- Weekly global market focus

- Massive Treasury supply dump begins today

Weekly global market focus — The U.S. markets face an extremely busy week with the focus on (1) reaction to the weekend G-7 meeting, which ended in acrimony after the Trump administration accused Canadian Prime Minister Trudeau of “betrayal” and refused to sign the joint G-7 communique, (2) the Tue/Wed FOMC meeting, which is unanimously expected to produce a 25 bp rate hike, (3) Tuesday’s U.S.-North Korea summit in Singapore, (4) an expected uptick in Tuesday’s May U.S. CPI to +2.7% y/y from April’s +2.5% (core CPI expected +2.2% from April’s +2.1%), (5) the Treasury’s massive sale of $193 billion of securities today and Tuesday, and (6) a light earnings week with the only two of the S&P 500 companies scheduled to report.

Trade tensions will be front-and-center as the Trump administration this Friday (June 15) is scheduled to release the final list of $50 billion worth of Chinese products that could be subject to a 25% tariff. The administration has said that the tariffs could be implemented “shortly thereafter.” If the U.S. goes ahead with the tariff, then China would almost certainly retaliate with a reciprocal tariff on the $50 billion of U.S. products that have already been detailed. NAFTA will also be in the news after President Trump again threatened to leave NAFTA and also raised the possibility of slapping auto tariffs on Canada in response to Canadian Prime Minister Trudeau’s criticism of U.S. trade policy on Saturday.

The markets this week will closely follow oil prices ahead of next Friday’s (June 22) OPEC+ meeting, which could produce some relaxation of the OPEC+ production cut. Saudi Arabia and Russia have floated the idea of raising OPEC+ output to offset reduced Venezuelan and Iranian production but there is opposition from other OPEC members that want to keep oil prices high. There will be key Saudi-Russian meetings this week with Russian President Putin meeting with Saudi Crown Prince Mohammed Bin Salman on the sidelines of the World Cup in Russia. In more substantive meetings, Russian Energy Minister Novak will meet this week with Saudi Energy Minister Khalid Al-Falih in Moscow.

In Europe, the focus will mainly be on Thursday’s ECB meeting where there will be a formal discussion about the future of the QE program and a possible announcement about how the QE program will end. In a Bloomberg survey, about a third of the respondents expect the ECB this Thursday to announce an ending date for QE, whereas about half of the respondents believe the ECB will wait until the July meeting to reveal the QE details.

The Swiss markets today will be relieved that Swiss voters on Sunday rejected the Vollgeld initiative (with only 24% voting in favor), which would have instituted sovereign money and eliminated the fractional reserve banking system upon which virtually the entire world’s banking system is based.

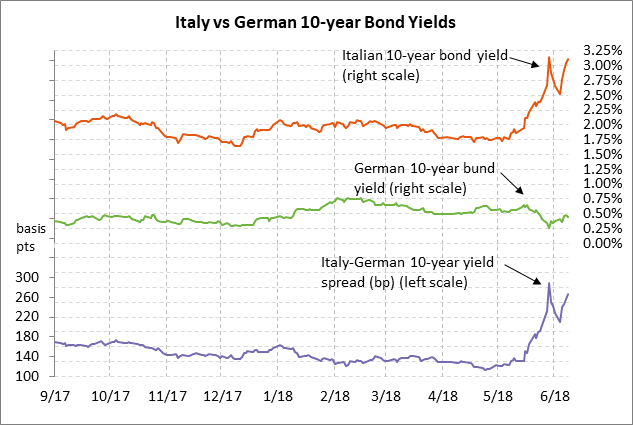

The Italian political situation remains tense with the 10-year Italian bond yield last Friday rising by +7 bp to 3.12%, which was only 4 bp below late-May’s 4-year high of 3.16%. The markets are waiting to see what legislation the new populist government will approve regarding tax cuts and a minimum citizen income, and the extent to which Italy will challenge Eurozone fiscal rules.

The UK markets this week will hinge on Brexit votes in Parliament on Tuesday and Wednesday as Prime Minister May tries to thread the needle on the intractable issue of the Northern Ireland border as well as other Brexit issues.

The Asian markets this week will mainly focus on the outcome of Tuesday’s U.S.-North Korea summit in Singapore and whether there is some progress that would reduce military tensions. Alternatively, the meeting could fall apart with increased military tensions. The Bank of Japan at its Thursday/Friday meeting is expected to leave its monetary policy unchanged.

Chinese economic data this week includes Wednesday’s May industrial production report (expected unchanged from April’s +7.0% y/y) and the May retail sales report (expected +9.6% vs April’s +9.4%). China’s May new home price report will be released on Thursday night.

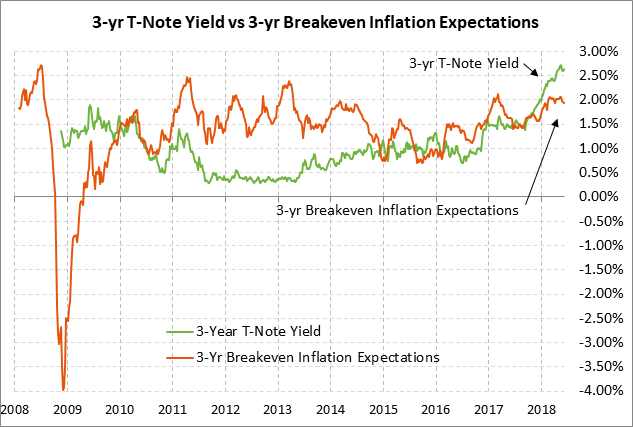

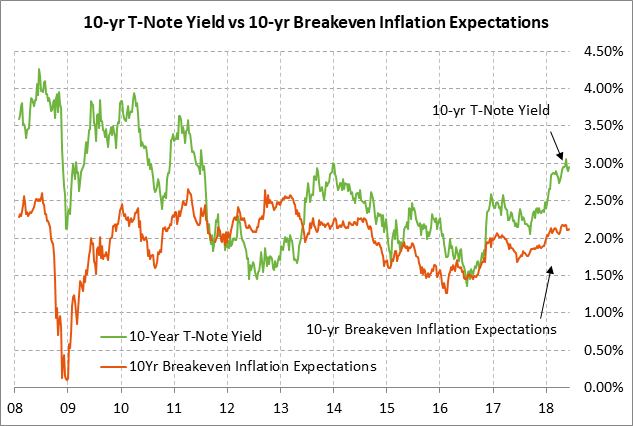

Massive Treasury supply dump begins today — The Treasury will sell $193 billion of Treasury securities today and Tuesday, including about $125 billion of T-bills. The Treasury will sell $32 billion of 3-year T-notes and $22 billion of 10-year T-notes today, and $14 billion of 30-year T-bonds on Tuesday. The Treasury wants to get the auctions out of the way before Wednesday’s FOMC meeting announcement. In when-issued trading late last Friday afternoon, today’s 3-year T-note issue was trading at 2.64% and today’s 10-year T-note was trading at 2.95%.

The $32 billion size of today’s 3-year auction is up by $1 billion from May’s auction and is $8 billion above the $24 billion size seen during 2015-17. The 12-auction averages for the 3-year are: 2.93 bid cover ratio, $70 million in non-competitive bids, 4.3 bp tail to the median yield, 25.1 bp tail to the low yield, 56% taken at the high yield, and 53.6% taken by indirect bidders (well below the average of 63.5% for all recent coupon auctions).

Today’s 10-year T-note auction will be the first reopening of May’s 2-7/8% 5-year note of May 2028. The $22 billion size of today’s 10-year T-note is $1 billion larger than the last reopening in March and April. The 12-auction averages for the 10-year are: 2.45 bid cover ratio, $19 million in non-competitive bids, 3.9 bp tail to the median yield, 16.5 bp tail to the low yield, 45% taken at the high yield, and 63.3% taken by indirect bidders (slightly below the average of 63.5% for all recent coupon auctions).