- Weekly market focus

- US/Chinese tariff deadline is now only four days away

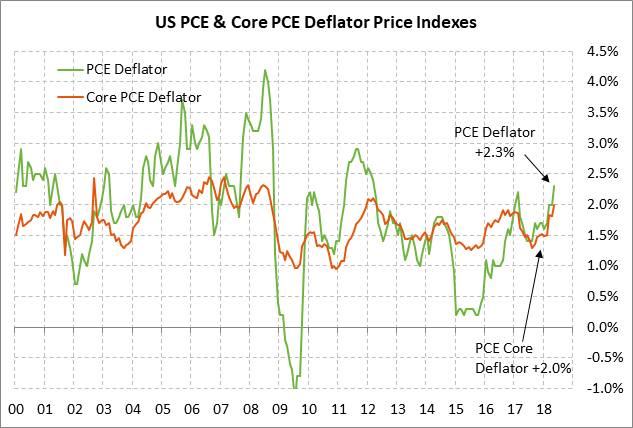

- U.S. inflation expectations rise after new 6-year high in PCE deflator

- U.S. ISM manufacturing index expected to remain strong

Weekly global market focus — The U.S. markets this week will focus on (1) U.S./Chinese trade tensions ahead of Friday’s (July 6) implementation date for reciprocal tariffs on $34 billion of U.S. and Chinese products, (2) this week’s fairly busy economic schedule capped by Friday’s June unemployment report (payrolls expected +195,000 and the unemployment rate expected unchanged at 3.8%), (3) Thursday’s June 12-13 FOMC meeting minutes, which may provide some additional color to assess whether the Fed will raise interest rates four times this year, and (4) T-note prices and inflation expectations after last Friday’s May PCE deflator report rose to 6-year highs of +2.3% y/y headline and +2.0% y/y core.

The Mexican and U.S. markets today will react to Sunday’s election in Mexico where left-wing Andres Manuel Lopez Obrador was expected to easily win. Mr. Obrador is expected to take a tougher line on NAFTA negotiations with the U.S, which may result in an eventual decision by President Trump to withdraw from NAFTA. Also on the trade front, Canada’s retaliatory tariffs on $12.8 billion worth of U.S. goods took effect yesterday, which may elicit a new trade threat from President Trump.

The European markets are focused on German politics after the EU summit late last week and the subsequent German coalition meetings. German Chancellor Merkel won some concessions on migration at the EU meeting but it remains to be seen whether those concessions will be sufficient to maintain support for her coalition from the CSU party.

Meanwhile, UK Prime Minister May this Friday will hold critical talks with her cabinet to try to thrash out a common Brexit position.

In Asia, the markets today will react to last Friday night’s news that the Chinese June manufacturing PMI fell by -0.4 points to 51.5, which was slightly weaker than market expectations of -0.3 to 51.6. However, the June non-manufacturing PMI rose by +0.1 point to 55.5, which was slightly stronger than market expectations of -0.1 to 54.8. Sunday night’s July Caixin Chinese manufacturing PMI was expected to be unchanged at 51.1. Sunday night’s Japan large-manufacturer Tankan report was expected to show a -2 point drop to 22 from 24.

US/Chinese tariff deadline is now only four days away — There are now only four days left until this Friday (July 6), when the reciprocal 25% tariffs on $34 billion worth of U.S. and Chinese products go into effect. There seems to be little hope for those tariffs to be averted considering that the U.S. and China are miles apart on their trade positions and there seem to be no serious negotiations. The most that the markets can hope for is perhaps a postponement of the tariff implementation date if the two sides at the last minute decide to engage in serious negotiations in an attempt to reach a comprehensive trade deal.

Also on the trade front, the markets are nervous that Mr. Trump could be getting close to officially announcing a 20% tariff on European auto imports. Mr. Trump last Tuesday said that “we are finishing our study on tariffs on cars from the EU” even though Mr. Trump just announced that specific idea a few days earlier. The EU will undoubtedly launch another round of retaliatory tariffs against U.S. exports to Europe if the Trump administration goes through with its tariffs on EU autos.

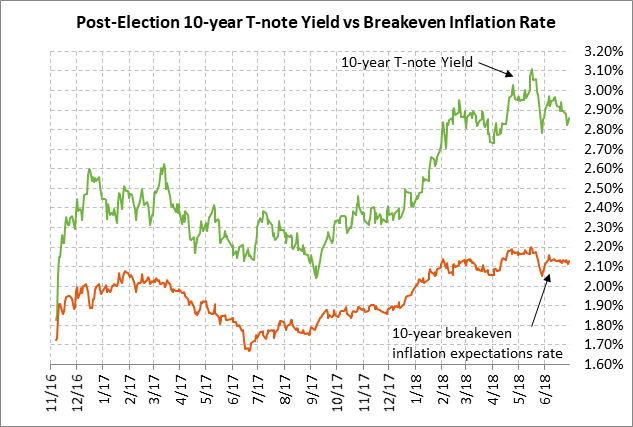

U.S. inflation expectations rise after new 6-year high in PCE deflator — The 10-year T-note yield last Friday rose by +2 bp to 2.86% on the stronger than expected PCE deflator report and the rise in inflation expectations. The 10-year breakeven inflation expectations rate last Friday rose by +2 bp to 2.13%.

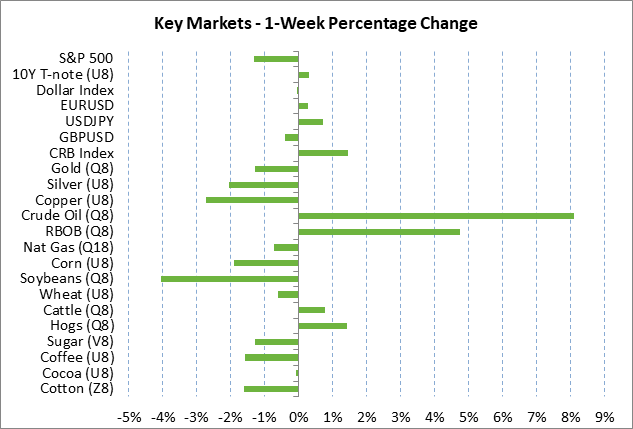

Inflation expectations also rose after Aug WTI crude oil prices last Friday rose to a new 3-1/2 nearest-futures high of $74.46. President Trump over the weekend said he talked with Saudi King Salman and that the King agreed to boost Saudi oil production by 2 million bpd. However, Saudi Arabia then put out a statement saying that King Salman simply referred to 2 million bpd of spare capacity and said Saudi Arabia would use that excess capacity prudently if necessary to ensure market balance and stability.

Friday’s May PCE deflator rose to a new 6-year high of +2.3% and the May core PCE deflator rose to a 6-year high of +2.0%. The rise in the core PCE deflator to match the Fed’s +2.0% inflation target could turn out to be a watershed event if the core deflator keeps on rising. However, the Fed has already said that it will accept at least a mild rise in inflation above its target since that target is symmetrical.

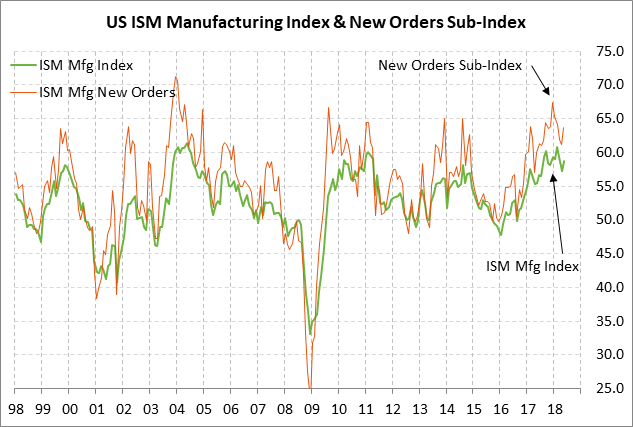

U.S. ISM manufacturing index expected to remain strong — The consensus is for today’s June ISM manufacturing index to show a -0.5 point decline to 58.2, giving back about a third of May’s +1.4 point increase to 58.7. The ISM index is in strong shape at only 2.1 points below February’s 14-year high of 60.8.

Manufacturing confidence remains strong due to the strong U.S. economy and increased capex spending following the Jan 1 tax cuts. The decline in the dollar index in 2017 was also helpful for manufacturing exports, although the dollar in recent months has recovered to a 1-year high. The ISM new orders index was strong in May with a +2.5 point increase to 63.7, indicating that the orders pipeline is full and will support ongoing strength in production and shipments.