- Trade tensions start to stack up for the U.S. stock market

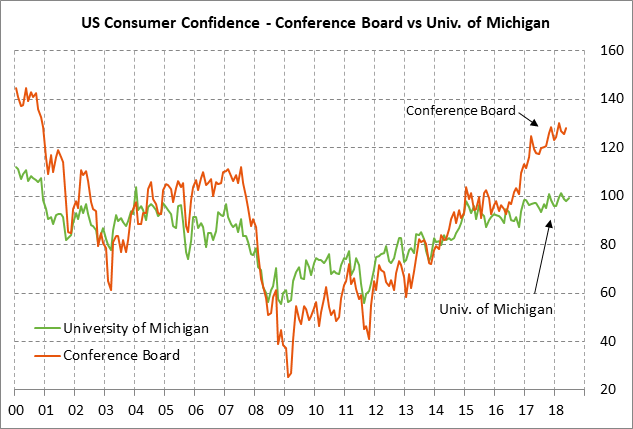

- U.S. consumer confidence expected to remain strong

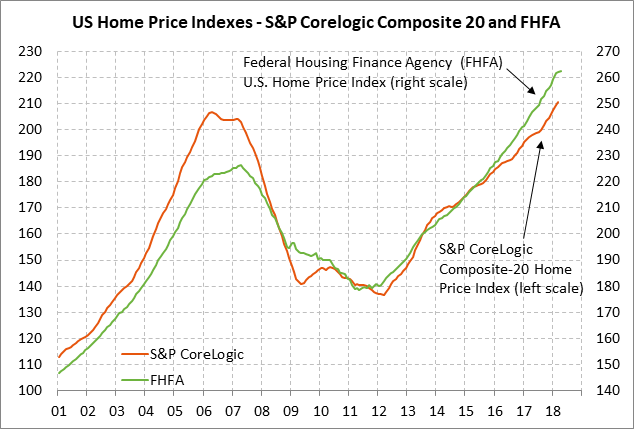

- U.S. home prices expected to show continued rise

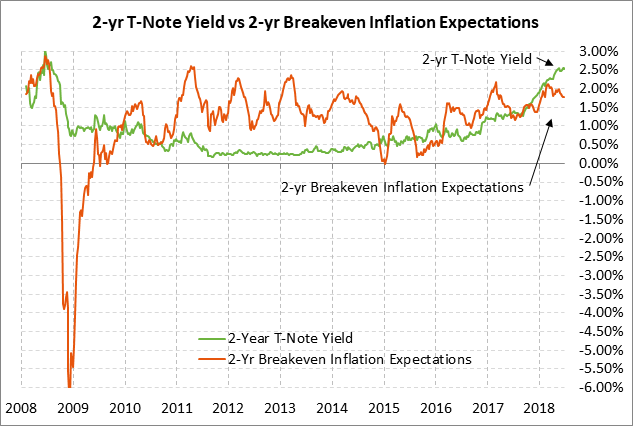

- 2-year T-note auction to yield near 2.54%

Trade tensions start to stack up for the U.S. stock market — The S&P 500 index on Monday fell to a 3-week low and closed the day sharply lower by -1.37%, although the index at least recovered somewhat from the day’s low when the index was down -2.04%. Trade tensions were the main bearish factor ahead of the Trump administration’s release by Friday of its new restrictions on Chinese investment. There were also reports that the administration will clamp down on U.S. exports of sensitive technology, which could hurt sales for some companies.

Trade tensions were highlighted in the media on Monday after Harley Davidson announced that it will move production of motorcycles destined for sale in Europe out of the U.S. to avoid the additional 25% tariff that the EU imposed last Friday in retaliation for U.S. steel and aluminum tariffs. Harley said the EU tariffs would cost the company up to $100 million annually since it will have to absorb some of the tariff cost itself until it can shift production overseas. Harley’s stock plunged by 6% on Monday. That followed Daimler’s news last week that it expects a significant hit to its earnings from increased vehicle tariffs.

The markets on Monday also reacted more fully to President Trump’s threat last Friday to slap a 20% tariff on imports of European cars. That EU threat was more specific than the administration’s investigation of a 25% tariff on all imported vehicles regardless of the country of origin.

The stock market also took a hit on Monday when Treasury Secretary Mnuchin said in an early tweet that the Treasury’s investment restrictions to be released by Friday will not be specific to China “but to all countries that are trying to steal our technology.” That made the markets worry about how extensive those investment restrictions might be. However, White House trade advisor Peter Navarro in an interview on CNBC later in the day seemed to indicate that the investment restrictions will indeed target only China, thus placating the markets somewhat and leading to a partial stock market recovery.

There are now only 10 days left until July 6, which is when the reciprocal 25% tariffs on $34 billion worth of U.S. and Chinese products go into effect. There seems to be little hope for those tariffs to be averted considering that the U.S. and China are miles apart on their trade positions and that there seem to be no serious negotiations at this point. China is hitting the U.S. agriculture particularly hard with those July 6 tariffs, including the key U.S. soybean market.

Other bearish factors for stocks included Eurozone tensions as the Italian 10-year bond yield on Monday rose sharply by +13 bp to 2.82% after the populist League party did well in Italian municipal elections on Sunday. League leader Salvini has become German Chancellor Merkel’s nemesis as she tries to hold her own coalition together on migration issues. The markets will be hoping for some progress on migration issues at the important EU Summit later this week on Thursday and Friday.

The U.S. stock market was also undercut by Monday’s -1.09% fall in the Shanghai index and its close below the -20% sell-off level that defines a bear market. The Chinese stock market remains very concerned about U.S./Chinese trade tensions and received little support from the Chinese central bank’s 50 bp cut in the required reserve ratio on Saturday, which was designed to free up some bank lending. The markets had fully expected that cut.

U.S. consumer confidence expected to remain strong — The market consensus is for today’s June Conference Board U.S. consumer confidence index to be unchanged at 128.0, holding on to May’s solid +2.4 point gain to 128.0. The index is in strong territory at only 2.0 points below February’s 17-year high of 130.

U.S. consumer confidence is receiving a boost from (1) the strong U.S. economy and labor market, (2) rising consumer income and household wealth, and (3) the Jan 1 tax cuts. Negative factors include (1) the jittery stock market, (2) trade tensions, (3) Washington political uncertainty, and (4) high gasoline prices.

U.S. home prices expected to show continued rise — The market consensus is for today’s Apr S&P CoreLogic composite-20 home price index to show a solid gain of +0.4% m/m and +6.8% y/y, which would be close to March’s report of +0.5% m/m and +6.8% y/y. The index has been very strong in the past seven reporting months (Sep-Mar) with an average monthly increase of +0.7%. U.S. home prices continue to move higher on strong home demand and tight supplies. Home prices have yet to run into much resistance from higher mortgage rates.

2-year T-note auction to yield near 2.54% — The Treasury today will auction $34 billion of 2-year T-notes. The size of today’s auction is up by another $1 billion from May’s auction size of $33 billion and is up by $8 billion (30%) from the $26 billion size that prevailed in 2015/17. The Treasury has boosted the size of its auctions to cover the higher budget deficit caused by the Jan 1 tax cuts and higher government spending.

Today’s 2-year T-note issue was trading at 2.54% late yesterday afternoon, which was only 6 bp below the 9-3/4 year high of 2.60% posted two weeks ago. The 12-auction averages for the 2-year are: 2.85 bid cover ratio, $233 million in non-competitive bids to mostly retail investors, 3.6 bp tail to the median yield, 19.9 bp tail to the low yield, 64% taken at the high yield, and 47.1% taken by indirect bidders (far below the median of 63.5% for all recent coupon auctions).