- Weekly market focus

- Fed policy will dominate the week

- Q2 earnings season begins with strong expectations

- U.S. retail sales expected to show strength for the fourth month in a boost to Q2 GDP

Weekly market focus — The U.S. markets this week will focus on (1) whether today’s Trump-Putin summit meeting in Helsinki has any market-moving elements, (2) Fed Chair Powell’s semi-annual testimony to Congressional committees on Tuesday and Wednesday, (3) any developments on the trade front after President Trump last week announced that he will slap a 25% tariff on an additional $200 billion of Chinese goods to take effect after Aug 30, (4) the first big week of Q2 earnings season with 61 of the S&P 500 companies scheduled to report, (5) the Treasury’s sale of $13 billion of 10-year TIPS on Thursday, and (6) this coming weekend’s meeting of G-20 finance ministers and central bankers in Buenos Aires.

The Asian markets will continue to focus on the Chinese stock market and the yuan, both of which remain weak on trade tensions and on worries about slower Chinese economic growth. The Shanghai Composite index has rebounded higher by a total of +5.7% thus far from the early-July 2-1/4 year low, but remains on the defensive and is still down -14.4% year-to-date. The Chinese yuan last week closed -0.74% lower at 6.6916 yuan/USD where it was just mildly above the 11-month low of 6.7214 yuan/USD posted in early July. The Japanese markets are closed today for a national holiday.

In Europe, the focus will mainly be on Brexit as Prime Minister May this week will continue to struggle to keep her government together as she seeks support for her soft Brexit plan. Wednesday’s UK June CPI is expected to strengthen to +2.6% y/y from May’s +2.4% but the core CPI is expected to be unchanged at an acceptable +2.1% y/y. The European economic calendar this week is light.

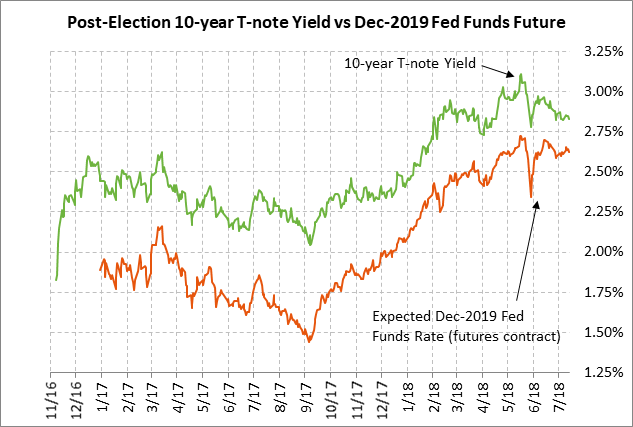

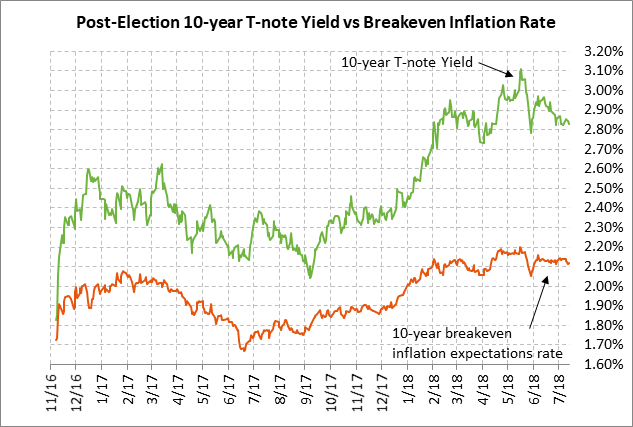

Fed policy will dominate the week — Fed policy will dominate market attention this week as Fed Chair Powell appears before the Senate Banking Committee on Tuesday and before the House Financial Services Committee on Wednesday. In addition, the Fed will release its Beige Book report on Wednesday. Fed Chair Powell in this week’s testimony will expand on the semi-annual monetary policy report that the Fed released last Friday. The report was in line with the Fed’s recent themes and said the FOMC expects “further gradual increases” in the funds rate.

The markets are mainly interested in hearing how worried the Fed is about trade tensions and rising inflation. Fed Chair Powell last Thursday said in an interview said that the U.S. economy is currently in a “good place” but that the Fed is hearing a rising level of business concern about trade policy. He said that it is very hard right now to determine which way the trade situation will go, but that a protracted trade war could be “very challenging” with rising inflation and a weakening economy.

Regarding inflation, the June CPI last week rose to a 6-1/2 year high of +2.9% y/y and the core CPI matched the 10-year high of +2.3%. The PCE deflator is also on the rise but is near target so far. The PCE deflator in May rose to a 6-year high of +2.3% and the core deflator rose to a 6-year high of +2.0% y/y, thus matching the Fed’s inflation target.

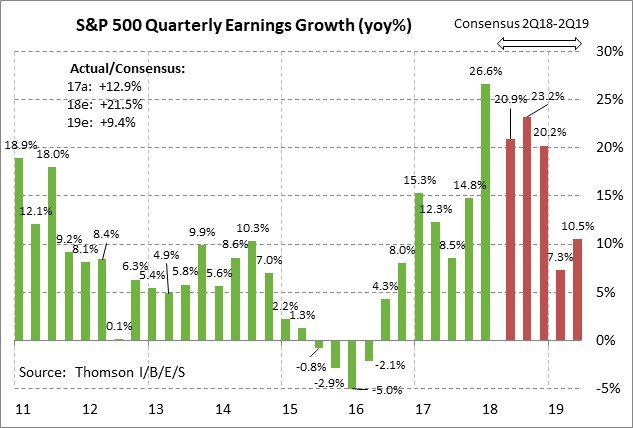

Q2 earnings season begins with strong expectations — This will be the first busy week of the Q2 earnings season with 61 of the S&P 500 companies scheduled to report. Notable reports include Netflix and Bank of America on Monday; Goldman Sachs on Tuesday; Morgan Stanley, eBay, American Express, and IBM on Wednesday; Microsoft and Capital One on Thursday; and GE and Honeywell on Friday.

The market consensus is for very strong SPX Q2 earnings growth of +20.9% y/y, which would be down from Q1’s +26.6% but would still be a very strong figure. Earnings growth is then expected to remain above 20% in the second half of this year at +23.2% in Q3 and +20.2%, according to Thomson I/B/E/S. On a calendar year basis, the consensus is for very strong SPX earnings growth this year of +21.5%. Earnings growth is then expected to decelerate to +9.5% in 2019 as the effects start to wear off from the Jan 1 tax cuts.

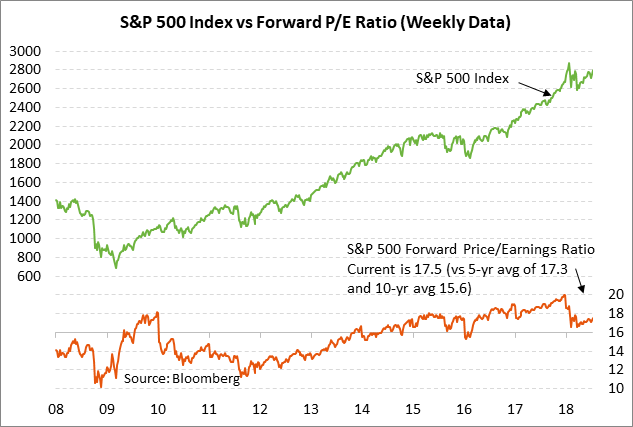

Valuation levels have become more reasonable due to the strength in earnings and the downward correction in stock prices seen since February. The current forward P/E for the S&P 500 index of 17.5 is just slightly above the 5-year average of 17.3 and is just moderately above the 10-year average of 15.6.

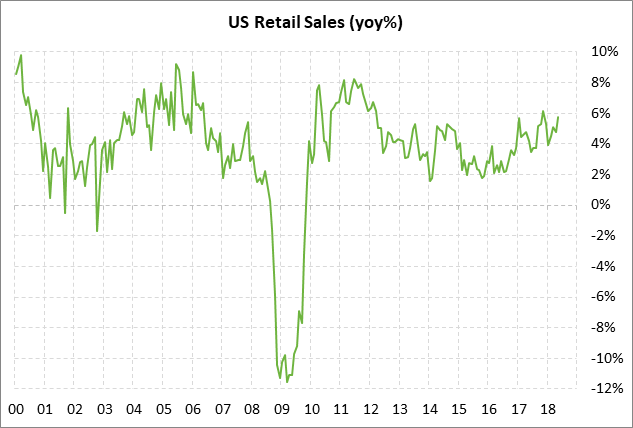

U.S. retail sales expected to show strength for the fourth month in a boost to Q2 GDP — The consensus is for today’s June retail sales report to show a respectable increase of +0.5% and +0.3% ex autos, adding to May’s very strong report of +0.8% and +0.9% ex autos. After weakness in Dec-Feb, retail sales then strengthened substantially to +0.7% in March, +0.4% in April, and +0.8% in May. On a year-on-year basis, retail sales in May rose by +5.8% y/y, which was just 0.3 points below the 6-year high of +6.1% posted in Nov 2017.

U.S. consumer spending kicked into high gear in the last three reporting months (March-May) due to strong consumer confidence and larger paychecks after the Jan 1 tax cuts. Personal spending contributed only 0.60 points to the Q1 GDP report of +2.0%, which was much weaker than the 2017 average of nearly +2.0 points. However, the Atlanta Fed’s GDP Now is expecting personal spending to contribute a much stronger +1.84 points to GDP in Q2, which is the key factor behind their strong Q2 GDP forecast of +3.9%. The second strongest contribution to Q2 GDP is expected to be from net exports with a +0.70 point contribution thanks to heavy overseas buying of some U.S. products such as soybeans to beat the U.S. implementation of tariffs.