- Powell’s testimony will be assessed for the extent of the Fed’s worries about tariffs and inflation

- U.S. June industrial production expected to rebound

- U.S. NAHB housing index expected steady

Powell’s testimony will be assessed for the extent of the Fed’s worries about tariffs and inflation — Fed Chair Powell will appear today before the Senate Banking Committee to present the Fed’s semi-annual monetary policy report and answer lawmakers’ questions. Mr. Powell will then repeat today’s performance tomorrow before the House Financial Services Committee. The Fed already released its semi-annual monetary policy report to the public last Friday. The report was in line with the Fed’s recent themes and said the FOMC expects “further gradual increases” in the funds rate.

The markets are mainly interested in hearing from Mr. Powell about how worried the Fed is about trade tensions and rising inflation. Fed Chair Powell said last Thursday in an interview said that the U.S. economy is currently in a “good place” but that the Fed is hearing about a rising level of business concern about trade policy. He said that it is very hard right now to determine which way the trade situation will go, but that a protracted trade war could be “very challenging” with rising inflation and a weakening economy. In a stagflation economy, the Fed is in a Catch 22 situation since can’t cut rates to help the economy because it needs high rates to address inflation.

Regarding inflation, the June CPI last week rose to a 6-1/2 year high of +2.9% y/y and the core CPI matched the 10-year high of +2.3%. The PCE deflator is also on the rise but is still close to target so far. The PCE deflator in May rose to a 6-year high of +2.3% and the core deflator rose to a 6-year high of +2.0% y/y, thus matching the Fed’s inflation target.

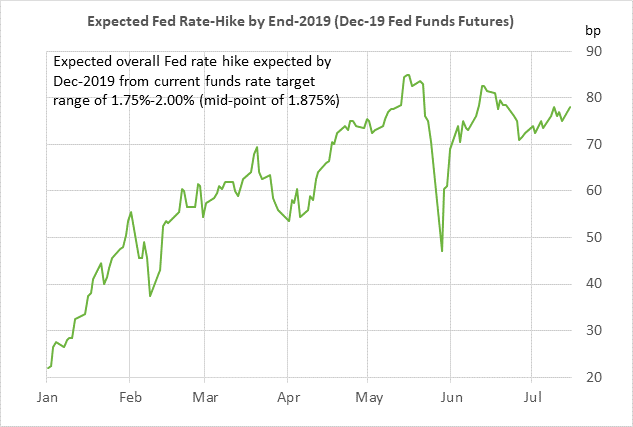

The market is currently discounting the odds at only 16% for a rate hike at the next FOMC meeting on July 31/Aug 1 since the Fed just raised its target by +25 bp to 1.75%/2.00% at its last meeting on June 12-13. However, the market is then discounting the odds of a rate hike at 100% at the following meeting on Sep 25-26 to 2.00%/2.25%. That would be the third rate hike of the year. The market is then discounting the odds at 66% that the FOMC by its Dec 18-19 meeting will implement its fourth rate hike of the year to 2.25%/2.50%.

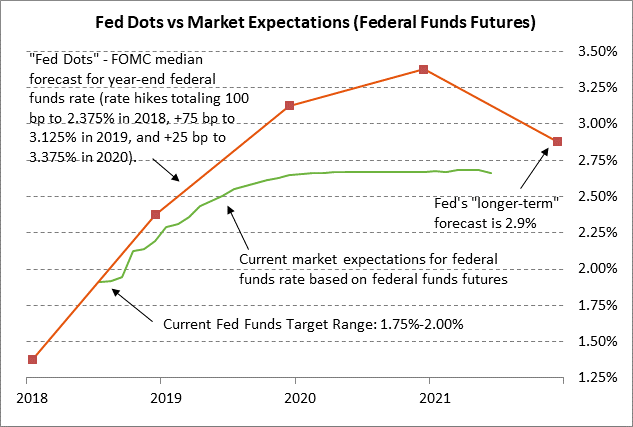

We believe that the odds are strong that the FOMC will in fact raise rates four times this year to 2.25%/2.50%, which would be in line with the Fed-dot forecast. At that level, the funds rate would finally be above the expected 10-year inflation rate of 2.11% and would finally climb into positive inflation-adjusted territory for the first time in a decade. With the unemployment rate near a 48-year low and with core inflation at the Fed’s 2.0% target, there is no excuse for the funds rate at present to be at a negative real level. The Fed also needs to get the funds rate higher so it has some room on the downside to cut interest rates whenever the next recession comes around.

The market continues to be significantly more dovish than the Fed for 2019 and beyond. The Fed dots indicate that the FOMC members expect a total of 125 bp of rate hikes from the current level to 3.25/3.50% by late 2020. However, the market is expecting only another 75 bp of rate hikes by the end of 2019 to 2.50/2.75%, which would mean that the funds rate would not even rise as high as the Fed’s longer-term forecast of 2.9%.

The market just a month ago had expected another 100 bp of rate hikes to the Fed’s long-term target of 2.9%. However, the market has turned more dovish in the past several weeks by about 25 bp mainly because of trade tensions. The U.S. and China implemented a 25% tariff of $34 billion worth of goods on July 6 and are expected to add $16 billion to that tally by the end of this summer. Then President Trump on July 10 announced that the U.S. plans for a 10% tariff on $200 billion worth of Chinese goods after Aug 30. President Trump also has plans in the works to levy a 25% tariff on all U.S. auto imports and/or a 20% tariff on auto imports from Europe.

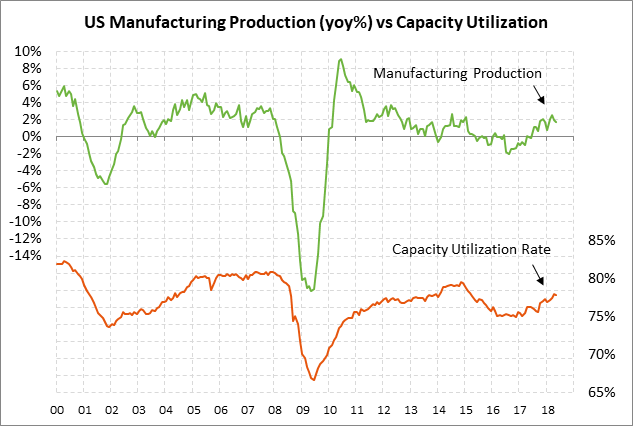

U.S. June industrial production expected to rebound — The market consensus is for today’s June industrial production report to rebound by +0.5% m/m after May’s weak report of -0.1%. Isolating the manufacturing sector, today’s June manufacturing production report is expected to show a large increase of +0.7%, exactly offsetting May’s -0.7% decline. Manufacturing production took a hit in May from weak vehicle production due to supply chain disruptions.

Aside from those temporary auto-sector disruptions, the U.S. manufacturing sector remains in good shape. The ISM manufacturing index in June rose by +1.5 points to 60.2, which was just 0.6 points below February’s 14-year high of 60.8. That shows that confidence among U.S. manufacturing executives is very high. Moreover, the future looks favorable with the ISM manufacturing new orders sub-index even higher than the overall index at 63.5, indicating a strong order-flow pipeline.

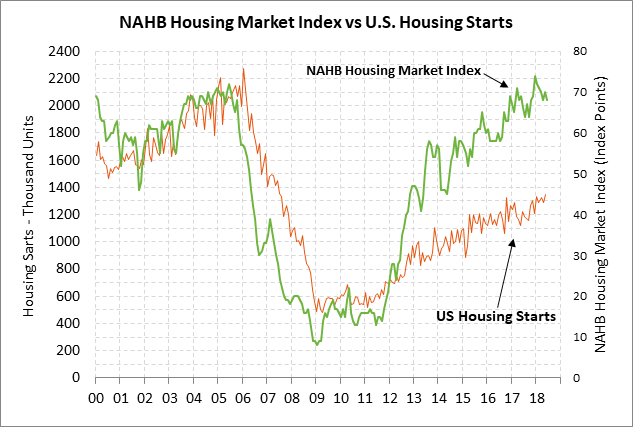

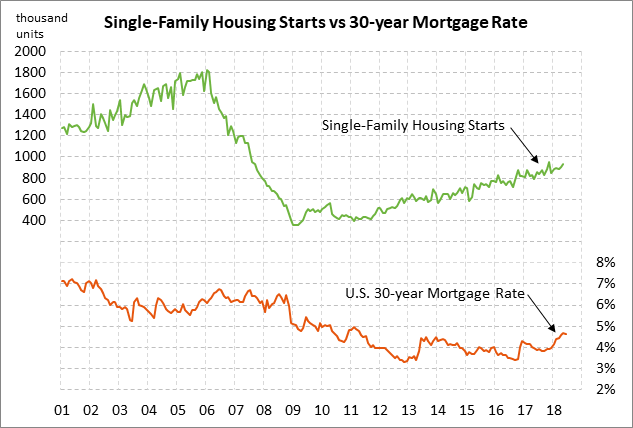

U.S. NAHB housing index expected steady — The market consensus is for today’s July NAHB housing market index to be unchanged at 68 following June’s -2 point decline to 68. The index peaked at a 19-year high of 74 in December 2017 and has since eased by 6 points to a 9-month low of 68 mainly because of higher mortgage rates. The current 30-year mortgage rate in the past 10 months has risen by 75 bp to the current level of 4.53%.

Yet, U.S. home builder confidence remains generally strong due to strong home sales and high prices for new homes. U.S. new home sales in May rose by +6.7% to 689,000 where the series was just 3.2 points below the 10-year high of 712,000 units posted in Nov 2017. Meanwhile, the median price of a new home was $313,000 in May, which was just 9% below the record high of $343,400 posted in Nov 2017.