- Will U.S. trade attack blow over China’s house of cards?

- Reports firm up that Trump administration will take measured steps on investment restrictions

- Q1 U.S. GDP expected to be left unrevised

- 7-year T-note auction to yield near 2.78%

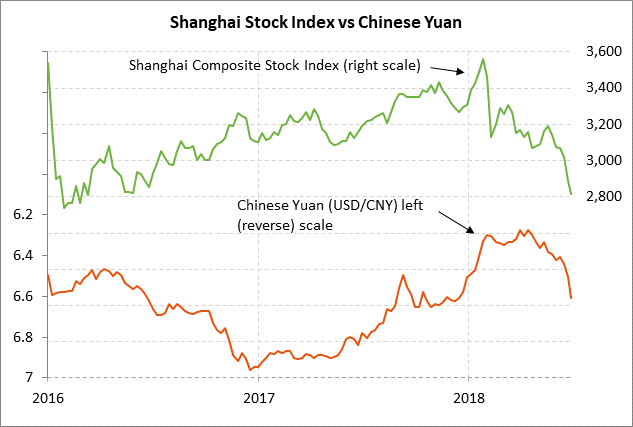

Will U.S. trade attack blow over China’s house of cards? — The Chinese markets are close to slipping into a panic mode as both the Chinese stock market and the yuan fall together in what could become a worsening downward spiral. The Chinese Shanghai Composite index in the past five months has fallen by 22% to a 2-year low from January’s 2-1/2 year high, which is a sell-off that qualifies for a bear market since it is more than 20%. Meanwhile, the Chinese yuan has plunged by -3.2% in the past two weeks to a 6-1/2 month low.

The highly correlated sell-off in China’s stock market and its currency is disturbing because of the duo’s bad history. Back in 2015 when the Chinese government tried to engineer a yuan devaluation, the Chinese stock market went into a free-fall in which about $5 trillion of market cap was lost. The Chinese government ended up stopping the panic by being forced to (1) impose much stricter currency controls to prevent capital flight, and (2) spend about $1 trillion of reserves to halt the yuan’s decline.

When the Chinese stock market falls, Chinese investors start to withdraw money and some investors try to move that money out of China if they are worried about the country’s overall direction. That yuan weakness and capital flight can then cause even bigger worries about holding depreciating Chinese assets, thus causing even more stock selling. This is the negative feedback loop whereby the stock market and yuan fall together.

The Chinese stock market and yuan currently have common bearish factors such as weaker Chinese economic data after May’s weaker-than-expected retail sales, industrial production, and investment reports. The yuan is also seeing weakness because the Chinese central bank (PBOC) last weekend announced a 50 bp cut in banks’ required reserve ratio (RRR) to boost bank liquidity and provide some support for stocks. However, the extra liquidity was bearish for the yuan.

The PBOC is in a tough spot at present because it cannot cut interest rates without sparking a fresh plunge in the yuan, which would grease the skids for stocks. The PBOC is therefore walking the tightrope of using an RRR cut to support stocks while keeping interest rates stable in the hopes of not causing undue yuan weakness.

In the bigger picture, China faces major problems at present including massive corporate and household debt levels, increasing corporate debt defaults, excess capacity in many industries, and an attack by the U.S. on no less than its fundamental economic development model. China has been able to muddle through its many problems in the past, but if the U.S./Chinese trade war expands to $250 billion or especially $450 billion, then the markets may soon find out whether China is actually a house of cards waiting for an ill wind to blow it over.

Reports firm up that Trump administration will take measured steps on investment restrictions — There were various media reports on Wednesday confirming Tuesday’s ideas that the Trump administration plans to take a measured approach on limiting foreign investment in U.S. technology. The administration is due to officially announce its plan by Friday.

The Trump administration will reportedly rely on Congress to beef up the power of the Committee on Foreign Investment in the U.S. (CFIUS) to halt or limit investment by China and other countries in sensitive areas of U.S. technology or infrastructure. That would be a more measured approach than fears that the Trump administration might use a dusty 1977 law called the International Emergency Economic Powers Act to block foreign investment in a broad and haphazard manner.

Also on the trade front, there are now only 8 days left until next Friday (July 6), when the reciprocal 25% tariffs on $34 billion worth of U.S. and Chinese products go into effect. There seems to be little hope for those tariffs to be averted considering that the U.S. and China are miles apart on their trade positions and that there seem to be no serious negotiations at this point.

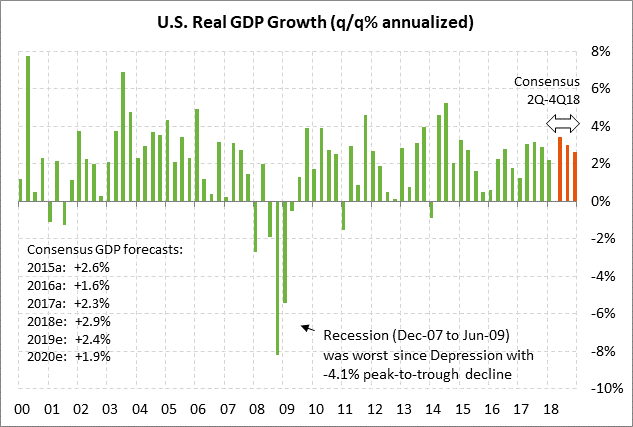

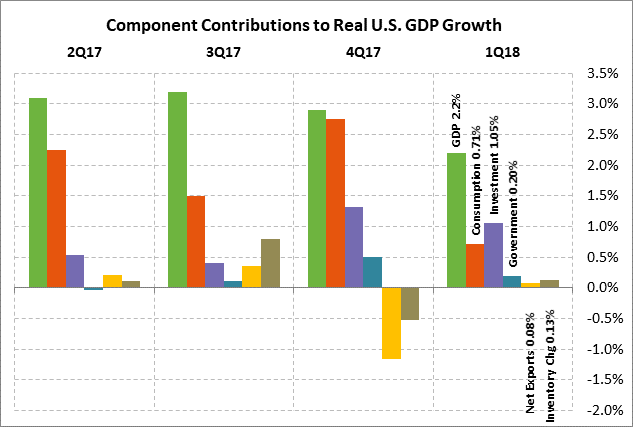

Q1 U.S. GDP expected to be left unrevised — The market consensus is for today’s Q1 GDP to be left unrevised at 2.2% and for Q1 personal consumption to be left unrevised at +1.0%. The lackluster growth seen in Q1 was mainly due to soft consumer spending and the residual seasonal effects that have plagued Q1 growth in recent years. However, the market is looking for a big improvement in Q2 GDP growth to +3.4% due to a strong improvement in consumer spending and business investment as the effects of the Jan 1 tax cuts kick into high gear. After peak growth in Q2, the consensus is then for GDP to ease to +3.0% in Q3 and +2.6% in Q4, leading to 2018 growth of +2.9%.

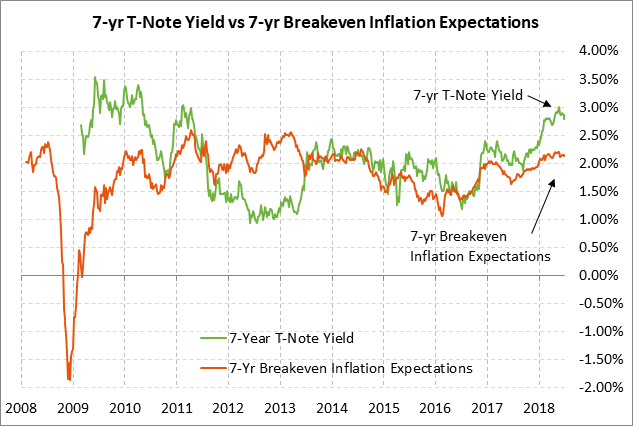

7-year T-note auction to yield near 2.78% — The Treasury today will auction $30 billion of 7-year T-notes. The $30 billion size of today’s auction is unchanged from May’s size but is up by $2 billion from the $28 billion size that prevailed during 2016/17. Today’s 7-year T-note issue was trading at 2.78% late yesterday afternoon, which was 30 bp below May’s 7-1/2 year high of 3.08%.

The 12-auction averages for the 7-year are: 2.50 bid cover ratio, $15 million in non-competitive bids to mostly retail investors, 4.6 bp tail to the median yield, 29.3 bp tail to the low yield, and 49% taken at the high yield. The 7-year is the fourth most popular coupon among foreign investors and central banks behind the 30-year, 10-year and 5-year TIPS securities. Indirect bidders, a proxy for foreign buyers, have takenan average of 65.2% of the last twelve 7-year auctions, which is moderately above the median of 63.5% for all recent coupon auctions.