- U.S. consumers expected to extend their spending surge

- U.S. industrial production expected to settle down after May-June disruptions

- U.S. NAHB housing index expected to edge to 11-month low as housing sector slows

- U.S. Q2 productivity expected to improve due to strong GDP growth

- U.S. official warns of new economic sanctions against Turkey

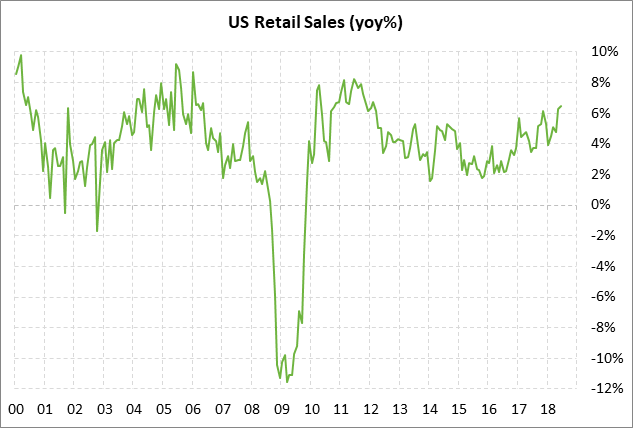

U.S. consumers expected to extend their spending surge — The market consensus is for today’s July retail sales report to show an increase of +0.1% and +0.3% ex-autos following June’s report of +0.5% and +0.4% ex-autos.

U.S. consumers since March have been on a spending spree that has been a major contributor to GDP growth. In June, retail sales were sharply higher by +6.5% y/y and +7.0% ex-autos. Personal spending contributed a hefty 2.69 percentage points of growth to the Q2 GDP report of +4.1%, which is much better than the average 1.83 point contribution last year.

U.S. retail sales have been supported by the combination of strong consumer confidence and the Jan 1 tax cuts, which put more cash in consumers’ pockets. The University of Michigan’s U.S. consumer sentiment index of 97.9 in July was only 3.5 points below March’s 14-1/2 year high of 101.4. Looking ahead, the Atlanta Fed’s GDPNow model is forecasting another strong quarter of personal consumption with a big contribution of 2.9 percentage points to its Q3 GDP forecast of +4.3.

U.S. consumer confidence is seeing support from (1) the strong U.S. economy, (2) the very tight labor market and the widespread availability of jobs, (3) rising income, and (4) rising household wealth with the strength in home prices and stocks. Negative factors for consumer confidence include (1) Washington political uncertainty, and (2) high gasoline prices.

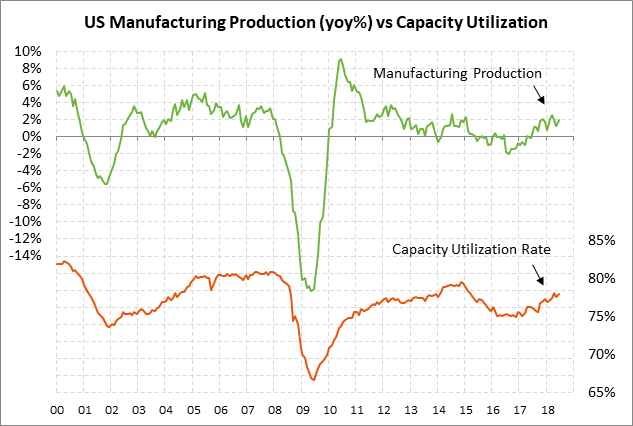

U.S. industrial production expected to settle down after May-June disruptions — The market consensus is for today’s July industrial production report to show an increase of +0.3%, falling back from June’s strong report of +0.6%. Focusing on just the manufacturing sector, today’s July manufacturing production report is expected to show an increase of +0.3% after June’s very strong report of +0.8%.

Industrial production had a strong +0.6% showing in June partially because of a rebound in auto production as a major auto parts supplier came back online after a fire at that supplier put a big dent in auto production in May. In any case, the underlying trend is positive for manufacturing production. Overall industrial production is also getting a strong boost from the petroleum sector with the mining and mineral extraction category showing a strong +1.2% increase in June. The ISM manufacturing index fell by -2.1 points in June due in part to concerns about tariffs, but remained at the solid confidence level of 58.1.

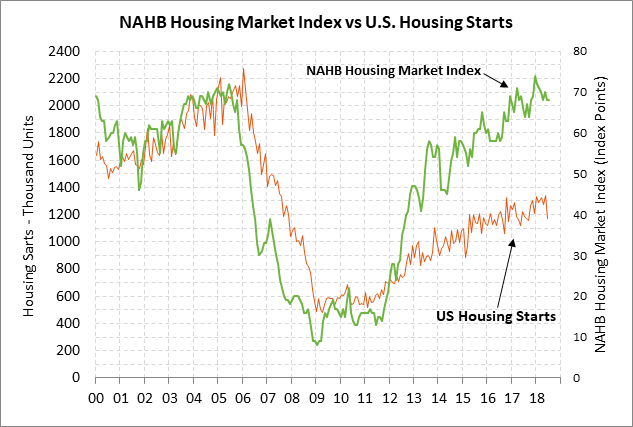

U.S. NAHB housing index expected to edge to 11-month low as housing sector slows — The market consensus is for today’s Aug NAHB housing market index to show a -1 point decline to 67. That would be a new 11-month low but would be only 7 points below the 19-year high of 74 posted in Dec 2017.

U.S. home builder confidence is showing some weakness due to concern about weaker demand. New home sales in June fell by -5.3% to an 8-month low of 631,000 units and new home prices in June skidded by another -2.5% to a 16-month low of $302,100 (now down by -12% from the late-2017 record high of $343,400). Home building activity is also seeing some weakness because of constraints of land, labor and materials. The combination of supply constraints and weaker demand caused housing starts in June to show a sharp decline of -12.3% to a 9-month low of 1.173 million units.

The slowdown in new home sales and home building activity has caused weakness in U.S. home builder stocks. The SPDR S&P Homebuilders ETF (XHB) is down -12% year-to-date and posted an 11-month low on Monday before rebounding modestly higher on Tuesday.

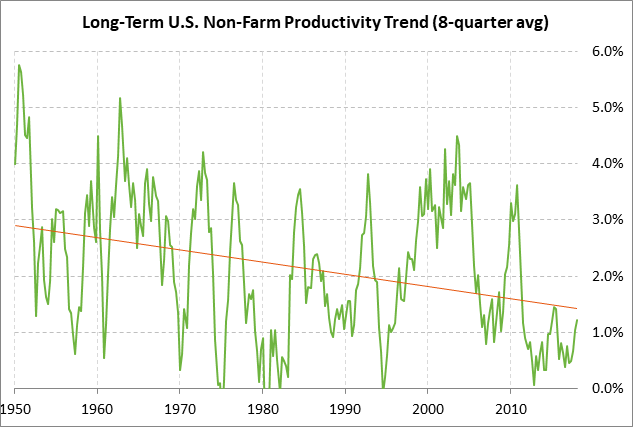

U.S. Q2 productivity expected to improve due to strong GDP growth — The market consensus is for today’s Q2 non-farm productivity report to show a strong increase of +2.4% following Q1’s weak report of +0.4%. The expected strength in Q2 productivity is a welcome development, although it stems mostly from a very strong Q2 GDP report of +4.1% (i.e., high output in the numerator of the productivity ratio) rather than from any structural improvement in productivity. The 8-quarter productivity average is only +1.2%, which is far below the post-war average of +2.2%. The weakness in productivity is a negative factor for real wages and corporate profits.

U.S. official warns of new economic sanctions against Turkey — The Turkish situation calmed down a bit on Tuesday but the markets must be prepared for new U.S. economic sanctions against Turkey if American pastor Andrew Brunson is not released very soon. A White House official told Reuters on Tuesday that “nothing has progressed” thus far on the Brunson case and that “if we do not see actions in the next few days or a week there could be further actions taken.” The U.S. has so far levied sanctions against two key Erdogan cabinet members and has doubled U.S. tariffs on Turkish steel and aluminum.

The Turkish lira and stock market showed a recovery rally on Tuesday due to some short-covering and hopes for a central bank interest rate hike to stop the currency bleeding. However, the Turkish situation remains grim in general with Turkey’s poor fundamentals and the feud with the U.S.

The Turkish lira on Tuesday rallied by +7.4% from Monday’s record-low close, more than reversing Monday’s -7.0% decline. However, the lira has a long way to go to reverse this year’s overall -83% decline. Meanwhile, the iShares Turkish stock ETF on Tuesday rebounded higher by +11.5%, more than reversing Monday’s -11.0% decline but not making much of a dent in last week’s -21% decline.