- U.S. job openings expected to remain strong

- 3-year T-note auction to yield near 2.66%

- Chinese stocks rebound despite ongoing trade tensions

- Sterling is whipsawed by May cabinet defections

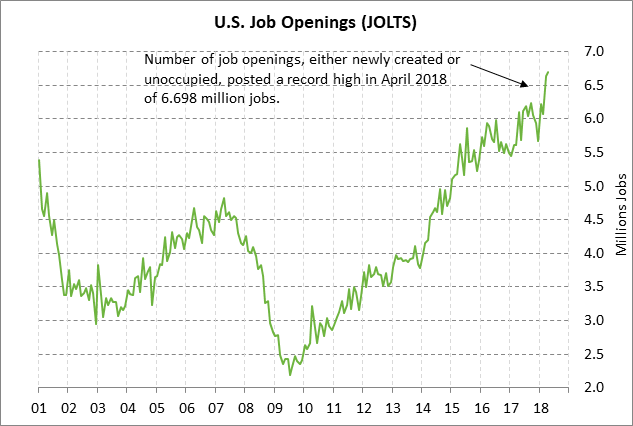

U.S. job openings expected to remain strong — The market is expecting today’s May JOLTS job openings report to show a decline of -43,000 to 6.655 million, giving back part of April’s +65,000 increase to a record high of 6.698 million.

Despite today’s expected decline, the job openings series will remain in very strong shape near April’s record high, indicating that many businesses are looking to hire new employees. The JOLTS job openings series is a leading indicator for the payroll report since many job openings will turn into an actual job hire within 1-3 months when the hiring process is complete.

The U.S. labor market remains very strong as shown by last Friday’s June payroll report of +213,000. Payrolls over the last six months have shown a strong monthly average increase of +215,000. The U.S. economy continues to produce a solid number of jobs even though employees are becoming harder to find. The June unemployment rate last Friday’s rose by +0.2 points to 4.0% from May’s 48-year low of 3.8%, but a 4.0% unemployment rate still indicates a tight labor market.

Despite the tight labor market, wages so far remain under wraps. Last Friday’s June average hourly earnings report of +2.7% y/y was unchanged from May and was 0.1 point below January’s 9-year high of +2.8% y/y.

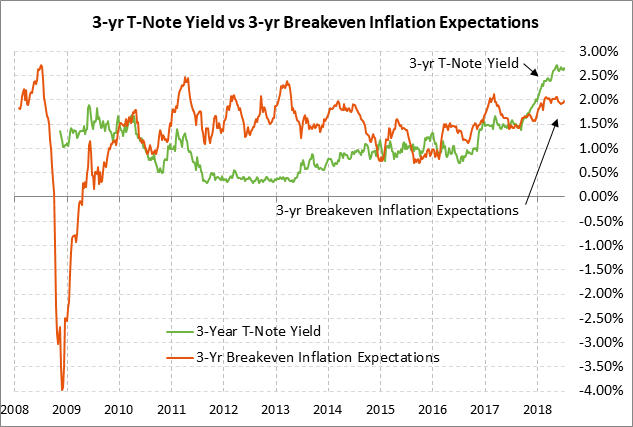

3-year T-note auction to yield near 2.66% — The Treasury today will sell $33 billion of 3-year T-notes. The Treasury will then continue this week’s $69 billion coupon package by selling $22 billion of 10-year T-notes on Wednesday and $14 billion of 30-year bonds on Thursday. This week’s 10-year and 30-year auctions will be the second and final reopenings of the securities that the Treasury first sold in May.

Today’s 3-year T-note issue was trading at 2.66% in when-issued trading late yesterday afternoon. That translates to an inflation-adjusted yield of 0.68% against the current 3-year breakeven inflation expectations rate of 1.98%. The 3-year T-note yield is currently trading just 11 bp below May’s 10-year high of 2.77%.

The 12-auction averages for the 3-year are as follows: 2.91 bid cover ratio, $70 million of non-competitive bids taken mostly by retail investors, 4.3 bp tail to the median yield, 28.1 bp tail to the low yield, and 57% taken at the high yield. The 3-year is the second least popular security among foreign investors and central banks behind the 2-year T-note. Indirect bidders, a proxy for foreign buyers, have taken an average of only 52.4% of the last twelve 3-year T-note auctions, which is well below the median of 63.3% for all recent coupon auctions.

Chinese stocks rebound despite ongoing trade tensions — The Chinese stock market on Monday finally staged a partial recovery rally after the relentless 3-week sell-off to last Friday’s 2-1/4 year low. The Shanghai Composite index on Monday rallied by +2.47% to a 1-week high.

Stocks rallied on Monday after selling pressures finally ebbed and short-covering took over. Stocks were also supported by the fact that the Chinese yuan on Monday rose by +0.40% against the dollar, recovering somewhat from last Tuesday’s 1-year low. The recovery in the yuan reduced capital-flight concerns sparked by the concurrent sell-off in both Chinese stocks and the yuan.

Yet the fundamental situation in China remains tenuous as Chinese investors wait for the next shoe to drop on tariffs. The U.S. and China last Friday implemented reciprocal 25% tariffs on $36 billion worth of goods. The next tariff tranche of $16 billion is expected by later this summer. The markets are also waiting to see whether President Trump will follow through with his threat to slap tariffs on another $200 billion worth of Chinese products.

Sterling is whipsawed by May cabinet defections — The markets were initially encouraged by Prime Minister May’s cabinet meeting last Friday in which she threw down the gauntlet and told her cabinet to either support her soft Brexit plan or resign from the cabinet. However, things then started to fall apart on Sunday when her chief Brexit negotiator David Davis and his deputy resigned from the cabinet. Ms. May on Monday quickly appointed a young euroskeptic Dominic Raab as her new Brexit negotiator.

The situation then took another turn for the worse after Foreign Secretary Boris Johnson resigned late Monday with a harsh statement against Ms. May’s Brexit plan. Ms. May moved quickly to install Health Secretary Jeremy Hunt as the new Foreign Secretary. GBPUSD rallied to a 3-1/2 week high on Monday morning but then fell back and closed the day little changed.

It is possible that Ms. May will be better off with the dissenters out of the cabinet so she can focus on developing a Brexit plan that can get enough political support to be approved by Parliament this autumn. However, the markets remain concerned that the hard-line Brexiteers may yet mount a leadership challenge to Ms. May. A leadership challenge would make it all the more difficult for the UK to meet the deadlines for negotiating a Brexit agreement with the EU. In addition, now that Boris Johnson is out of the cabinet, he will be in a prime position to step up his attacks on Ms. May to see if he can oust her as Prime Minister.