- Weekly global market focus

- Next US/Chinese tariff round could arrive as soon as next week

- Light U.S. earnings week

- 2-year T-note auction

Weekly global market focus — The U.S. markets this week will focus on (1) any trade developments as a U.S. trade agreement with Mexico could be announced as soon as today but as US/Chinese trade relations remain tense after last week’s mid-level trade talks ended without any progress, (2) this week’s sale of $121 billion of T-notes, (3) a light earnings week with 13 of the S&P 500 companies scheduled to report, and (4) a moderate economic schedule with key reports including Tuesday’s Aug U.S. consumer confidence index (expected -0.9 to 126.5), Wednesday’s Q2 GDP revision (expected +4.0% from +4.1%), and Thursday’s July PCE deflator (expected slightly higher at +2.3% y/y headline and +2.0% y/y core versus June’s +2.2% and +1.9%, respectively).

Turkey may return to the headlines this week after the Turkish stock market was closed all last week for holidays. The Turkish lira last week traded sideways near the middle of the range established by the early-August plunge. The Trump administration this week could launch more sanctions against Turkey since President Erdogan still refuses to release American pastor Brunson. Meanwhile, the Turkish central bank has still refused to raise its official interest rates in a bid to support the lira and stave off capital flight and bank runs.

In Europe, the Italian situation remains tense with the 10-year Italian government bond yield spread over Germany last Friday reaching a 1-week high of 281 bp where it was only 5 bp below mid-Aug’s 3-month high of 286 bp and 8 bp below May’s 5-year high of 290. An Italy/EU flashpoint over migrants being held on a coast guard ship in an Italian harbor appeared to be resolved over the weekend but only after Italy threatened to veto the next EU budget.

The Eurozone Aug CPI on Friday is expected to be unchanged at +2.1% y/y headline and +1.1% y/y core. The tepid core report will encourage the ECB to maintain its current promise not to raise interest rates until at least summer 2019.

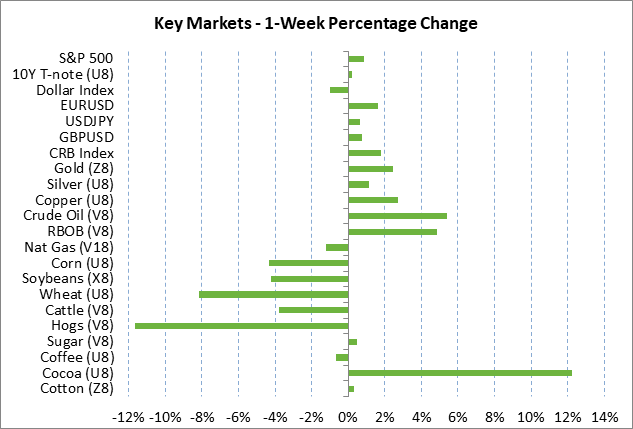

In Asia, the focus will remain on the Chinese markets as the U.S. and China are on a collision course over the next round of tariffs as soon as next week. However, the Chinese yuan last Friday rallied by 1% and posted a new 2-1/2 week high after Chinese authorities said that the daily yuan fix will again have a counter-cyclical factor. That was taken as a clear sign from Chinese authorities that the yuan has fallen far enough and that authorities now favor a mild rebound. The stronger yuan is supportive for confidence in the Chinese stock market, which benefited last week from reports of government-directed stock buying. The Shanghai Composite index last week rebounded higher from the recent 2-1/2 year low and closed the week +2.27% higher.

Regarding Asian economic data, the markets are looking ahead to Thursday night’s Aug NBS Chinese PMI data (Aug manufacturing PMI expected -0.2 to 51.0 after July’s -0.3 to 51.2) and Sunday night’s Aug Caixin manufacturing PMI (expected +0.1 to 50.9 after July’s -0.2 to 50.8). Thursday night’s Japan July industrial production report expected to show a small upward rebound of +0.2% after June’s sharp -1.8% decline.

Next US/Chinese tariff round could arrive as soon as next week — Time is growing short before the Trump administration can implement its proposed 10-25% tariffs on another $200 billion of Chinese goods. The public comment period for those tariffs ends on Sep 6, which means that the Trump administration could implement those tariffs as soon as next Friday (Sep 7). The U.S. today will hold its final day of public hearings on those tariffs. The Chinese government has already announced that it will retaliate for that move with tariffs ranging from 5% to 25% on another $60 billion worth of U.S. products.

There appears to be little chance of averting that next round of tariffs. The U.S. and China held mid-level trade meetings last week but those talks broke up with reports that no progress was made and that no further talks are scheduled. Chinese officials last week reportedly raised the possibility that further talks might have to wait until after the U.S. November mid-term elections. If the $200 billion round doesn’t bring concessions from China, then President Trump has threatened to levy tariffs on all U.S. imports from China, which totaled $525 billion in the last 12 months.

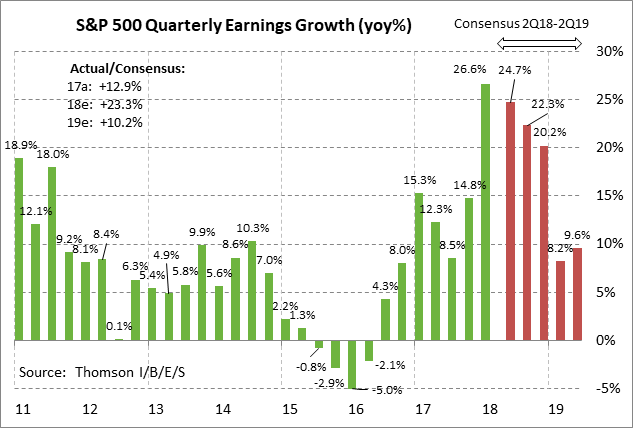

Light U.S. earnings week — There are 13 of the S&P 500 companies scheduled to report this week with notable reports including HP and Best Buy on Tuesday; salesforce.com on Wednesday; and Kroger and Dollar General on Thursday. Q2 earnings season was very positive with 79.8% of the 485 reporting SPX companies beating earnings expectations, well above the long-term average of 64% and the 4-quarter average of 75%, according to Thomson I/B/E/S. S&P 500 earnings growth in Q2 was very strong at +24.7%, just below Q1’s +26.6% pace. Looking ahead, earnings growth is expected to remain strong at +22.3% in Q3 and +20.2% in Q4, according to Thomson I/B/E/S. On a calendar year basis, the consensus is for very strong SPX earnings growth this year of +23.3%. Earnings growth is then expected to decelerate to +10.2% in 2019 as the effects from the Jan 1 tax cut start to wear off

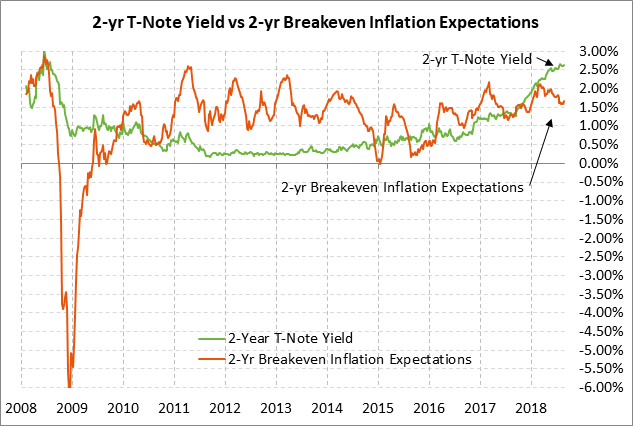

2-year T-note auction — The Treasury this week will sell $121 billion of T-notes on Monday through Wednesday. The 2-year T-note yield last Friday rose to a 2-week high and closed the day +0.4 bp at 2.62% where it was only 6 bp below July’s 10-year high of 2.68%. The 12-auction averages are as follows: 2.81 bid cover ratio, $266 million in non-competitive bids to mostly retail investors, 3.5 bp tail to the median yield, 21.8 bp tail to the low yield, 65% taken at the high yield, and only 44.8% taken by indirect bidders (far below the median of 63.1% for all recent coupon auctions).