- U.S. home prices expected to regain strength

- U.S. LEI expected to indicate continued strong GDP growth

- Unemployment claims expected to remain favorable

- 30-year TIPS auction to yield near 0.95%

- Oil prices prices rally on EIA report but are braced for OPEC+ production hike

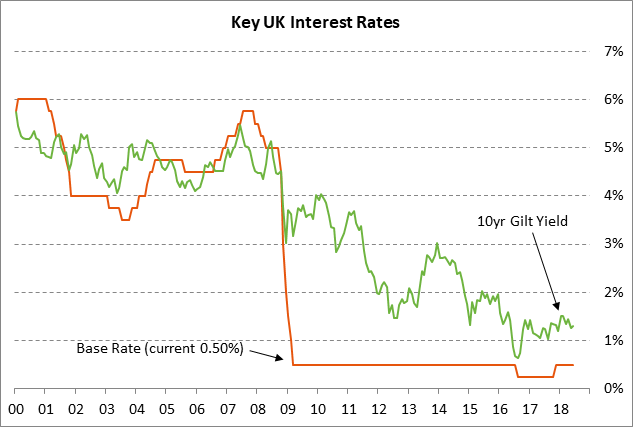

- BOE unanimously expected to leave rates unchanged

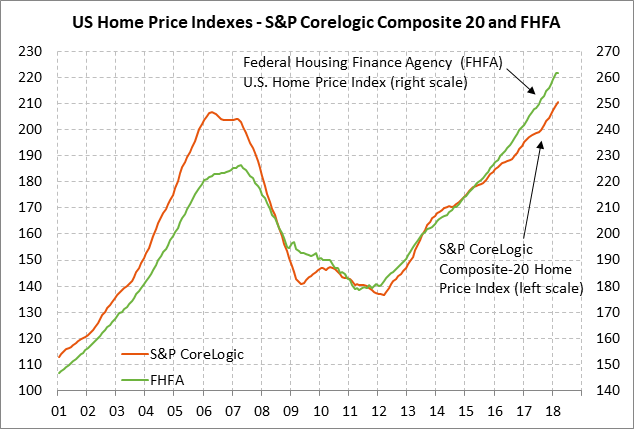

U.S. home prices expected to regain strength — The market consensus is for today’s Apr FHFA house price index to show a solid increase of +0.5% m/m, regaining strength after March’s weak report of +0.1%. The FHFA index has steadily risen since the housing-bust trough by a total of 46% and hasn’t shown a monthly decline in more than six years. The index has been particularly strong in recent months and showed a +6.7% y/y gain in March.

U.S. home prices continue to rise due to strong demand and tight supplies. Existing home sales in May were strong at 5.43 million units, which was only 5% below the 11-year high of 5.72 million units posted in Nov 2017. On the supply side, there were only 4.1 months worth of homes on the market in April, which was below the pre-crisis 2000-05 average of 4.5 months and well below the 7-8 month level that the National Association of Realtors says is consistent with stable home prices.

U.S. LEI expected to indicate continued strong GDP growth — The market consensus is for today’s May leading indicators report to show another strong increase of +0.4%, thus matching April’s +0.4% gain. On a year-on-year basis, the LEI in April was up +6.4% y/y, matching Feb’s 3-3/4 year high.

The market is looking for Q2 GDP to be very strong near 4.0% after the lackluster Q1 pace of +2.2%. The market is then looking for U.S. GDP growth to tail off a bit through year end but remain strong at +3.0% in Q3 and +2.6% in Q4. The U.S. economy is benefiting from a recent pickup in consumer spending and from the Jan 1 tax cuts.

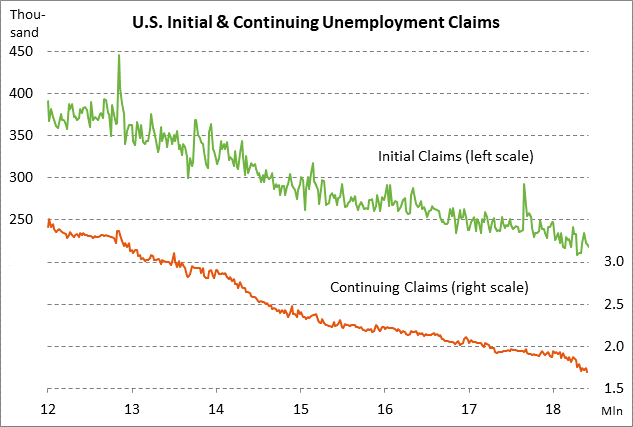

Unemployment claims expected to remain favorable — The consensus is for today’s initial unemployment claims report to show a +2,000 increase to 220,000 following last week’s -4,000 to 218,000. Continuing claims are expected to show a +13,000 increase to 1.710 million following last week’s -49,000 to 1.697 million. Layoffs in the U.S. economy are at or near the lowest levels in more than four decades. The initial claims series is only +9,000 above May’s 48-year low of 209,000, while continuing claims in last week’s report fell to a new 44-year low.

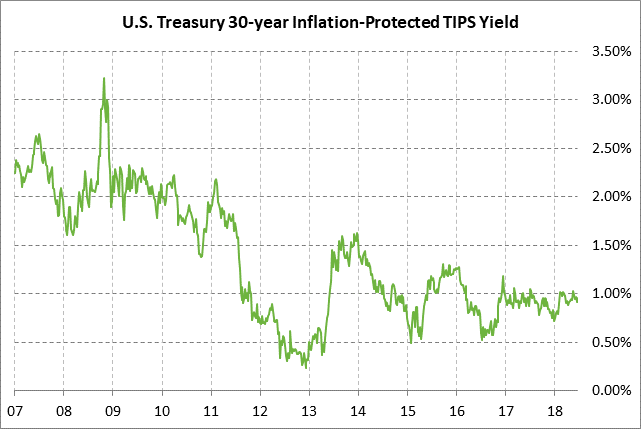

30-year TIPS auction to yield near 0.95% — The Treasury today will auction $5 billion of 30-year TIPS in the first reopening of the 1% 30-year TIPS of Feb 2048. The benchmark 30-year TIPS was trading at 0.95% late yesterday afternoon. The 30-year TIPS yield rallied by 20 bp early this year but has since been moving sideways.

The 12-auction averages for the 30-year TIPS are as follows: 2.31 bid cover ratio, $15 million in non-competitive bids to mostly retail investors, 6.8 bp tail to the median yield, 17.1 bp tail to the low yield, and 61% taken at the high yield. The 30-year TIPS is the most popular coupon security among foreign investors and central banks. Indirect bidders, a proxy for foreign buyers, have taken an average of 70.5% of the last twelve 30-year TIPS auctions, which is well above the median of 63.5% for all recent Treasury coupon auctions.

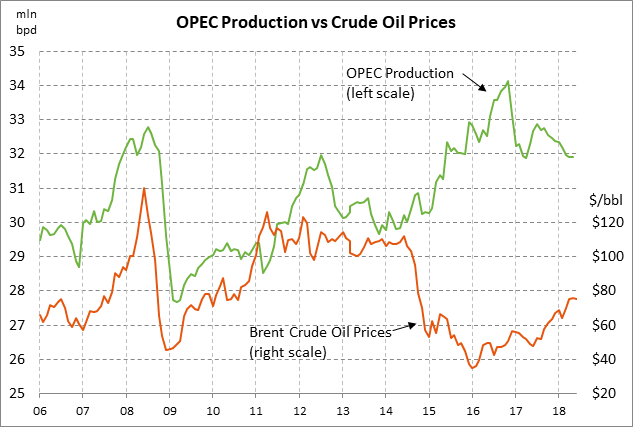

Oil prices rally on EIA report but are braced for OPEC+ production hike — Aug WTI crude oil prices on Wednesday rallied by +0.81 (+1.25%) to $65.71 as the weekly EIA report showed a sharp -5.91 mln bbl drop in U.S. crude oil inventories, which was much larger than the expected drop of -2.5 mln bbls. However, Aug Brent crude oil prices on Wednesday closed -0.34 (-0.45%) at $74.74 as the market looks ahead to a production hike at the OPEC meeting on Friday and the OPEC+ meeting on Saturday.

Iran on Wednesday sounded more flexible about agreeing to a production increase after bilateral meetings with other OPEC members. The production hike may be presented, not as a production hike, but rather as a reduction of the production cut originally agreed to in late 2017. The official OPEC+ production cut was 1.8 million bpd, but the actual production cut has been 2.2 million bpd due to cuts beyond the agreement by producers such as Venezuela. In any case, the market is still be expecting a production increase of somewhere between 300,000 bpd and 600,000 bpd, with the bulk of the higher production coming from Saudi Arabia and Russia.

BOE unanimously expected to leave rates unchanged — A recent Bloomberg survey found unanimous market expectations for the BOE today to leave its policy unchanged. The BOE’s last move was a +25 bp rate hike to 0.50% in Nov 2017 to reverse the -25 bp cut to 0.25% that was implemented in Aug 2016 after the June 2016 Brexit vote.

The market is expecting the BOE today to leave rates unchanged as it continues to monitor first-quarter GDP weakness and the rocky Brexit process. However, the market is still expecting a rate hike later this year in order to address still-high inflation. The market is discounting about an 80% chance of a rate hike by September and a 100% chance of that rate hike by Feb 2019.

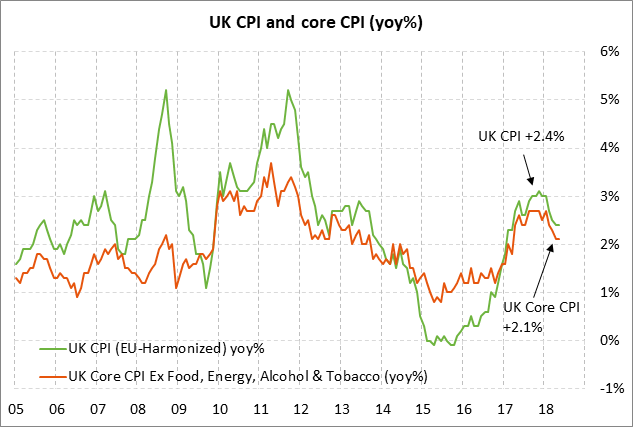

UK inflation has eased substantially in the past several months but is still above target. The UK CPI in April/May fell to +2.4% y/y from the 6-year high of 3.1% posted in Nov 2017. Meanwhile, the UK core CPI in April/May fell to a 14-month low of +2.1% y/y from the 6-year high of +2.7% posted in late 2017.

Sterling is on the defensive after falling sharply by -8.4% in the past two months to a 7-month low on Wednesday. Sterling has fallen sharply due to deferred expectations for a BOE rate hike and due to the rocky Brexit process as Prime Minister May had a very difficult time getting her Brexit bills through Parliament this week.