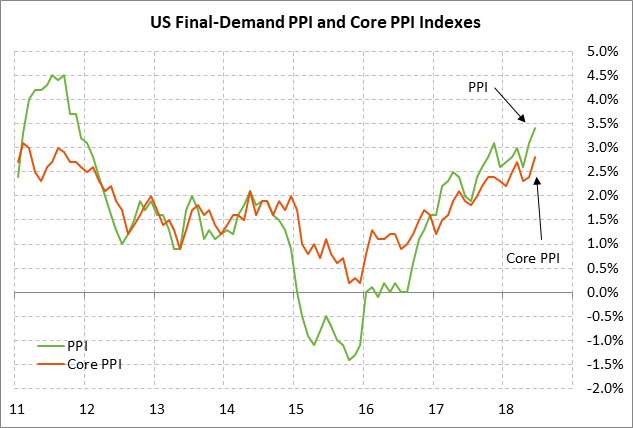

- PPI expected to remain at 6-3/4 year high

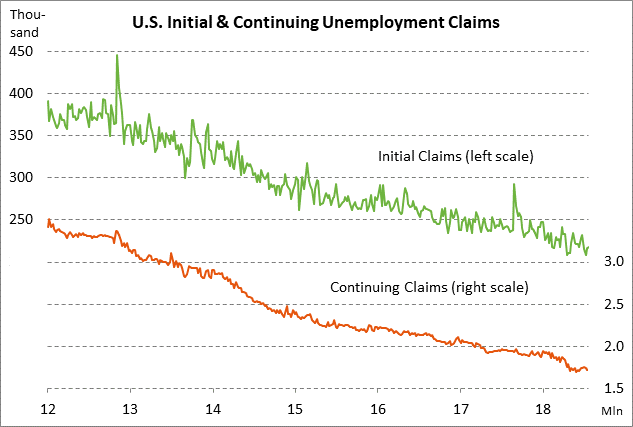

- Unemployment claims expected to remain very favorable

- 30-year T-bond auction expected to yield near 3.12%

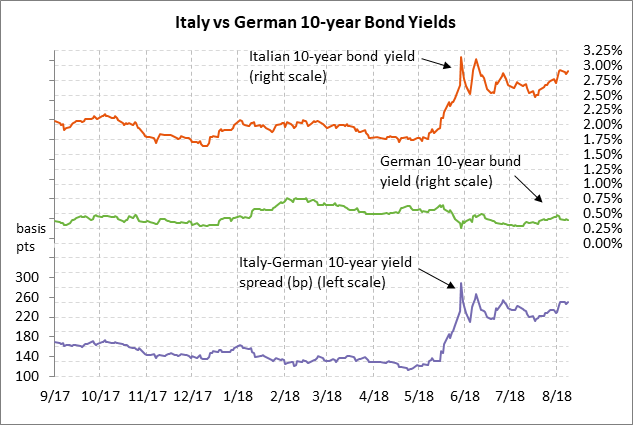

- Italian bond spread is near a 6-week high on budget worries

PPI expected to remain at 6-3/4 year high — The market consensus is for today’s July final-demand PPI to be unchanged from June with the headline PPI remaining at +3.4% y/y and the core PPI remaining at +2.8% y/y. The headline and core PPIs both rose to 6-3/4 year highs in June.

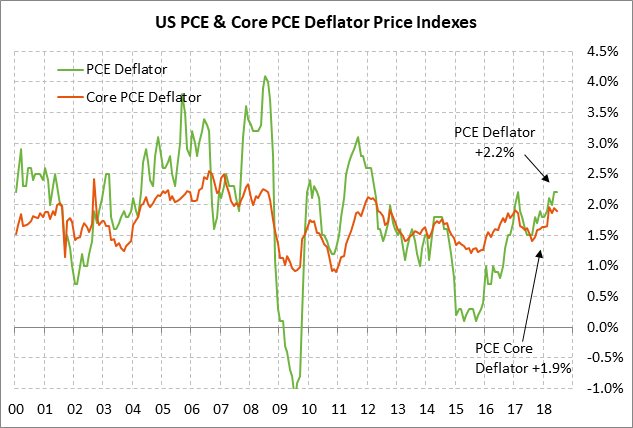

The strength in the PPI illustrates how all the inflation measure have been rising in recent months. The CPI in June rose to a 6-1/2 year high of +2.9% y/y and the core CPI rose to a 10-year high of +2.3% y/y. The PCE deflator, which is the Fed’s preferred inflation measure, has been a bit better behaved but has also been rising. The PCE deflator in May and June rose to a 6-1/4 year high of +2.2% y/y and June’s core deflator of +1.9% was just 0.1 point below March’s 6-1/4 year high of +2.0% y/y.

Despite the strength in the PPI and CPI measures, the Fed is not panicking about inflation since the PCE deflator is close to the Fed’s +2.0% target. In addition, the Fed has stressed that it is willing to allow inflation to temporarily move above its target since that target is symmetrical and since inflation has been generally been below target for the past decade.

Nevertheless, if the inflation statistics continue to move higher, then the Fed will be under pressure to speed up its rate-hike regime and raise rates higher than currently anticipated. The Fed has $3.4 trillion worth of excess high-powered money in the financial system, which could begin to fuel an inflation surge if the Fed isn’t cautious. The Fed is slowing drawing down its balance sheet, but it will be at least five years before the Fed gets its balance sheet down to a neutral level, meaning there are inflation risks lurking below the surface.

Unemployment claims expected to remain very favorable — The unemployment claims series are in very favorable shape with layoffs at the lowest level in more than four decades. The initial claims series is only +10,000 above the 48-year low of 208,000 posted in the July 13 week and the continuing claims series is only +23,000 above June’s 44-year low of 1.701 million. The consensus is for today’s initial claims report to show a +2,000 increase to 220,000, adding to last week’s slight +1,000 increase to 218,000. Meanwhile, the consensus is for today’s continuing claims report to show a +6,000 increase to 1.730 million, retracing part of last week’s -23,000 decline to 1.724 million.

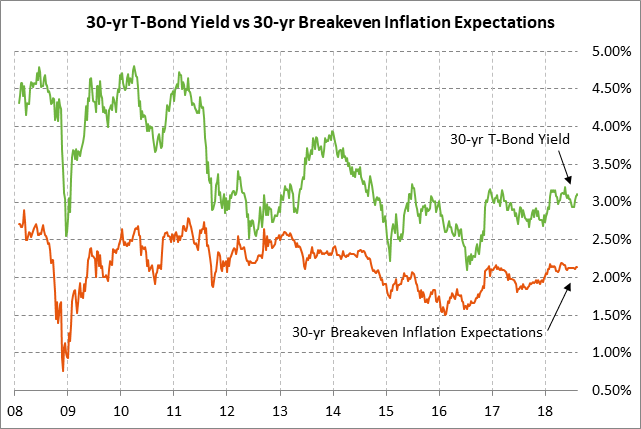

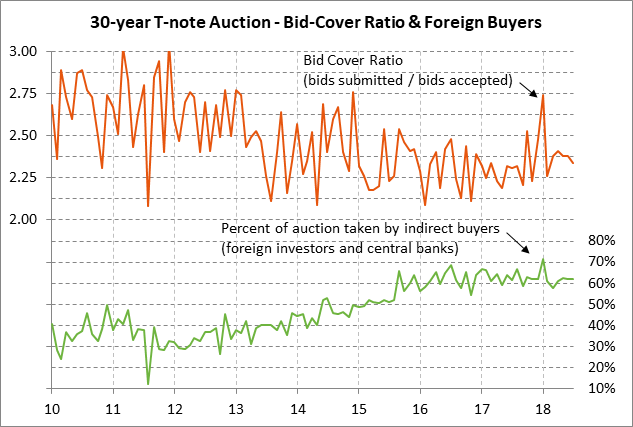

30-year T-bond auction expected to yield near 3.12% — The Treasury today will sell $18 billion of new 30-year T-bonds, concluding this week’s refunding operation. The $18 billion size of today’s 30-year bond auction is a record high and is up by $1 billion from May’s refunding bond and by $3 billion from the $15 billion size that prevailed in 2015/16. The Treasury is being forced to substantially raise the size of its auctions to cover the larger budget deficit that has resulted from the Jan 1 tax cuts and the increase in government spending.

Today’s 30-year bond issue was trading at 3.12% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of 0.98% against the current 30-year breakeven inflation expectations rate of 2.14%.

The 30-year bond yield has been in a neutral trend over the last five months, moving sideways in the range of about 2.90-3.15%. The 30-year bond yield rose by about 50 bp from the 2.70% area in December when the Jan 1 tax cut bill was passed to reach an 3-3/4 year high of 3.26% in May. The 30-year bond yield has been pushed higher by (1) rising inflation, (2) the strong economy, and (3) the Fed’s steady rate-hike regime. Factors keeping a lid on the 30-year yield include (1) trade tensions, (2) Washington political uncertainty, and (3) Eurozone uncertainty tied to Brexit and the populist Italian government.

The 12-auction averages for the 30-year are: 2.39 bid cover ratio, $6 million in non-competitive bids to mostly retail investors, 4.5 bp tail to the median yield, 37.7 bp tail to the low yield, and 35% taken at the high yield. The 30-year is slightly below average in popularity among foreign investors and central banks. Indirect bidders took an average of 62.5% of the last twelve 30-year T-bonds, which is mildly below the median of 63.3% for all recent Treasury coupon auctions.

Italian bond spread is near a 6-week high on budget worries — The 10-year Italian bond yield is currently trading at 2.91%%, which represents a 252 bp premium to the German bund yield. The yield spread of 252 bp is near a 6-week high and is only 38 bp below May’s 5-year high of 290 bp.

The market is nervous about the extent to which the Italian government will defy EU authorities about meeting the annual deficit cap of 3% of GDP. The populist Italian government is under pressure to make good on its campaign promises whereby the League promised a big tax cut and Five Star promised a minimum income to the poor.

Prime Minister Conte on Wednesday suggested that those measures could be introduced progressively to reduce the up-front cost. However, he was quickly corrected by the Five Star and League leaders who said that the measures must be implemented immediately. The Italian government seems to be planning to put whatever pressure is necessary on EU officials to get an exception to the 3% deficit rule or to change the rule altogether. The budget time-line is for the Italian government to set new deficit targets in late September, submit a draft budget to the EU for review by Oct 15, and receive final parliamentary approval of the budget by year-end.