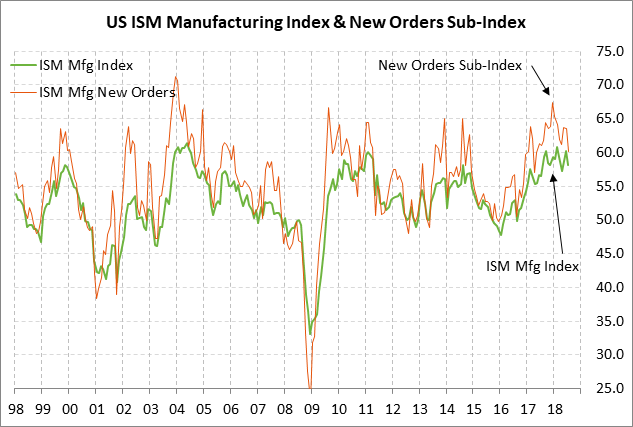

ISM manufacturing index expected to show a back-to-back dip but remain strong — The market consensus is for today’s Aug ISM manufacturing index to show a -0.7 point decline to 57.4, adding to July’s -2.1 decline to 58.1. The expected report of 57.4 would be only 3.4 points below Feb’s 14-year high of 60.8 and would still be a strong level. U.S. manufacturing confidence is taking at least a temporary hit from concerns about tariffs and the strength in the dollar. However, U.S. manufacturing confidence remains strong in general due to the very strong U.S. economy and the generally solid growth overseas. In addition, the order pipeline still looks very positive since the Aug ISM new orders sub-index was strong at 60.2 in July even after a -3.3 point decline.