- Markets will assess today’s Fed report for the level of Fed’s concern about trade tensions and inflation

- U.S. consumer sentiment expected to remain strong

- Stronger U.S. import prices expected to put upward pressure on U.S. inflation

Markets will assess today’s Fed report for the level of Fed’s concern about trade tensions and inflation — The Fed today will release its semi-annual monetary policy report that Fed Chair Jerome Powell will present when he testifies before Congress next week in the semi-annual hearings on monetary policy. The markets are hoping to get a better idea of how worried the Fed is about tariffs and about whether the Fed’s is growing more concerned about rising inflation.

Mr. Powell in an interview yesterday said that the U.S. economy is currently in a “good place,” but that the Fed is hearing a rising level of business concern about trade policy. He said that it is very hard right now to determine which way the trade situation will be go, but that a protracted trade war could be “very challenging” with rising inflation and a weakening economy.

Trade effects at this point are limited since the U.S. economy is currently growing at a very strong rate and since the tariff amounts aren’t particularly high as yet. The market consensus is for Q2 GDP to show a strong increase of +3.4% and there some forecasts of +4% or even +5%. U.S. GDP in Q2 got a big boost from the Jan 1 tax cuts and from big overseas sales of U.S. goods such as soybeans to try to beat the start of the tariffs.

Meanwhile, the tariff amounts aren’t particularly high as yet when compared to the size of the overall U.S. economy. President Trump has thus far enacted tariffs on $85 billion worth of U.S. imports, which accounts for only about 3.6% of total imports ($2.4 trillion in 2017), according to the Washington Post’s tariff tracker.

However, the impact on the U.S. economy is compounded by the fact that most countries have retaliated against the Trump tariffs with their own tariffs on some $56 billion worth of U.S. exports, which will slightly reduce U.S. exports and thus reduce U.S. economic growth.

While the tariff impact at the macro level is modest for now, that could quickly change if President Trump proceeds with his plan for a 10% tariff on another $200 billion of Chinese goods and a 20% tariff on imported European autos. Those tariffs would put a clear dent in the U.S. economy and could also boost inflation to the point where the Fed might have to respond with an accelerated rate-hike regime.

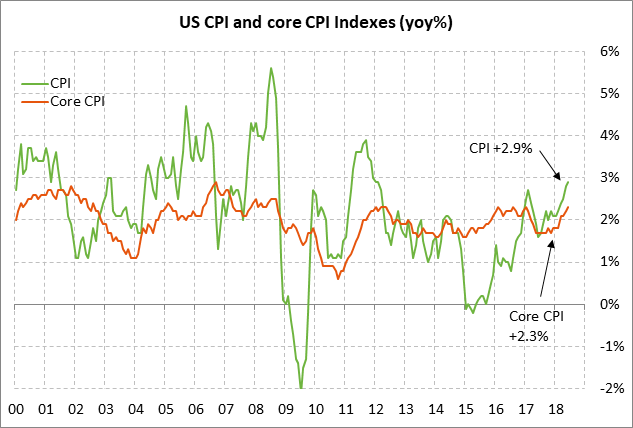

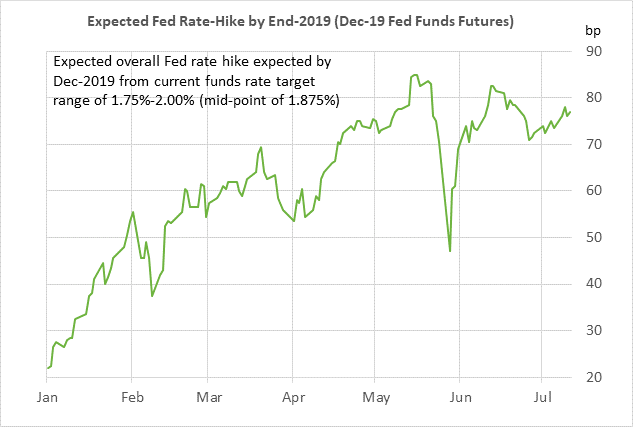

Regarding rate hikes, the Fed report and Fed Chair Powell’s testimony next week are likely to stick to their mantra about slow and steady rate hikes. This week’s PPI and CPI reports showed strength and reinforced the fact that the Fed must continue to raise interest rates. Yesterday’s June CPI rose to a new 6-1/2 year high of +2.9% y/y and the core CPI matched a 10-year high of +2.3% y/y. In fact, we think there is a stronger chance for the Fed’s fourth rate hike in December than the current market estimate of 66%.

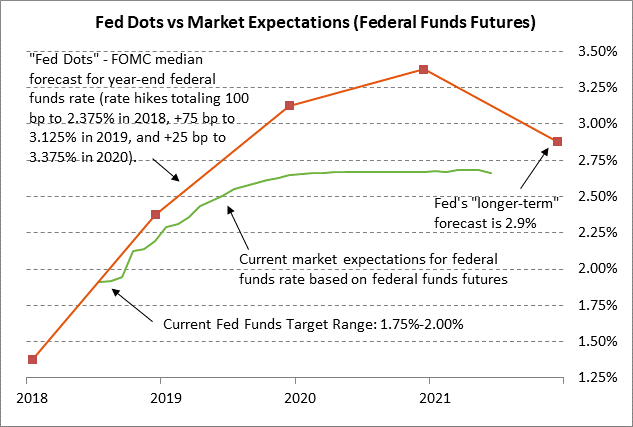

However, if the trade turmoil worsens, then the Fed may need to curb its tightening moves in 2019 and 2020. The Fed dots indicate that the Fed expects to raise its funds rate to over 3.25% by late 2020. However, the market is substantially more dovish and is expecting only about 75 bp of rate hikes to 2.6% by early-2020. If trade tensions worsen substantially, the Fed could conceivably only be able to raise interest rates by another 50 bp.

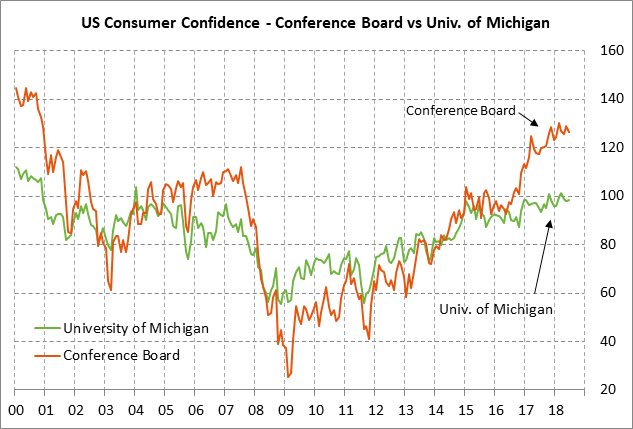

U.S. consumer sentiment expected to remain strong — The market consensus is for today’s preliminary-July University of Michigan U.S. consumer sentiment index to show a small -0.2 point decline to 98.0, reversing June’s small +0.2 point increase to 98.2. U.S. consumer confidence is in very strong shape at only 3.2 points below March’s 14-year high of 101.4.

U.S. consumer sentiment is being boosted by (1) the strong U.S. economy and labor market, (2) rising income and wages, (3) rising household wealth from the generally strong stock market and the steady rise in home prices, and (4) increased cash from the Jan 1 tax cuts.

Threats to consumer sentiment include (1) concern about the shaky stock market and trade tensions, (2) the Fed’s rate hikes and rising mortgage rates, (3) high gasoline prices, and (4) Washington political uncertainty.

Stronger U.S. import prices expected to put upward pressure on U.S. inflation — The market consensus is for today’s June import price index to rise to +4.6% y/y from May’s +4.3% y/y. The expected report of +4.6% y/y would be just 0.1 point below the 19-year high of +4.7% posted in Feb 2017.

The strength in import prices will put upward pressure on the overall U.S. inflation indexes. Import prices are being inflated by (1) strong U.S. demand, (2) high oil prices, (3) dollar weakness through early 2017, and (4) new tariffs on about $85 billion worth of U.S. imports.

U.S. inflation pressure is on the rise, causing concern for the Fed. The PCE deflator, which is the Fed’s preferred inflation measure, rose to a 6-year high of +2.3% in May and the core PCE deflator rose to a 6-year high of +2.0%, matching the Fed’s inflation target.

The Fed has said that it will tolerate a mild overshoot of its 2.0% inflation target since its target is symmetrical. However, it is possible that the U.S. inflation rate will rise much farther above the Fed’s target due to the various upward pressures, thus putting the Fed behind the inflation curve.